Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Hedge funds are well known for being risky and at the same time rewarding with the emphasis being on risky. The truth is they can be extremely risky as a standalone investment in any single Hedge Fund. However placed within the context of a diversified portfolio allocation to Alternative Investments creates a different picture. A portfolio of diversified Hedge Funds can bring downside protection and diversification of risk and return.

It is necessary to create a portfolio of several investments so as to diversify the risk of holding actively managed assets.

Although Hedge Funds often trade and invest in traditional assets, like Stocks and Bonds or their derivatives, they are not necessarily limited by a governing body in terms of how much concentration they may have in any one asset, their use of derivatives or the possibility of taking short positions. This leads to Hedge Funds often having very low to sometimes negative correlations with traditional assets like Stocks or Bonds.

Diversification potential

Diversification potential is mostly likely to arise when there is very low correlation. The closer correlation is to zero the greater the potential in diversification as returns will be less likely to move in the same direction at the same time.

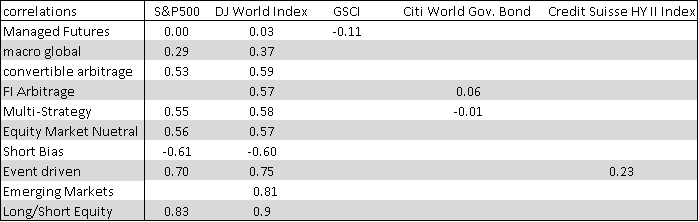

The table below shows correlations for indices of the most frequently defined Hedge Fund strategies. We can see the low correlation to stocks of strategies like Global macro and Managed Futures; 0.29 and 0.00 when compared to the S&P 500. This is due to their strategies which are completely independent of general market direction even though in the case of Global Macro these funds may be investing in Stocks. The Managed Futures funds index also has a low correlation to GSCI (Goldman Sachs Commodity Index), at -0.11, which shows again that despite trading in the assets underlying the GSCI returns have no correlation due to its strategies.

The other indices of Hedge Fund strategies have correlations that vary from 0.53 for Convertible Arbitrage to 0.86 for Long/Short Equity. Fixed Income Arbitrage and Multi-Strategy also have very low correlation to Bonds; 0.06 and -0.01 respectively when compared to the Citi World Government Bond Index. A correlation of 0.86 is high given that maximum correlation is 1. This is mostly due to the fact that these Funds may find themselves net long in a Bull trend and net short in a Bear trend. However the strategy may still fit in a portfolio of Hedge Funds creating the necessary diversification of strategies.

The Short Bias strategy as expected has a negative correlation to the performance of a general stock index. These types of funds may serve as downside protection as they will be net short of the market when the bear trend begins and remain net short during the whole regime.

Source Hedgefundindex.com

Given the low correlations to traditional assets Hedge Funds offer a very high diversification potential for risk as well as return. A solid due diligence program is necessary when choosing which Hedge Fund to invest in and it is necessary to have a clear idea of how many Funds and in which strategies investments will be made to keep the Hedge Fund portion of the portfolio well diversified.

Downside Protection and Risk

Something of great concern to investors is downside protection. This is traditionally achieved by buying Put options on a general stock Index such as the S&P 500. This can prove expensive as it does not generate any income, in fact it only undermines the performance of the portfolio. Another way is to include assets that are less likely to be as risky or are less likely to have as large maximum drawdowns. As we saw above Short Bias strategy funds could give some protection to the downside in times of a Bear market. But they come at a cost as they are more likely to show negative returns in times of Bull markets.

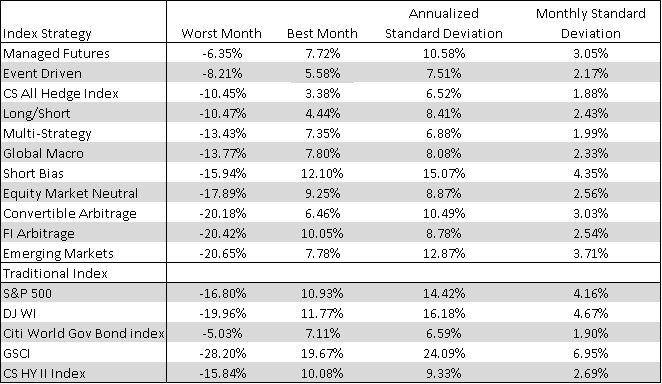

Looking at the table below we can see how the strategy Index with the lowest worst month was Managed Futures at -6.35% this compares favourably with the worst month for S&P 500 at -16.80%. It is also only worse than the Citi World Government Bond Index at -5.03%. Whereas the strategy Index with the highest monthly drawdown amongst Hedge Funds was Emerging Markets with -20.65%.

In terms of risk measured by volatility the lowest volatility for a single strategy was shown by the Multi-strategy index with Annualized standard deviation at 6.88% which is considerably lower than the standard deviation for S&P 500 at 14.42%

However the broad CS All Hedge Index had an even lower standard deviation than any single strategy index, at 6.52%, indicating the potential benefit of a well-diversified Hedge Fund portfolio in reducing riskiness.

Source Hedgefundindex.com

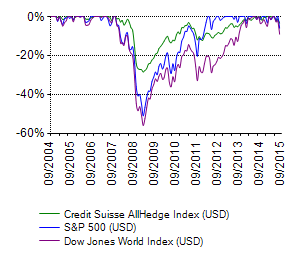

The graph below shows the maximum drawdown for the Credit Suisse All Hedge Index, S&P 500 and the DJ World Index. The years leading up to the crisis show that there wasn’t that great of a difference between the indices. During the 2008 crisis you can see how the broad Hedge Fund Index offered some downside protection in that it had a much lower maximum drawdown than its traditional counterparts. The subsequent 2 years after the crisis also show that the Hedge Funds index performed better in minimizing drawdowns than the stock indices.

Source Hedgefundindex.com

What The Numbers Show

We can see from the above data that the low correlation to Stocks and Bonds offered by Hedge Fund indices shows that a well-diversified investment in Hedge Funds has the potential to offer A) diversification benefits such as lower volatility. B) Reducing maximum drawdowns.

Adding an asset that has a low correlation to the underlying assets of the portfolio reduces overall volatility, this effect is further enhanced if the asset being added has a lower volatility than that of the constituent assets. At the same time it may reduce the effect of negative shocks, such as those seen during the last crisis.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst