Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Warren Buffet famously said that diversification is protection against ignorance. For Buffet, diversification is like an insurance policy for those of us who don’t have the time, opportunity, or patience to thoroughly research the fundamentals of every stock.

What Buffet describes as ignorance is, in fact, a near-universal. There’s a much higher statistical chance of your investments straying from your predictions than adhering to them. That’s why we insure against the likelihood of our picks failing—to shelter our retirement savings from risk, and to protect against our own fallibility.

Despite what you might have heard, all financial instruments carry risk. However, they vary in kind and in degree. For instance, Vanguard assigns U.S. small-cap stocks a median projected volatility (MPV) of 23% over ten years, whereas the U.S. dollar has a 1% MPV.

That doesn’t mean you should go ahead and store all your wealth in cash. Prudent investors are typically better off spreading their assets across a wide basket of securities, fixed-income assets, cash, and alternatives to enjoy the benefits of concentration (growth) and diversification (risk management) in equal measure.

In this article, I’ll go over the basic principles of diversification and provide a general roadmap to diversifying across asset classes. Note, however, that diversification means different things to different people. Speak with a licensed financial advisor for a diversification strategy that addresses your specific situation.

Diversification Definition: What Is A Diversification Strategy?

A diversification strategy is a method of controlling one’s exposure to financial risk by allocating capital across a mix of asset classes, asset types, and sectors.

There’s no one-size-fits-all approach to risk management. Every investor has a different level of risk they’re willing to accept in their portfolio. Therefore, diversification strategies for retirement investors should be dynamic; varying according to one’s individual tolerance for risk and specific time horizon.

For instance, younger investors have time on their side. When you’re in your 20s and 30s, you might have another thirty or forty years in the labor force ahead of you. This being the case, you won’t need your invested money any time soon and can therefore afford to experiment with higher-risk allocations if you so choose. If your portfolio is hit by a sudden downturn or recession, you have the time to simply wait it out until the next bull market.

If you’re in your 50s or 60s, then you’ve probably got to take a different approach. Since you’re likely thinking about your retirement at this age, it’s important you don’t expose yourself to too much risk. If your portfolio tanks overnight, it could significantly push back your retirement date or negatively impact your quality of life.

Diversification Strategies: Conservative vs. Growth Portfolio Examples

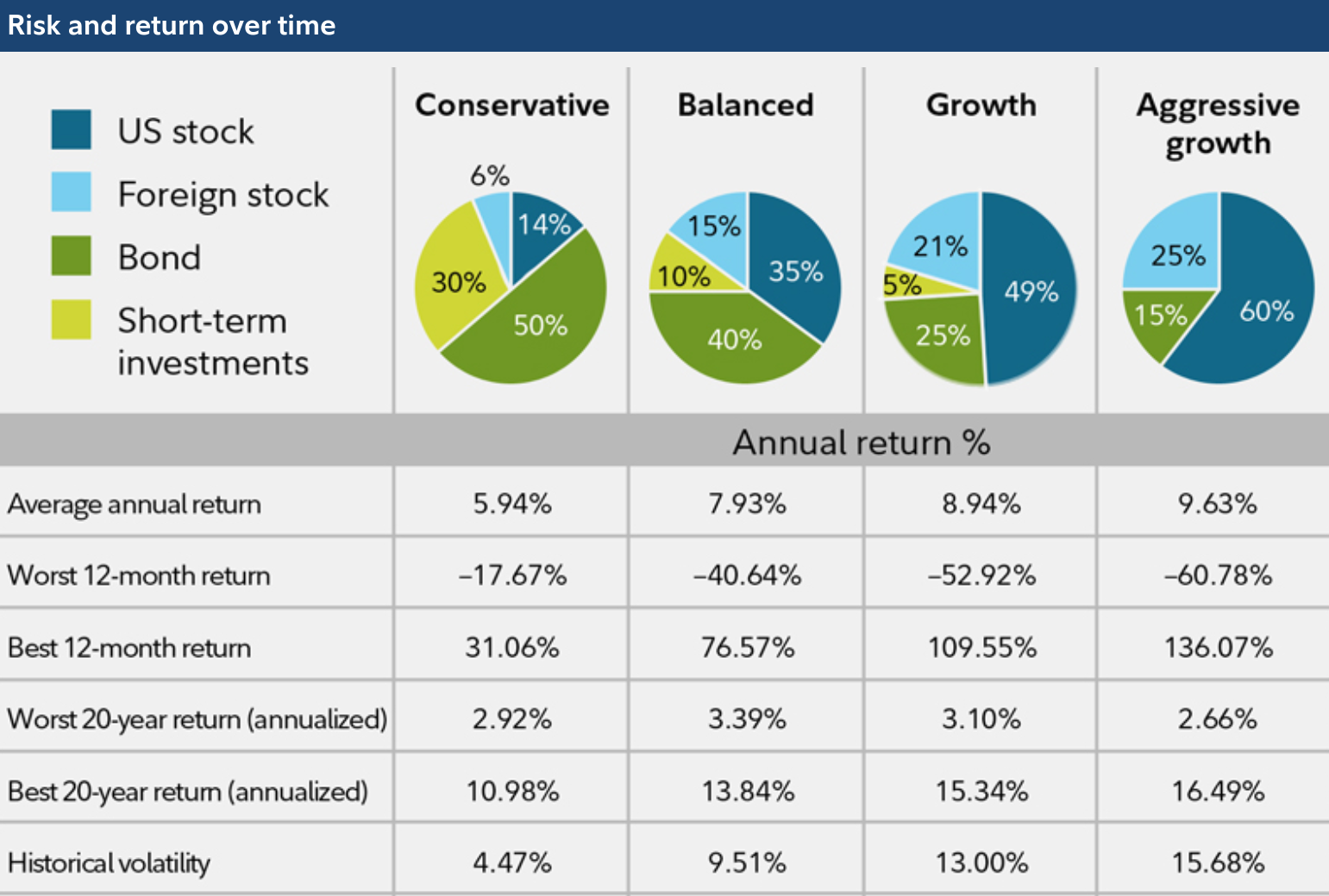

Riskier assets, such as U.S. and foreign equities, tend to offer higher potential rewards. Aggressive portfolios are those which are concentrated in high-volatility assets like equities and cryptocurrencies. Over time, these portfolios elicit much wider swings in value (i.e., -60.78% worst 12-month return) compared to bond-heavy, conservative ones (-17.67%).

The chart below describes the basic composition of four portfolio types ranging from the least to most risky (left to right).

Source: Fidelity Investments (1926-2019)

As an exercise, let’s assume we’ve hit a once-in-a-lifetime 12-month downturn in the market with $100,000 invested. Based on the data above, the Aggressive portfolio would lose $60,780 for an ending balance of $39,220 (-60.78% return). Now you would have to win back 155% of your portfolio value before rising back to your starting balance.

The Conservative portfolio, under the same conditions, would lose $17,670 for an ending balance of $82,330 (-17.67% return). You’d then have to gain 21.5% to get back to your starting point—an uphill battle, no doubt, but 7.2x less steep than it would be had you held an Aggressive portfolio.

Notes on Prudent Diversification

As a general rule, conservative portfolios make a good fit for investors who are fewer than 10 years from retirement. These are the least volatile on average (4.47%) and are built to withstand market shocks better than conservative ones. When the market cycle reverses course, investors with conservative portfolios will need less time to regain their losses.

Balanced portfolios comprise a greater share of stocks and are better suited for investors between 10-20 years from retirement, whereas growth portfolios consist of at least 50% U.S. equities. These are typically held by investors who have another 20 or 30 years until their target retirement date.

Majority-stock portfolios are considered aggressive because they’re highly volatile (15.68% MPV) and generate higher returns and steeper losses on average. These qualities make them a better fit for young investors who haven’t started thinking seriously about their eventual retirement.

Risks of Over-Diversification

At the same time, it would be unwise to diversify to such an extent that you basically become a one-man index fund. The promise of a diversification strategy is that risks can be made manageable by exposing yourself to a variety of non-correlated risks. The downside is that you can miss out on gains particular to a hot asset class or sector.

Whereas weak diversification exposes you to potentially substantial losses, over-diversification blunts the impact of better-performing investments. Between these two extremes is the Goldilocks zone: a properly risk-managed position that benefits equally from diversification and concentration to maximize returns while minimizing risk.

Prudent investors nearing retirement should err on the side of caution. For those planning to retire in the next 10 years or fewer, the luxury of concentration is virtually off the table. This demographic is better suited for a conservative portfolio and retirement diversification strategy with minimal exposure to stocks and equities while investing more heavily in alternatives and cash.

Diversification Definition: 5 Layers of Risk Management

Diversification is multifaceted. It’s not enough to conservatively spread your wealth across equities and fixed-income assets and call it a day. This is because true diversification exists within asset classes, and not merely across them.

Below, I’ve listed the five methods of diversification that can take place simultaneously within one’s portfolio, ordered by depth:

- Asset Class Diversification: Between types of financial instruments, such as stocks, bonds, cash, real estate, cryptocurrencies, and precious metals.

- Intra-Class Diversification: Within categories of financial instruments, such as small-cap, large-cap, mega-cap, emerging market, and U.S. stocks within the equities asset class; protects against firm-specific risk.

- Risk Factor Diversification: Different classes of investments are exposed to different types of risk that drive the return of a particular asset; stocks are vulnerable to equity market risk, while bonds are subject to interest rate risk and currencies are exposed to inflation risk.

- Geographic Diversification: If you’re highly invested in traditional assets, currencies, and real estate, you can avoid “home country bias” by diversifying with international assets purchased on foreign exchanges. In cases such as Japan in the 1990s, asset price bubbles can be specific to one country while financial markets in other countries (e.g., U.S. equity markets) remain largely unaffected.

- Time Diversification: Often referred to as Dollar-Cost Averaging (DCA), time diversification reduces the negative impact of unlucky timing and poor investor discipline. A DCA strategy spreads out the purchase of investments over time (i.e., monthly, bi-weekly) instead of a lump sum, which often leads to better investor behavior and long-term planning instead of short-term guessing.

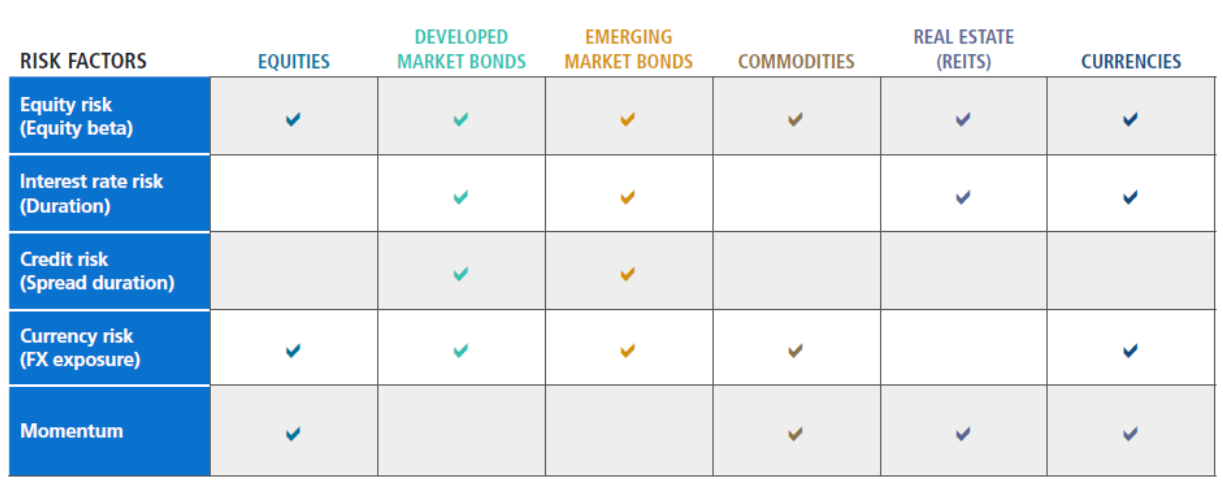

As I touched on earlier, all investments entail risk. However, they vary in kind and duration. To illustrate the importance of diversification, I’ve included a chart below that speaks to the various risks characteristic of traditional asset classes.

Source: PIMCO

It’s impossible to evaluate your total portfolio risk without first understanding the underlying risk factors of each asset class. To deliver the best possible rewards over time, one’s portfolio should have balanced and controlled exposure to all five types of risk.

Risk Categorizations for Deep Diversification

No diversification definition can elude discussion of risk categories. If you’re unfamiliar with the five primary categories of investment risk, I’ve defined each of them below.

- Equity Risk (Equity Beta): The measure of a stock’s volatility versus the market. The expected return on the investment minus the risk-free rate of return equals the equity risk premium.

- Interest Rate Risk (Duration): The risk that a change in interest rates or federal funds rates will change the value of a bond or a variable-rate investment; when interest rates fall, bond prices rise and vice versa.

- Credit Risk (Spread Duration): The potential of loss resulting from failure to repay a loan to a creditor or meet one’s contractual debt obligations.

- Currency/Inflation Risk: Exchange-rate risk resulting from a currency’s loss of value relative to another that can create unexpected losses.

- Momentum: The rate of acceleration of a security’s value, often involved during intra-day trading when swaps, puts, and calls are put on stocks experiencing upward or downward price movement from other traders.

A sound diversification strategy adds uncorrelated types of risk together so that you can keep or increase your expected returns while restraining volatility. The root logic is that the average of two variable risk types produces a weighted average. However, the variance of those variables, once added together, is modified by their correlation. Negatively correlated risks combine to reduce the weighted average risk between them, thus lowering your total portfolio exposure to risk.

Consider opening an IRA or self-directed 401(k) that combines risk types. If you’re all equities, for example, you’re missing important hedges against financial market risk like gold and silver. If you’re all-in on large-cap tech stocks, you’re missing out on hedges against sectoral risk like utilities or insurance equities.

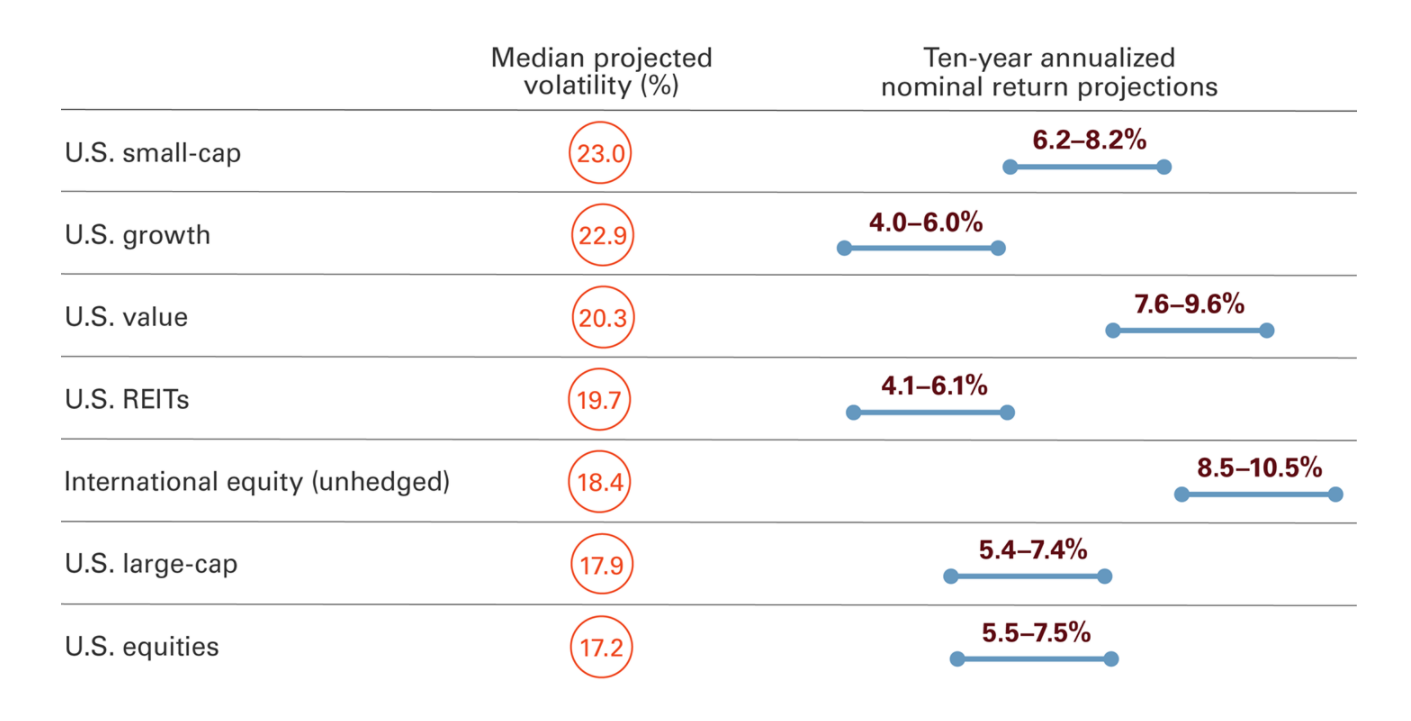

Risk Allocation of Traditional Assets

The chart below demonstrates how traditional securities vary in their estimated risk and reward profiles. Investing in a variety of asset types helps mitigate the risk of more volatile assets (e.g., U.S. small-cap) while also enjoying the growth potential of high-upside investments (e.g., unhedged international equities).

Source: Vanguard

Note that Vanguard’s MPVs and projected returns are hypothetical in nature and the result of simulations. Real-world results will vary.

As demonstrated above, U.S. and international equities are relatively volatile assets that have the potential to generate high returns. For their upside potential, they often comprise a large percentage of portfolios belonging to younger risk-tolerant investors. Those of us who are thinking about retirement should consider taking a different approach that involves a variety of assets non-correlated with equities.

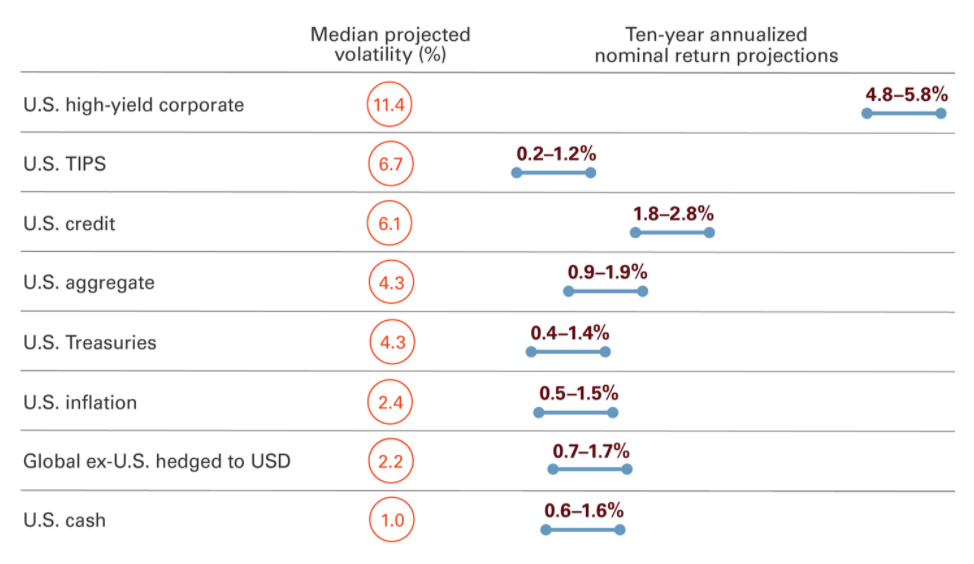

Source: Vanguard

The chart above depicts a variety of alternative assets that share little correlation to the stock market. Noticeably, they have much lower MPV values and, in turn, also significantly lower annualized return projections. Since they involve separate types of risk as compared to equities—namely, interest rate and currency risks—they would make for useful diversifiers in a stock-heavy portfolio.

The Role of Alternatives in a Diversified Retirement Portfolio

Alternative investments are classified as those other than equities, bonds, or cash. Gold bullion, a quintessential alternative asset, has a low correlation (approximately ~0.25) to the stock market, which makes it extremely useful as a hedge in more aggressive portfolios.

Alternatives are typically characterized by low liquidity, which means they cannot be bought and sold as quickly as stocks listed on a global exchange. For that reason, they’re significantly more resistant to volatility brought on by knee-jerk investor behavior.

There are numerous reasons why retirement investors should consider including alternatives in their diversification strategy, such as:

- Potentially higher portfolio-wide aggregate yields

- Risk management resulting from low equity market correlation

- Access to a broader menu of investment opportunities

- Lower liquidity acts as a safeguard against market crashes

The fact is, you can dampen volatility by investing in alternatives at any stage in your investing career—whether you’re eighteen or eighty years of age. Alternatives such as silver and gold bullion, real assets, REITs and REIT index funds, annuities, and even cryptocurrencies IRAs including Bitcoin and Ethereum can protect your wealth during adverse interest events or stock market downturn. That is, as long as they represent a small portion of your total wealth.

Diversification: Your Best Defense Against Risk

When it comes to your retirement savings, you can’t afford to have your portfolio overexposed to any one type of risk. As the saying goes, you shouldn’t put all your eggs in one basket. Remember, diversifying means more than divvying up wealth between assets—it’s also about spreading risk across and within assets. Failing to diversify could cost you your life savings during the next market crash.

This is true, but your diversification strategy shouldn’t simply mirror the next guy’s. Take Warren Buffet, who owns 70 private companies outright and has studied their fundamentals inside and out. Buffet’s idea of diversification is out of reach for those of us who rely on piecemeal stocks and bonds.

Deep diversification requires more than just traditional securities. It’s not enough to put a chunk of our portfolio into government bonds and call it a day. True risk management calls for diversifying beyond traditional assets and into alternatives uncorrelated with the stock market, such as precious metals, annuities, and real estate.

To get started with your investing diversification strategy, check out our list of the best annuity companies. Fixed annuities provide guaranteed fixed-income payments over a period of time, so they don’t carry equity risk or volatility. For greater upside potential and a hedge against stock market volatility, we recommend going a step further and reading our review of the best precious metals IRA providers.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.