Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Investing in equities and other volatile assets carries a lot of risk. In fact, studies show that about 80% of investors lose money in the stock market. It makes sense, then, why someone might want to become a more conservative investor—by taking risk management precautions, you can hang onto more of your wealth if adverse economic conditions arise.

Unfortunately, there’s no way to eliminate risk in one’s portfolio. Even low-risk assets such as treasury bills, corporate bonds, and even investing in silver and gold carry some degree of risk. Nonetheless, there are steps you can take to reduce your exposure to price volatility, counterparty risks, and market cycle risks.

Being a conservative investor means prioritizing safety and stability over high returns, which can help safeguard your hard-earned money during economic downturns and market volatility. For those looking to prioritize capital preservation and minimize risk, adopting a conservative investment approach is a prudent choice.

In this article, I’ll discuss how you can make adjustments to your portfolio to adopt a more conservative investing strategy.

1. Practice Asset Class Diversification

One of the fundamental principles of conservative investing is diversification. Diversifying your investment portfolio across various asset classes, including the following:

- Defensive equities (e.g., water, gas, and electric utilities)

- Bonds

- Real estate

- Cash and cash-like equivalents

- Physical precious metals

Different asset classes have different risk profiles, and when some perform poorly, others may perform well. This balance can help reduce the overall risk of your portfolio by spreading it around.

For example, during the global financial crisis, the S&P 500 Index fell by 20.1% between October 2007 to October 2010; at the same time, the price of gold rose by 78.9%.

By investing in diverse, non-correlated assets such as precious metals and stocks (rather than exclusively one or the other) you can offset some or perhaps all of the losses incurred by any one asset type. However, the key is to not overcommit to any one asset type by allocating a reasonable percentage of your wealth to each asset class.

2. Choose a Prudent Asset Allocation

Asset allocation involves deciding how much of your portfolio to allocate to different asset classes. Conservative investors typically favor a higher allocation to less volatile assets, such as bonds, commodities, and cash, and a lower allocation to riskier assets like stocks.

Your asset allocation should align with your financial goals, risk tolerance, and investment horizon. Below are examples of asset allocations that might suit conservative investors:

Mid-Term Conservative Investor (Age 45 and Above)

This strategy is suitable for individuals with a longer time horizon and a lower appetite for risk, typically those who are 45 years old and above. The goal is to preserve capital while still achieving moderate growth over the long term.

- Stocks: 40%

- Bonds (Including Treasury Bonds and Corporate Bonds): 40%

- Cash or Cash Equivalents (e.g., Money Market Funds): 10%

- Precious Metals (e.g., Gold and Silver): 10%

Rationale: This allocation aims to provide a degree of growth potential through moderate exposure to stocks while maintaining a significant allocation to bonds for income and stability. The allocation to precious metals acts as a hedge against economic uncertainty and inflation.

Long-Term Conservative Investor (Age 30-45)

This strategy is designed for investors aged 30 to 45, who have a somewhat longer time horizon but still prioritize capital preservation with a moderate level of growth potential.

- Stocks: 45%

- Bonds (Including Treasury Bonds and Corporate Bonds): 35%

- Cash or Cash Equivalents (e.g., Money Market Funds): 10%

- Precious Metals (e.g., Gold and Silver): 10%

Rationale: This allocation increases stock exposure slightly compared to the mid-term strategy, placing a greater emphasis on bonds for stability and income generation. The 10% allocation to precious metals helps maintain a conservative approach.

Short-Term Conservative Investor (Age 60 and Above)

For investors aged 60 and above, capital preservation becomes paramount as they may rely on their investments for income in retirement. This allocation minimizes risk and volatility while providing a stable income.

- Stocks: 15%

- Bonds (Including Treasury Bonds and Corporate Bonds): 60%

- Cash or Cash Equivalents (e.g., Money Market Funds): 10%

- Precious Metals (e.g., Gold and Silver): 15%

Rationale: This allocation is the most conservative, with a reduced allocation to stocks and an increased allocation to bonds and cash. The precious metals component is bumped up to 15% to provide an additional layer of stability, especially during economic downturns.

It’s important to note that these asset allocation strategies are general guidelines, and individual circumstances may warrant adjustments. Conservative investors should regularly review and rebalance their portfolios to ensure they align with their specific financial goals in collaboration with a licensed financial advisor.

3. Focus on Quality Investments

Conservative investors often opt for high-quality, well-established investments. This might mean investing in large-cap stocks with a history of stability, investment-grade bonds, or well-managed real estate properties. Quality investments tend to be less susceptible to extreme fluctuations in value, which can help you preserve your wealth during recessions and other adverse conditions.

4. Look for Income-Generating Investments

Consider investments that provide a steady stream of income, such as dividend-paying stocks and bonds. These income-generating assets can provide a cushion during market downturns and help you meet your financial needs even when your portfolio’s capital value is not appreciating significantly.

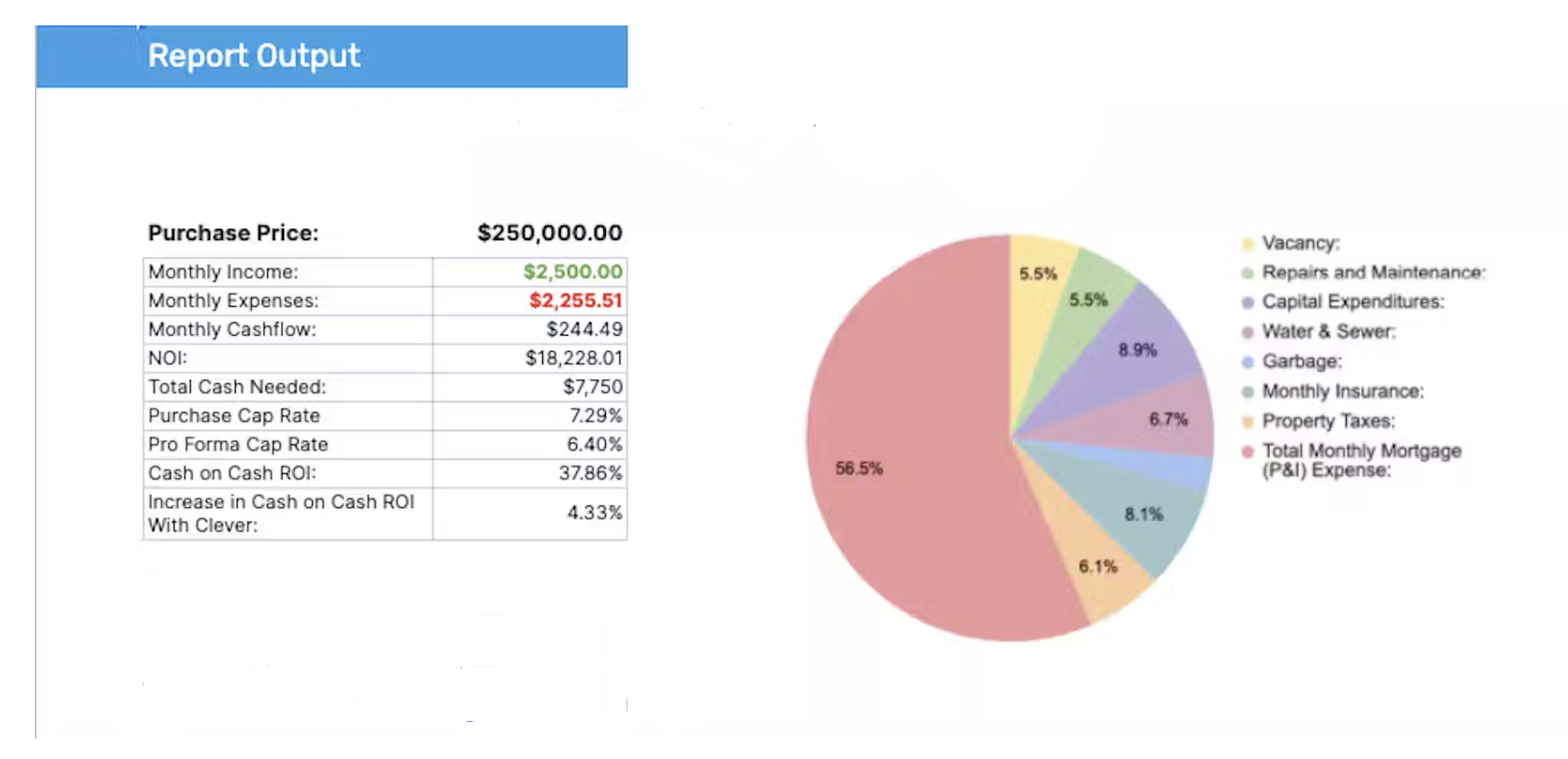

Another classic example of an income-generating investment is a rental property. While real estate markets are known to periodically crash, dedicating a minority percentage of your net worth to income-generating real estate can help you become cash flow positive while diversifying your investment holdings.

An example of a cash-flow positive rental property (Source: Clever Real Estate)

5. Regularly Rebalance Your Portfolio

The weighting in your portfolio will naturally change over time as certain market values rise and fall. To maintain your desired asset allocation and risk level, it’s essential to periodically rebalance your portfolio.

Rebalancing involves selling assets that have performed well and buying assets that may have underperformed. This practice ensures that you don’t become overly exposed to a single asset class. Check out this helpful guide to learn more about portfolio rebalancing.

6. Practice Risk Management through Stop-Loss Orders

If you invest in individual stocks or exchange-traded funds (ETFs), consider using stop-loss orders. A stop-loss order sets a predetermined price at which your investment will be sold automatically. This can help limit potential losses during market downturns.

In essence, a stop-loss order allows you to purchase or liquidate assets at pre-determined prices. Using these tools can help you avoid holding onto assets that have fallen below your acceptable risk threshold. Although stop-loss orders are more commonly used by stock and options traders, conservative investors can and should use them too.

7. Have an Emergency Fund

Having an emergency fund outside of your investment portfolio is crucial for conservative investors. Despite the fact that more than 20% of Americans have no emergency savings, an emergency fund provides a safety net for unexpected expenses and prevents you from needing to sell investments at unfavorable times.

There is no clear consensus as to how much of your wealth you should sock away in an emergency fund. However, some of the leading investors, investment companies, and financial educators insist on the following amounts:

- Vanguard Investments: 3 to 6 months’ worth of expenses

- Dave Ramsey: At least $1,000 cash

- The Motley Fool: 6 times your monthly budget

- MoneyHelper: 3 months’ living expenses

Another major benefit of an emergency fund is that it prevents you from relying on high-interest credit when you need to cover an unexpected expense—something that can save you thousands of dollars in interest payments in the long run.

8. Regularly Monitor Your Investments

Stay informed about your investments and keep an eye on market conditions. Conservative investors should be more risk-averse, so monitoring your portfolio’s performance and making necessary adjustments is essential to maintaining a conservative approach.

As a rule, consider checking in on your portfolio’s performance on at least a once-per-week basis. If your portfolio is losing value over multiple consecutive quarters, consider consulting with a qualified financial advisor.

9. Seek Professional Advice

Speaking of qualified financial advisors, if you’re unsure about how to create and manage a conservative investment portfolio, don’t hesitate to speak with a professional. A financial advisor can help you tailor your investments to your specific financial goals and risk tolerances. If you’re actively preparing for your retirement, it’s even more important to seek outside guidance.

A Conservative Investor is a Principled Investor

Becoming a more conservative investor involves making deliberate choices to prioritize safety and stability in your investment portfolio. By diversifying, allocating assets wisely, focusing on quality investments, and implementing risk management strategies, you can protect your wealth while still pursuing your financial goals.

Remember that conservative investing may not provide the highest returns, but it can offer peace of mind and financial security, which are invaluable in the long run. To help you add value to your portfolio while managing risk, consider opening a self-directed retirement account with one of America’s best gold investment companies.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.