Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

We are going to look at the results of a paper published by AIMA (Alternative Investment Management Association) in collaboration with CAIA (Chartered Alternative Investments Analysts) Association The paper finds that more and more sophisticated investors are allocating to hedge funds not only as portfolio diversifiers but also as portfolio substitutes to traditional investments like stock and bond long only funds.

The paper uses a statistical, method known as cluster analysis, to take an accurate look at the risk and return profiles of each hedge fund strategy. Depending on the level of correlation of a hedge fund strategy to the underlying assets these funds will be considered as a substitute of long only allocation, or as a portfolio diversifier.

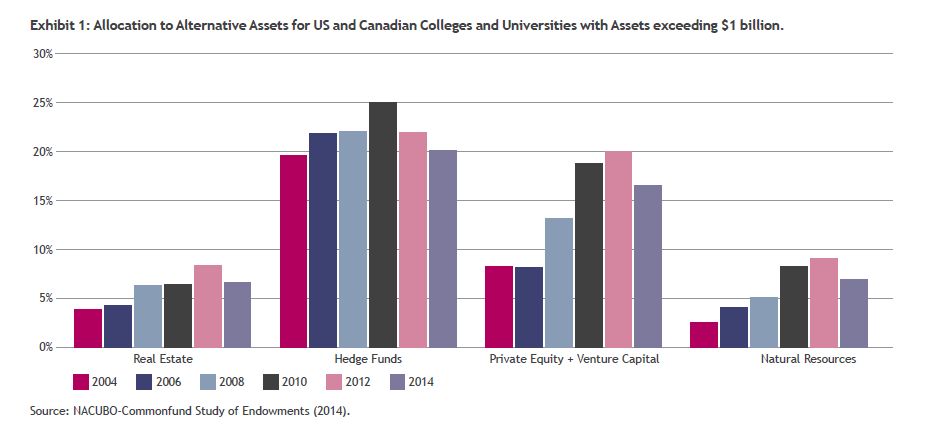

Establishing an allocation

Investors are increasingly allocating higher proportions of their portfolio to hedge funds. Each type of investor has different financial needs and objectives. A foundation may have very different needs to a family office which again may have very different needs to an endowment. They can all however benefit from the particular risk-return profiles of hedge fund strategies and their capability of generating positive returns under varying market conditions. This characteristic can also greatly help in providing long term capital preservation.

Apart from allocating to assets that have a low correlation to traditional investments, investors typically choose to invest in hedge funds for other qualities not found in long only funds. To gain exposure to investment strategies that are out of reach to traditional fund managers. Or to be able to take advantage of both bull and bear markets. Lastly to select the best managers which may add Alpha, something hard to find in traditional investment strategies.

More recently the reasoning behind hedge fund allocation has developed and taken on a few more characteristics. Risk budgeting now takes a more predominant role. This implies creating a portfolio with a lower overall risk profile to be able to allocate to riskier investments in a more meaningful way.

Investors are beginning to see a hedge fund allocation as a way of gaining access to higher yields through investing in a portfolio of fixed income arbitrage hedge funds. Low yields across the board in developed countries means traditional strategy funds in bonds are a poor investment.

Investors are increasingly considering their allocation to equity hedge funds as part of their total allocation to equity. Hedge fund strategiesedge fund strategies in this case are a substitute and not a complement to the equity portion of the portfolio.

Defining portfolio diversifiers and portfolio substitutes

The main criterion that divides substitutes from diversifiers is correlation to traditional assets, and therefore to long only funds. The paper defines the two subsets of hedge fund strategies in the following way

Substitutes

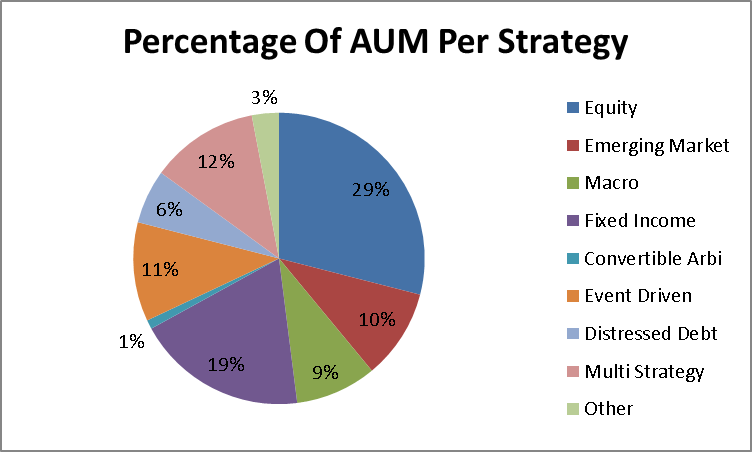

Long/Short hedge funds, including long/short equity, long/short credit and emerging markets. Equity strategies make up the largest hedge fund strategy, with equity long/short being the largest single strategy. According to the paper HFR (Hedgefundresearch.com) found that over the last 25 years the HFR equity hedge index gave an annualized return of 11.9% with a risk of 8.9% as measured by standard deviation. That compares favorably when considering the S&P 500 which had an annualized return of 7.36% and risk of 14.6% over the same period. As these strategies allow for going long as well as short and for covering sector or market wide risk using hedging, managers can achieve positive results even in times of market stress.

The long short strategy also works in the same way using fixed income securities as the underlying asset. Managers in long/short credit strategies invest across the corporate capital structure with exposure to differing levels of seniority of debt. The strategy looks to capitalize on market inefficiencies while maintaining a low exposure to market cyclicality.

Event driven including, activist, merger arbitrage, special situations and distressed securities. These strategies have one thing in common they take advantage of special situations in an attempt to earn outperforming returns. Event driven strategies focus on headline news or major corporate events that may give rise to a change in value of a company’s stock. The Merger arbitrage strategy attempts to profit from the success of a merger or acquisition actually going through, although some managers will also set up trades to bet on the failure of the merger or acquisition.

These strategies are sought by investors who do not have the means or the time to be analyzing the markets constantly for the catalyst that will drive price change. Managers are set up to act quickly and efficiently to take advantage of specific events.

Diversifiers;

Global Macro and Managed futures. These types of strategies are the least correlated to traditional investments and take advantage of extremely loose investment mandates and trading styles. Macro global managers may invest across all types of assets from stocks, bonds, currencies interest rates and commodities. Some managers will look at individual stocks in an attempt to take advantage of an undervalued company. Most managers however of this strategy look at the global macro narrative and invest where they specifically believe there is opportunity, regardless of geographical boundaries. They are more likely to use broad indices, commodity or interest rate swaps and forwards.

CTAs, have a similar philosophy but invest through Futures traded on major exchanges. Again they may not necessarily be limited to any particular asset or geographical location. These two strategies are known for being able to perform well in even the most adverse market conditions and are strongly regarded for the capacity to reduce overall risk of a portfolio. Managed futures was the strategy that had the least overall drawdown during the 2008 crisis. Data from hedgeindex.com shows that during the 2 year period from 2008 to 2009 their managed futures index had a monthly average ROR of 0.47% and a monthly standard deviation of 3.2%.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst