Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Hedge Funds Universe

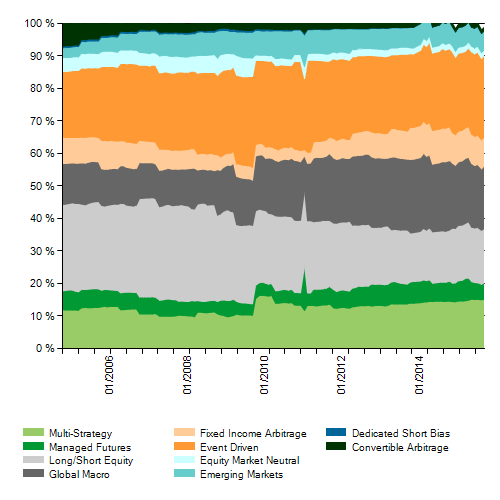

Hedge Funds have a myriad of different types of strategies and it should be well defined and stated in the investment memorandum. There is no official list and even market-wide definitions of styles may vary considerably depending on who is defining the set of strategies. However they are usually divided between, Equity Strategies, Bond Strategies, and Macro Global. I will be using the set of strategies as they are listed in the Credit Suisse Hedge Fund Index. This index incorporates a database of 9000 funds and categorizes the most commonly defined strategies.

Macro Global

This is probably the most well known strategy as funds that were defined as such have often been in the headlines, bringing the attention of the general public to their existence. Macro Global funds have the broadest choice of assets to invest in, usually their investment statement will include the possibility of trading Bonds, Stock Indexes, Currencies and other Over The Counter derivatives as deemed necessary to take advantage of the macroeconomic narrative as determined by the fund manager. They are usually looking at the broad Macro picture and not involved at the Micro level, or Stock picking. The strategy allows for crossing geographical boarders and industry sectors. These fund managers may be able to invest in Europe or other developed areas as well as the USA. In Stocks they may invest in Large Cap or Small Cap, or in Heavy Industries or in Technology. Basically this strategy allows for the widest use of security choice when implementing an investment idea.

Managed Futures

This type of strategy as the name suggests makes use of Futures mainly, many funds will also use FX, where there are usually no restrictions on which sector the fund will trade in. These funds are run by CTAs and again the outlook is global and at the macro level, where these funds may take positions in Grain, Crude Oil, Gold or Foreign Currency. Depending on the mandate they my or not be limited to Futures on domestic exchanges. The strategies followed tend to be systematic and quantitative and often rely heavily on technical analysis tools. This contrasts with Macro Global funds where the focus is usually on fundamental analysis. There may also be Managed Futures funds that use a mix of Fundamental and Technical analysis to define their trading.

Event Driven

This strategy refers to various types of Stock and Bond strategies. The main one is Merger Arbitrage, but it also includes, Distressed Debt, Activist, and multi-strategy. Merger Arbitrage involves trading two stocks that are involved in a merger. If the manager thinks the merger will be successful then the strategy consists of buying the targeted corporation and selling the acquiring corporate’s Stock. Distressed Debt strategy involves buying bonds issued by companies that are currently going through bankruptcy or are about to fall into it. The securities of choice for this strategy are senior bonds or bank loans that have the highest seniority in the case of liquidation and are therefore more likely to recover larger amounts of the face value. Activist strategy looks for companies where the management is not maximizing shareholder wealth. Once shares are acquired then the activism involves obtaining proxy votes from other shareholders to make changes to corporate governance that will maximize share price. The Multi-Strategy fund may combine any of the above strategies, the manager will consider which strategy would be best to pursue given the current economic conditions.

Emerging Markets

As the name suggests this strategy invests in developing countries, amongst which are China, Russia and India. They distinguish themselves from their Emerging Market Mutual Fund counterparts as they can invest in securities other than Stocks. These funds may also take positions in interest rates, bonds, commodities or currencies specializing in one particular country or investing amongst various depending on where the manager sees the greatest opportunities. These funds tend to show higher levels of volatility as the markets they invest in will also be prone to the volatility reflected by the fund.

Short Bias

This is one of the Equity Strategies where these funds are prevalently net short in their exposure to the general market. These funds usually only have positive returns when the market is in a Bear trend and are held in a portfolio as a way of reducing the adverse effects of market crises. This comes at a cost as during Bull trends these funds show negative returns, reducing the overall performance of a portfolio.

Long/Short Equity

The strategy involves combining Long positions with short positions whereby the overall exposure is net long. The manager will attempt to identify Stocks that will out-perform the market and Stocks that will under-perform the market. By being both long and short the strategy seeks to eliminate part of the systematic risk, that is the risk of the broader market, and be exposed for the most part to idiosyncratic risk, which is the individual company risk.

Equity Market Neutral

This strategy seeks to eliminate market risk completely. The manager will identify Stocks that seem under-priced for long positions and Stocks that seem over-priced for short positions. The overall net position to systematic risk will be neutral, however the strategy is not without risk. There is also cross sector risk, the gains from positions in say, Energy stocks, may not be able to out weigh the losses from positions in Transportation stocks, therefore positions are weighted to neutral amongst sectors also.

Convertible Arbitrage

This strategy consists of buying Convertible Bonds and simultaneously selling the Equity of the issuing corporation. Convertible Bonds have a provision that allow the bond holder to convert these bonds into common stock at a set price, similar to a Call option. This arbitrage tries to take advantage of possible miss-priced values in the option feature of these bonds. By being long this type of bond the fund is also long volatility, which is one of the main factors in Option pricing. If volatility increases the strategy will turn a profit as the bond will increase in value. The position is hedged against a fall in stock price which would make the Convertible Bonds loose value as it involves being short Stocks. The manager will seek convertible bonds of corporations that have shares that are easy to borrow for short selling.

Fixed Income Arbitrage

This is a relative value play, the manager will attempt to identify two bonds with characteristics in terms of maturity, rating and yield, that he considers are miss-priced. setting up the trade consists of buying the under valued security and simultaneously selling the overvalued security, in theory the prices of the two bonds will converge to reflect the correct values. Another variation can be selling and buying bonds from the same issuer but with varying maturities, this is called a curve play.

Multi Strategy

This strategy may combine any number of the Equity and Bond strategies, the idea is to offer the investor diversification of strategy risk all in one fund. Usually investors allocate to various strategies, but this can be costly in terms of time commitment and resources in the due diligence process of several funds. In this case these extra costs are mitigated as in theory you may consider one or two multi- strategy funds. Multi-strategy funds attempt to take advantage of their mandate which grants access to various strategies to apply the most profitable given the current economic environment regardless of the underlying main trend. Thereby profiting in Bull and Bear markets of in high or low interest rate regimes.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst