Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

A 67 year old Asset class

Futures have been around for a long time, in the US the first Futures contracts began trading in soft commodities back in the 1800s, in Japan rice Futures were traded as early as the 1700s. So Managed Futures funds have not been around that long compared to the underlying assets, but for longer than most might think. The first fund was set up by Richard Donchian in 1948 and traded in Commodity Futures using trend following strategies. In recent years investors have begun taking a closer look at these funds in the search of risk & return diversification and as a return enhancer. Due to the ability to trade indifferently long or short positions these funds have the potential to perform well independently of whether there is a Bull or Bear Stock market.

Similarities to Macro Global Hedge Funds

Managed Futures funds, also known as Commodity Trading Advisors (CTAs), have a lot in common with Global Macro Hedge Funds. Both have the possibility of taking long and short positions, they make use of leverage and deal in broad asset markets, such as stock indices, currencies and interest rates. CTAs however use Futures as the vehicle to place their trades and also deal in a variety of Commodities other than Gold and Crude Oil. The Futures markets offer very close bid-offer spreads, transparent pricing and a high degree of liquidity in some markets. Futures exchanges also reduce drastically counter-party risk, as the risk of a third party defaulting is covered by the exchange. Another similarity is the compensation structure. CTAs also usually charge a 1%-2% management fee and an incentive fee between 10% and 20%

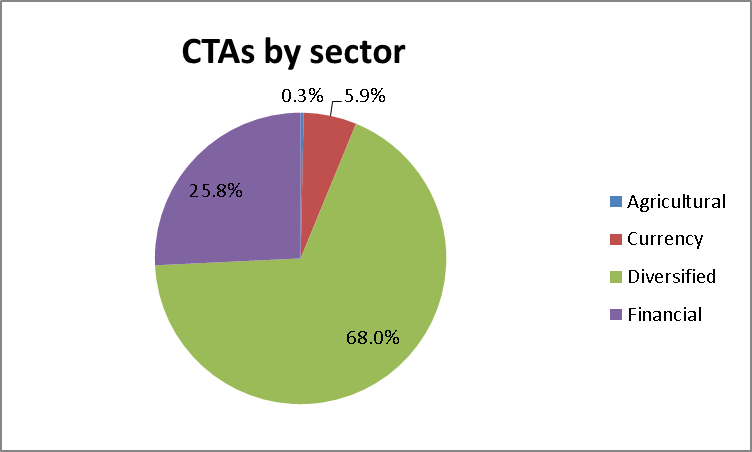

CTAs have come a long way since Donchian established his fund which only traded in Commodities. These funds now trade in a variety of different Futures as new markets have become available also in the financial sector. The chart below shows amounts for CTAs by sector of specialization. We can see that a large majority, 68%, will trade across sectors and define themselves as Diversified.

Data from Barclayhedge,com

Two types of Strategies

Most Managed Futures funds are trend followers, that is the strategy involves defining the on-going main trend and taking positions accordingly. To analyse and establish the current trend CTAs trading strategies adopt either a Systematic or Discretionary system. Systematic strategies make use of algorithms written within computer software, often known as black box trading. These automated trading programs are of course written by humans and are usually back tested on historical market prices, to test their validity, before being used to automate trades with real money. The algorithm may be based on Technical Analysis tools and indicators or may be a proprietary mathematical formula. Discretionary CTAs may also use technical analysis but they also use the managers judgement, knowledge of the market and fundamental analysis to make trading decisions at the manager’s discretion. According to Barclayhedge.com of the CTAs reporting managers defining themselves as discretionary had AUM of $19.1 billion and managers defining themselves as systematic held $306.7 billion, data for Q2 2015.

How can Managed Futures Funds provide Alpha?

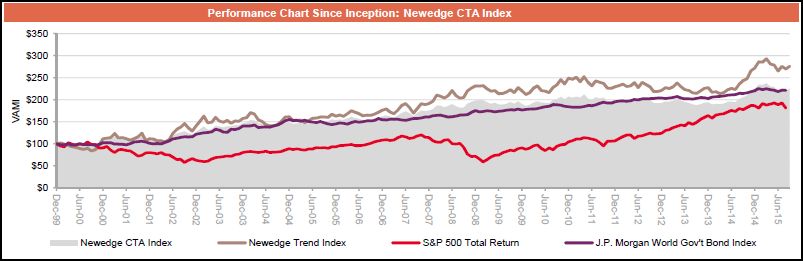

CTAs cannot access returns from the sources of other investments such as illiquidity premiums, or informational or management advantageous edges that can be found in some Hedge Fund strategies or in Private Equity. These managers rely heavily on their skill in timing the market correctly. That is to say they produce Alpha by being on the right side of a market movement at the right time. Of course for every dollar gained by a manager with a position in futures there has to be a dollar lost by another participant holding the other side of the same position. However some participants in Futures markets are not speculators and take positions to hedge physical exposure in the commodity. Producers and consumers are what are known as Natural hedgers of Commodities, they may loose money on their futures position but they may be making it back on their physical positions. This in theory explains the possibility of CTAs generating Alpha despite the issue of Futures being a zero sum game. Ultimately it will depend on the manager’s skill in identifying trends and his/her capacity in mainlining that edge going forward. The same is true for systematic or automated strategies, what worked for the past 6 months or even 6 years may not necessarily continue to work well going forward. Both, discretionary and systematic, trading systems need constant re-evaluation or tweaking to continuously generate Alpha. Not all CTAs will make money all the time, but it would seem that due to the variety of markets traded and the freedom to trade in any direction CTAs may be able to earn consistent returns regardless of the general market regime. The chart below shows the performance of the largest 20 CTAs for AUM that make up the Newedge CTA index since December 1999. To be included in this index CTAs must be open to new investors and report daily balances. Worthy of note is how this basket of CTAs performed well both in the 2001 and 2008 crises.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst