Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Mark Twain once wrote, “Buy land, they aren’t making it anymore.” Though he wasn’t known for his sage financial one-liners, I think Mark was onto something.

Real estate is a finite commodity, and housing is a basic, universal human need. The characteristics of scarcity and inelastic demand make real estate a unique investment type that’s relatively well-guarded against broader market downturns.

Today, on the heels of a recession, investors are turning to safe-haven assets to protect their retirement savings from stock market volatility. Diversifying with tangible assets like real estate can help safeguard wealth in bear markets and provide positive cash flow in the form of rent payments.

With a self-directed individual retirement account (IRA), you can take charge of your portfolio by investing in a broad range of alternative asset classes such as precious metals, private placements, tax liens, and, yes, even real estate. Below, I’ve compiled all the must-know information you need before getting started with a self-directed real estate IRA.

Why Invest in Real Estate Via A Self-Directed IRA?

IRAs are more versatile investment vehicles than most people give them credit for. Few investors realize that IRAs are more than tax-deferred accounts for stocks, bonds, and mutual funds, and even fewer understand that you can buy, sell, and rent investment properties in an IRA while the proceeds grow tax-free.

The tax advantages are just one of several upsides to self-directed IRA real estate investing. Below, I’ve listed the other commonly cited benefits of holding investment properties in an IRA.

Equity Leverage

Leverage is a compelling reason for investing in real estate with an IRA. Nobody is going to loan you 400% of your net worth at 3.5% to invest in the stock market. But they will for real estate.

Let’s assume you have $50,000 to put down on a $250k asset that’s likely to rise in value. Now let’s go a step further and assume it breaks even on a monthly basis after expenses such that you don’t profit a single dollar at year-end. In this case, the property will have a negligible impact on your tax forms and won’t impact your tax liability.

What if the home appreciates in value by 5% in a given year? You won’t earn 5% on $50k ($2,500), you’ll earn 5% on $250k ($12,500), which is a hefty 25% ROI on your initial $50k investment. By contrast, if $50k in the stock market returns 8% in a year, you would make only $4,000 and might owe taxes on the gains as well.

A Note on Leverage Risk

Of course, leverage works both ways. However, real estate is unique in that it’s one of the few highly asymmetric investments where retail investors are far more likely to realize gains on their leverage than losses.

Traditionally, if the property depreciates you’re entitled to a sizable tax deduction that can be written off your income—this is one of the most unique risk-minimizing benefits of real estate. You can calculate a residential property’s depreciation deduction by calculating its cost basis and dividing the sum by 27.5. However, since your IRA doesn’t pay taxes, IRA-held real estate is ineligible for deductions on property taxes, depreciation, upkeep, or mortgage interest.

You can lessen your exposure to leverage risk in real estate IRA investing by making a larger down payment on the property. The more money you put down on the property, the less leverage risk you assume in selling at an inopportune time in the market cycle.

Cash Flow

Investment properties generate significant rental income, especially after you consider the impact of leverage. In a regular, taxable account, your rental income would be subject to taxation as if it were ordinary income minus depreciation and interest income.

A self-directed IRA skirts this problem, allowing your rental income to be reinvested tax-free, for as long as the money remains in the IRA. Holding investment properties in an IRA lets you productively reinvest positive cash flow back into the properties in the form of:

- Repairs

- Capital improvements and renovations

- Legal fees (i.e., LLC filing fees)

- Insurance premiums

- Furniture purchases

- Paying down mortgages

- Marketing expenses

It’s important to note that all property-related expenses and maintenance costs must be paid with IRA funds. All repairs and work rendered on the property must be carried out by someone else who manages the property. Otherwise, you may trigger a taxable event by engaging in a self-dealing transaction.

Moreover, the portion of the rental income attributable to leverage is still subject to income taxes. In this case, a home worth $250k for which you have a 25% equity stake would require you to pay income taxes on 75% of the cash flow generated by the property. The more equity acquired in the property over time, the less you will owe in taxes on your rental income.

Note that your tenants must write their rent checks to the self-directed IRA that owns the property. If your tenants make their checks out of you directly, the IRS will regard it as a distribution and will therefore be subject to taxation and may trigger early distribution penalties.

Diversification

Real estate is generally a less volatile long-term investment than most traditional assets, and often moves counter to financial markets. Including investment real estate in your IRA has been proven to increase risk-adjusted returns over time. Small wonder why 11% of the world’s ultra-wealthy made their fortune with real estate as the central component of their investment strategy.

Favorable Government Incentives

In the U.S., federal government programs exist to incentivize real estate acquisitions. With a Federal Housing Administration (FHA) loan, you can receive government-backed financing of up to $500k to purchase a home with only 3.5% down. There isn’t a lender in the world that would offer this much leverage for acquiring other assets like equities or fixed-income securities.

Additionally, 1031 rental transfers (referring to Internal Revenue Code Section 1031) allow real estate investors to defer capital gains taxes on rental properties virtually indefinitely. A 1031 exchange is a 180-day process that lets you swap one like-kind investment property for another, which changes the form of the investment without recognizing a capital gain, therefore allowing your investment to grow tax-deferred.

Tax Deferral

If you invest $100k in real estate through an IRA and then sell at $150k, you don’t pay tax on the difference. Whereas investing personally might cost you 20% of your capital gains.

Capital gains on real estate would otherwise be taxable for sellers who net large returns on their investment. Currently, the IRS allows home sellers to exclude up to:

- $250,000 of real estate capital gains for single homeowners

- $500,000 of real estate capital gains for married sellers or joint filers

The downside is that these capital gains exemptions go out the window if the property wasn’t your principal residence or if you’ve already claimed the exemption for another home solid in the last two years.

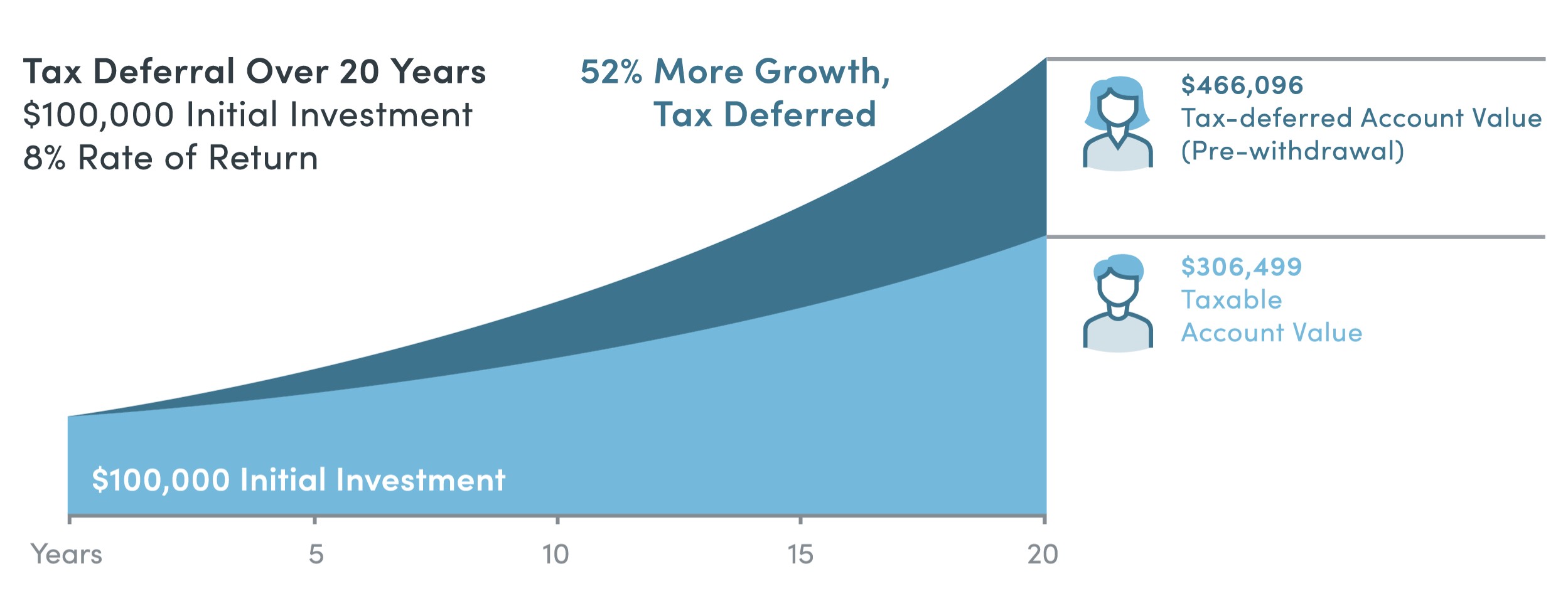

As investment income is reinvested into the IRA over time, the power of tax deferral becomes clear. Below is an illustrated example of the difference that 20 years of tax deferral can make on a $100k investment with an 8% average annual return and assuming a 28% overall tax rate for both parties.

Source: Security Benefit

Rules for Real Estate Self-Directed IRAs

Before you hop on LegalZoom, set up an LLC, and probe Zillow for the hottest duplex deal, first brush up on the rules that govern how self-directed real estate IRAs operate. If you don’t follow the rules and regulations, you risk losing the tax-deferred status of your account.

- The Disqualified Persons Rule: Your IRA cannot purchase real estate through “self-dealing” transactions through which you or a direct family member benefit. Therefore, your IRA cannot acquire properties that you, your spouse, or any descendant or spouse of a descendent already own.

- All Rental Income Must Redirect to Your IRA: Positive cash flow accrued from an investment property held in your self-directed IRA must direct back to your IRA custodian and reenter the account.

- The “Indirect Benefits” Rule: Given that IRAs are designed to provide for your future retirement, you’re barred from using them to benefit yourself today. Using your self-directed IRA to purchase a vacation home or rent an office space for yourself in a property owned by your IRA, for example, would constitute a disqualifying “indirect benefit”.

- UBIT Taxes: Investment properties held in an IRA purchased with leverage are subject to unrelated business income taxes (UBIT).

- The Title Rule: It’s crucial that you keep you and your IRA separate legal entities. Therefore all documents pertaining to investments held in your IRA must be titled appropriately to reflect this distinction (e.g., Equity Trust Company Custodian FBO (For Benefit Of) [Account Holder’s Name] IRA).

Tax benefits are what motivates so many investors to purchase real estate in an IRA, but taxes are also one of the biggest causes for concern. If the IRA rules and regulations aren’t closely followed, you can trigger a taxable event

How To Setup a Self-Directed IRA (SDIRA)

You can streamline the process of investing in real estate with an SDIRA by following these steps.

Step 1: Do Your Due Diligence

Once you’ve identified a real estate investment opportunity, consult with a licensed financial professional or certified public accountant (CPA) with experience handling real estate. An experienced CPA can walk you through the initial steps to ensure you can afford the property and reliably remain compliant with IRS rules and regulations.

Step 2: Find A Self-Directed IRA Custodian

You won’t be able to open a self-directed IRA at your local Fidelity or Charles Schwab. Instead, you’re going to have to shop around for the best alternative asset IRA custodian. These are companies that allow account holders to purchase a range of assets that traditional IRA brokerages don’t allow, such as real estate, precious metals, and cryptocurrencies.

The types of assets you can invest in varies by custodian, so make sure you research each qualified trustee to ensure they permit real estate holdings. Not every IRA custodian holds every asset class and some may require “accredited” status before investing in certain high-risk assets.

Step 3: File a Direction of Investment

Your next step is to file a Direction of Investment (DOI) form with your chosen custodian. This form contains all the necessary information regarding where the funds are being sent, and how much money is being invested. A signed DOI informs the custodian or trustee of the investment you want to make, as you cannot personally make the investment yourself per IRS rules and regulations.

To fund your SDIRA, you can rollover holdings in your 401(k) or an existing IRA for free within a 12-month period. Note that individuals have a maximum of sixty (60) days from the receipt of an eligible rollover distribution to deposit the funds into the self-directed IRA at no cost.

When filing a DOI for a real estate acquisition, you must append all other relevant documentation associated with the purchase, including:

- Purchase Agreement

- Preliminary Title Report

- Deed

- Lease Agreement(s)

- Signed Property Manager Agreement

- Signed Property Manager Release Agreement

Step 4: Manage Your Investment

Once the property is purchased, all property-related expenses must be paid through the IRA. Likewise, all rental income derived from the property must be channeled back into the IRA and not into your personal account. It’s imperative that your personal accounts and your IRA be kept completely separated.

Remember that performing repairs on your IRA-owned property is considered a prohibited transaction. You must hire property managers or handymen to perform repairs, renovations, or general upkeep and maintenance using funds from your IRA.

Step 5: Develop an Exit Strategy

The choice is yours whether you want to lease your property in perpetuity or sell the investment later down the road. No matter your intention for the investment, it’s the responsibility of your self-directed IRA custodian or account trustee to process the lease of the units or sale of the property on your behalf.

When the property is eventually sold, the asset is removed from the IRA and is replaced with the income generated by the sale. Before closing on the sale of the property, do your due diligence and consult with a qualified financial professional and a real estate attorney.

The Tax Risk Of Using An IRA To Buy Real Estate

Purchasing real estate with an IRA has its share of risks. First among them is the risk of incurring an IRA “over-contribution” penalty. In the event that the property needs a major repair or emergency upgrade, it’s necessary that the funds in the IRA cover the cost.

What happens if the necessary repairs are so extensive that they drain the cash reserves in your IRA? Suddenly, you have to contribute more cash to your IRA to cover the rest of the costs. However, the IRS only permits contributions of $6,000 per year to an IRA ($7,000 if you’re over the age of 50).

Source: Midatlantic IRA

In this situation, you’re forced to contribute over the IRS-sanctioned limit. An IRA over-contribution triggers a 6% excise tax on the over-limit contribution for every year that it vests in the IRA. Therefore, a high-maintenance period might require you to over-contribute $50,000 to your IRA, which would cost $3,000 in excise taxes.

Keep in mind the opportunity cost of withdrawing funds from an IRA to cover miscellaneous expenses. Every dollar withdrawn from an IRA and spent on upkeep is a dollar that cannot grow tax-free within the account in the years ahead. A $10,000 withdrawal today can amount to a $50,000 future-value loss over two decades.

Establishing a Limited Liability Company (LLC)

In some cases, setting up a limited liability company (LLC) or other corporate entity is the best course of action for couples or investment partners who otherwise couldn’t afford to purchase real estate independently.

Let’s take the example of a married couple who want to purchase an investment property for $200k. Partner A has $150k in their Roth IRA and Partner B has $100k in theirs. In each of their savings accounts, they have an additional $100k in cash.

Neither Partner A nor B can afford to independently purchase the property. If they were to pool $100k from each of their IRA balances in a registered LLC with 50/50 ownership between them, they could purchase the asset in full.

Now let’s say you generate $10k in annual investment income from the rental property. The rental income would be tax-free to both IRAs. As your rental income grows in a tax-sheltered environment, you can leverage out more properties using non-recourse loans under multiple LLCs.

Before setting up an LLC, always render the services of a qualified professional. Doing so on your own would constitute a prohibited transaction because you’re a disqualified party. This would dissolve both of your IRAs. To avoid that, consult the services of a licensed attorney to set up a real estate LLC via a self-directed IRA.

Key Takeaways for Responsible SDIRA Real Estate Investing

Let’s take a minute to review the rules and regulations that govern self-directed IRA real estate investing as well as other need-to-know aspects of buying IRA-owned rental properties.

- Real estate held in an IRA must function solely as an investment property and cannot be lived in or utilized by you or any lineal descendants

- All property-related expenses must be paid through the IRA and not out of the account holders’ pocket

- Rent checks must be made out to the IRA custodian or trustee and not the personal account holder

- SDIRAs cannot be used to purchase property already owned by yourself or a lineal descendant

- Property management, maintenance work and repairs must be carried out by property managers or third-party contractors

- Carefully vet each real estate IRA custodian to ensure they offer the services you need to purchase investment properties tax-free

Is It Worth It To Invest in Real Estate With An SDIRA?

Yes, although a self-directed IRA isn’t a unicorn product. While SDIRAs provide a tax-sheltered environment in which to grow your rental income, there are real drawbacks that are enough to make some investors think twice about taking the IRA route.

For instance, you won’t be able to acquire a traditional mortgage to buy real estate in an SDIRA. This is because investors can only utilize non-recourse loans per IRS regulations, which means that the IRA account holder is not personally liable for repayment. In the event that the IRA custodian defaults on their obligations, the collateralized asset (i.e., the property) is repossessed by the lender.

To compensate for the additional risk, lenders often charge higher interest rates on non-recourse loans. It’s not uncommon to see terms such as 65% Loan-to-Value (LTV) at 6.5% over a 20-year mortgage.

Plus, you can forget about sweat equity. You cannot increase the value of your IRA-held home by putting work into it yourself. To prevent a “self-dealing” transaction, you have to contract the work out to a third-party. Not to mention, tax season is made a little more complicated by introducing a 990-T form since, technically speaking, IRAs are considered non-profits, and non-profits with debt-financed assets are subject to ordinary corporate taxes.

The important counterpoint is that if you can flip a house held in an IRA you can profit $50,000 or $100k, for example, completely tax-free. An IRA is the only tool ordinary investors have at their disposal for selling and renting investment properties in a tax-advantaged account. The prospect of six-figure returns on a home sale in a tax-sheltered environment is reason enough for many investors to take the IRA route when buying rental properties.

Ready To Get Started With a Real Estate IRA?

A self-directed IRA lets your investment properties generate passive income on a tax-deferred basis—or, in the case of a Roth IRA, entirely tax-free. But if you don’t abide by IRS regulations regarding self-dealing transactions, you can find your account stripped of its tax-advantaged status.

To reap the benefits of IRA real estate investing, it’s crucial that you take the time to carefully research a trusted third-party custodian to administer your account. To save you some time, we’ve put together a shortlist of our favorite self-directed IRA providers that can set you up with a tax-sheltered account for purchasing real estate, precious metals, and other alternative assets.

Like all alternative assets, real estate is a diversifier and risk-management tool that has a rightful place in most investors’ portfolios. And although real estate is a lot of work, those willing to tough it out find that it pays dividends in the long-run. Ask your financial advisor today about whether a self-directed real estate IRA can set yourself up for an earlier retirement.

The information provided here is not investment, tax or financial advice. You should consult with a licensed CPA and tax attorney for advice concerning your specific situation.

Citations:

http://www.midatlanticira.com/your-2020-contribution-limits/

https://www.sec.gov/news/press-release/2020-191

https://sophisticatedinvestor.com/highly-asymmetric-investments-golden-opportunity-2020-risky/

https://sophisticatedinvestor.com/precious-metals-ira-reviews/

https://www.irs.gov/charities-non-profits/unrelated-business-income-tax

https://www.securitybenefit.com/tax-center/article/how-tax-deferral-works

https://www.law.cornell.edu/uscode/text/26/1031

https://www.hrblock.com/tax-center/income/real-estate/how-to-calculate-cost-basis-for-real-estate/

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.