Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Retirement investors are often stuck having to choose between the volatility of the stock market and the underwhelming stability of money markets and bond yields. Self-directed retirement savings accounts are the perfect middle ground solution between these two extremes.

A self-directed 401(k) lets investors take charge of their retirement portfolios by providing them the freedom to pick-and-choose from a variety of diverse asset classes that best suit their retirement goals. With a self-directed 401(k) or individual retirement account (IRA), investors can diversify with everything from stocks and fixed-income securities to real estate, cryptocurrencies, precious metals, tax liens, and even fine art.

In years past, setting up a self-directed 401(k) was a time-consuming process that involved a lot of hoop-jumping and playing phone tag with your stockbroker. Thankfully, those days are behind us. Today, you can sign up for a self-directed retirement savings account with the click of a button.

Know that a self-directed 401(k) is not without its share of risks. In this article, I’ve taken a close look at self-directed 401(k)s and unpacked their various pros and cons to help you decide for yourself whether this retirement savings account is right for you.

401(k) vs. IRA: What You Need to Know

First, let’s compare the differences between IRAs and 401(k)s. To do so, we have to first distinguish between Roth IRAs and Traditional IRAs. Below, I’ve provided the cliff notes for each:

Roth IRA

- Tax-deferred retirement savings account

- All contributions are with after-tax dollars

- Penalty-free, tax-free withdrawals after age 59 ½

Traditional IRA

- Tax-deferred retirement savings account

- All contributions are with pre-tax dollars

- Withdrawals after age 59 ½ are taxed as ordinary income

- 10% early contribution penalty if distributions are taken pre-retirement

In both cases, your investments grow tax-free in a sheltered savings account. However, their key distinction is that Roth IRAs consist of contributions that have already been taxed as regular income. Therefore, they won’t be subject to taxation after one starts making withdrawals in their retirement. Withdrawals taken from Traditional IRAs are taxed as regular income at the time of withdrawal and are thus subject to one’s marginal tax rate at that time.

In a nutshell, Roth IRAs are best suited for individuals who expect to be in a higher tax bracket when they start taking withdrawals in retirement (e.g., medical students on track to become highly paid physicians).

A Traditional IRA, on the other hand, is the better option for those in higher tax brackets (i.e., >22%). Under this option, you’re deferring high taxes today with the hope that you will be in a lower tax bracket in your retirement.

Today, young people are taking out Roth IRAs in record numbers under the expectation that their earning potential will continue to grow as they enter retirement age. A 2018 study by Fidelity found that 41 percent of Roth IRAs are opened by millennials aged 38 or younger. Keep in mind, however, that there’s nothing stopping someone from opening both a Roth and Traditional IRA and using each strategically based on differing tax situations.

The 401(k) Advantage

The main differentiating factor between a 401(k) and IRA is that the former must be established by the account holder’s employer. In a 401(k), employees and their employer decide to contribute a predetermined share of their pay into a single plan trust. The trust administrator tracks each account holder’s balance separately, and contributions are deducted directly from the employee’s paychecks.

Often, employers offer a 401(k) match policy up to a certain limit. Usually, that limit is 50 cents on the dollar for up to 6% of the employee’s gross pay. This arrangement is becoming the new standard, with 80% of U.S. companies offering a 50%/6% employer match in 2019.

For example, if you earn a $60k salary pre-tax, then an employer under the standard matching scheme would contribute $1,800 ([60,000*0.06]/2) to one’s 401(k) annually. To pass on an employer’s 401(k) match would be tantamount to leaving free money on the table. That’s why it’s imperative that employees contribute at least until the point that their employer stops matching.

Like an IRA, 401(k)s can be Roth or Traditional. The same distinctions apply here as they do with IRAs—Roth implies contributions are after-tax, and Traditional contributions are pre-tax—and the same tax advantages hold true across both account types.

Why Open a Self-Directed 401(k)?

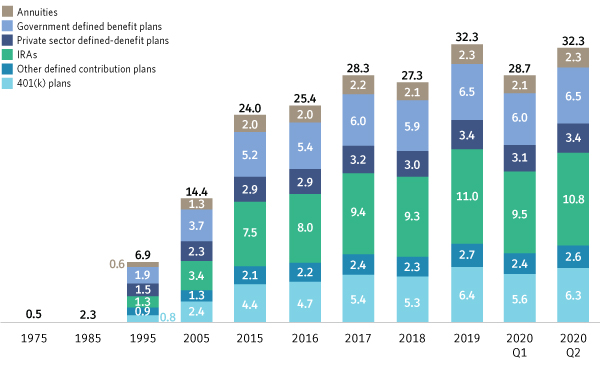

Once upon a time employees could count on their company-sponsored pensions to set them up comfortably in their retirement. These days, retiring on a pension alone is a luxury reserved for the few. When 401(k)s and IRAs were introduced toward the end of the 20th century, as depicted by the graph below, the responsibility to provide for one’s retirement was shifted from employers and government programs to the employee.

Source: Investment Company Institute

For many Americans, their 401(k) is their own retirement savings account. Naturally, people want control over their money and their financial future. It’s no surprise then why self-directed 401(k) plans have a certain appeal for investors who want a more active role in their investments.

Similar to a self-directed IRA, a self-directed 401(k) permits investors to spread their wealth across a variety of asset classes otherwise unavailable in conventional plans. For example, real estate, private placements, money lending, and precious metals are all eligible for inclusion in a self-directed retirement account. With a standard brokerage account, you’re tightly restricted on the assets you can and can’t invest in and are often confined to fixed-income securities and equities.

How Do Self-Directed 401(k) Plans Work?

There are two distinct types of self-directed 401(k): standard self-directed 401(k)s and checkbook control 401(k)s. With the latter, investors are given full freedom to invest in alternative assets alongside traditional assets like stocks, bonds, and ETFs.

Note that self-directed 401(k) plans are subject to the same laws and limitations as standard brokerage accounts. As such, account holders are only permitted to contribute $23,000 to their 401(k) for 2024. However, those age 50 or older can make catch-up contributions of $7,500 for 2024.

As depicted by the chart below, 401(k) contribution limits have gradually increased over time. Generally, the employee contribution portion rises by $500 per annum every 1-3 years, and the age 50+ catch-up contribution rises by $500 every 5 years. Savvy investors would do well to account for these contribution cap changes over time when devising their retirement savings strategy.

Source: DQYDJ

Since you’re in full control of your investment portfolio with a self-directed 401(k), it’s crucial that you do your due diligence to comply with IRS regulations. Luckily, you don’t have to jump through hoops or dig through pages of legalese to keep on the right side of the IRS. A self-directed 401(k) administrator or custodian can help keep your account compliant so you can stay focused on trading and finding new opportunities in the market.

What Are Self-Directed 401(k) Administrators?

A 401(k) is usually administered by a brokerage or an investment company. However, self-directed accounts are, by definition, independent of third-party brokers or investment providers. This is why you’ll likely never find a “Fidelity self-directed 401(k)” or a “Vanguard self-directed IRA”—these brokerages simply make too much money on custodian fees to justify allowing their customers to direct their own accounts.

This is both good and bad. Two things that brokerages do well is that they protect customers from assuming financial risks that they cannot afford, and they ensure their account holders remain compliant with regulators and the IRS. The downside is that brokerage-enabled plans charge fees and commissions that eat into your earnings, and they restrict the types of assets you can invest in.

Luckily, there’s a middle ground solution. A self-directed 401(k) administrator can help you stay abreast of IRS regulations while giving you the freedom to invest your money in assets of your choosing. Typically, brokerage accounts limit your 401(k) investments to pre-approved mutual funds with high expense ratios. An administered 401(k), however, gives you full authority to pick the underlying assets that best suit your investment goals.

If you invest in precious metals through your 401(k), federal law requires that you have an account administrator that acts as a third-party custodian. Your account custodian vaults your precious metals bullion and ensures that it is compliant with IRS storage and processing standards. Bullion stored in one’s home (or, “home storage gold”) is ineligible for inclusion in a 401(k) or IRA.

What Is A Self-Directed Solo 401(k)?

For retirement investors who aren’t traditionally employed, a self-directed solo 401(k) is your go-to retirement investment vehicle. Designed for self-employed individuals, a solo 401(k) boasts several unique benefits unavailable to regular self-directed 401(k) account holders, such as:

- Higher Contribution Limits: One of the primary benefits of a solo 401(k) that’s self-directed is that the annual contribution limit is boosted (depending on whether you qualify for a catch-up contribution) to $69,000, catch-up contribution included for 2024. Therefore, a solo 401(k) allows for significant retirement savings in a short period of time, whereas regular self-directed 401(k)s are held to low annual contribution caps.

- Participant Loans: As a freelancer, it can be hard to get approved for credit. That’s why self-directed solo 401(k) holders can take out a participant loan of up to $50,000 or 50% of one’s account balance. In most cases, these loans are issued at prime plus 1% interest, and have no credit requirement.

- Roth Savings: Don’t want to pay income tax in your retirement? With a self-directed Roth Solo 401(k), you can contribute up to $30,500 post-tax dollars per annum (for those 50 or older) and keep your gains tax-free when it comes time to withdraw.

- Total Discretion: Like a regular self-directed retirement account, a solo 401(k) gives you full discretion over your portfolio and allows you to diversify with alternative asset classes like real estate, cryptocurrencies, and precious metals.

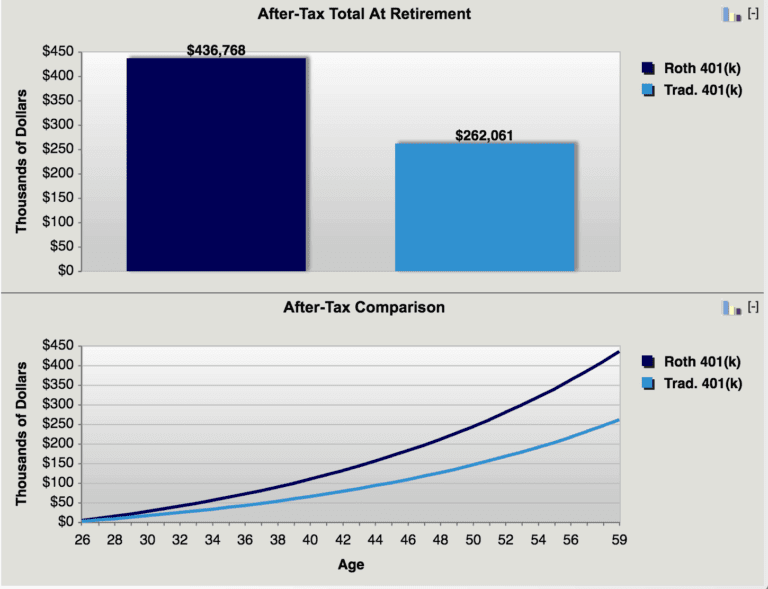

If you’re on the fence about whether to open a Roth or Traditional 401(k), take a look at the chart below. For most young investors who are in a lower tax bracket (i.e., 32% marginal tax rate or lower), you save more money over time by opting for a self-directed Roth 401(k).

Source: Millennial Money

The difference isn’t even close. In the same amount of time and with the same annualized returns (5%), contributions ($5,000), and retirement age tax bracket (40%), a Roth 401(k) garners an after-tax total of $436,768 over a 23-year time horizon. This constitutes a +66.5% improvement over a self-directed Traditional 401(k), which would accrue $262,061 under the same conditions.

In other words, if you’re in a lower tax bracket now and expect to earn much more during your retirement, you should consider opting for a self-directed Roth 401(k). This way you can contribute dollars taxed at 23% now, for example, instead of 40% or higher later in life.

Funding Your Self-Directed 401(k)

To add funds to your self-directed 401(k), you have three main options.

- Rollovers: Existing funds in a 401(k), IRA, 403(b), 457(b), or any other qualification retirement savings account can be rolled over to one’s self-directed 401(k). Transferring funds from a non-401(k) account to one’s 401(k) is called a “rollover” and is limited to one rollover per 12-month period. Moving funds from an existing 401(k) to a new, self-directed 401(k) is referred to as a direct rollover or transfer and must be executed within 60 days after taking a distribution from the existing employer-sponsored 401(k).

- Contributions: Account holders can make regular personal deferrals from their paychecks or self-employment income to their self-directed 401(k). In 2024, self-employed individuals can contribute 100% of their income up to $23,000, and those over the age of 50 can take advantage of an additional $7,500 in catch-up contributions ($30,500 total for 2024).

- Profit-sharing: Some self-directed 401(k)s are also profit-sharing plans (PSP), which, per IRS regulations, allows for two distinct entities to make defined plan contributions that derive from the sponsoring party’s profits.

How To Set Up A Self-Directed 401(k)

We’re often asked how to set up a 401(k) that’s self-directed and untethered to a sponsored employer. Since you can’t simply walk into a Fidelity or Charles Schwab location and ask for a self-directed 401(k), it can feel a bit complicated opening a self-directed account.

Most self-directed 401(k) account holders are in one of two situations—they’re earning self-employment income as their primary income source, or they’re employed but aren’t eligible for an employer-sponsored 401(k). If either case describes you, you’re obliged to create and operate a qualifying self-employment business which acts as the holding company for the account.

There are several types of corporate entities that qualify for self-directed 401(k)s, including:

- Sole proprietorships

- Married couple sole proprietorships

- S-Corps

- C-Corps

- Limited Liability Companies (LLC)

No matter which type of business you incorporate, it’s crucial that you don’t employ any full-time employees (i.e., individuals working over 1,000 hours per annum). The only exception is one’s spouse, who can work full-time for the company without being classified as a full-time employee.

When it comes time to finally open the account, contact a third-party 401(k) custodian who under federal law must act as an administrator of the retirement vehicle. For more information about getting started with a self-directed checkbook 401(k), check out this helpful guide to 401(k)s for beginners.

Should You Open A Self-Directed 401(k)?

Since self-directed 401(k)s encompass more risk than your standard brokerage 401(k), it’s certainly not the best retirement savings vehicle for everyone. This is especially true for older investors who are near their target retirement age (i.e., <5 years from retirement). Investors closer to retirement might find more value in a brokerage account that’s moored to low-risk ETFs and mutual funds.

However, self-directed accounts aren’t limited to young investors who can absorb more risk. For instance, investing in precious metals like gold and silver bullion is an excellent way to insulate your portfolio from market risk later in life. With a traditional 401(k), you’re barred from investing in these assets, whereas a self-directed 401(k) gives you full discretion to diversify how you please.

With a self-directed 401(k), you’re given the freedom to pick and choose the asset types you want to invest in, such as real estate. Self-directed 401(k) real estate investing is possible and allows you to own investment properties within a tax-sheltered environment. Last month, we covered self-directed IRA real estate investing. Be sure to check out this guide, because many of the caveats that apply to self-directed 401(k) real estate investing also apply to IRAs.

In short, a self-directed 401(k) might be the better option for investors who want to diversify their retirement portfolio with assets that aren’t merely stocks and bonds.

The chart below demonstrates how a more conservative investor can hedge against systemic risk and uncertainty by taking a position in precious metals in their 401(k). During the recent coronavirus stock market crash, gold and precious metals retained their value while the equities market plummeted. Younger investors, however, still benefit from a self-directed 401(k) because it allows for broader diversification with cryptocurrencies, real estate, tax liens, or even fine art.

Source: CCN

Self-Directed Traditional vs. Solo 401(k)

If you’re self-employed, a Solo 401(k) might be your best bet. Since self-employed individuals don’t have access to an employer-sponsored, defined-contribution 401(k), Solo 401(k) contribution limits are set significantly higher, at $69,000 in 2024.

Solo 401(k) rules are comparable to traditional self-directed retirement accounts, in that there are no age or income restrictions and that you must be a business owner without employees. A Solo 401(k) may consist of pre- or after-tax dollars, just like a regular IRA or 401(k). For strictly self-employed individuals, it usually makes more sense to open a Solo 401(k) since the contribution limits are set well above a traditional self-directed 401(k).

Take Control of Your Retirement: Open A Self-Directed 401(k) Today

In March, the stock market saw the most devastating crash since the infamous Crash of 1929. The S&P 500 dropped 30.94% in the one-month period between February 21 and March 20. On March 16 alone, the Dow Jones Industrial Average fell nearly 13%. Can you really afford to let your retirement savings fall by 13% in a single day?

With a self-directed 401(k) or IRA, you’re at the helm of your own retirement strategy. Unlike a brokerage account, you aren’t restricted to high-fee mutual funds. Instead, you have the power to diversify your portfolio with alternatives such as real estate, precious metals, and cryptocurrencies. This way, when the next market crash occurs, you’ll protect more of your retirement nest egg.

To get started with a self-directed 401(k), check out our list of IRS-approved retirement accounts. For more insider investment information and to stay abreast of the latest trends in retirement investing, consider subscribing to these top investment newsletters—this way, you won’t make any false moves with your hard-earned retirement savings.

The information provided here is not investment, tax, or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.