Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

A real estate investment trust (REIT) is like an index fund for residential, commercial, and industrial real estate. Managed by professionals, REITs let investors land a dividend-paying inflation hedge without the stress of being a landlord and the obligations that come with having your name on the deed.

For risk-conscious investors, a REIT index like the Schwab US REIT ETF—with $4.6B in assets under management—provides diversified and highly liquid exposure to the real estate market. Thanks to their dividend yields, they’re also long-term options for investors seeking passive income.

REIT indices are an excellent first step into the otherwise complicated world of real estate investing. But before you get started, there are a few things you absolutely must know before you consider diversifying your portfolio with a REIT or REIT index.

What Is A REIT / REIT Index?

REITs are essentially pass-through entities similar to LLCs or S Corporations. Those who buy shares in REITs are known as “unitholders” to whom the fund managers must pay at least 90% of their net income in the form of distributions—functionally, but not taxably, equivalent to dividends.

Like with corporate stocks, REIT unitholders have a proportional interest in the underlying asset of the real estate as well as the distribution income.

REITs generate income from monthly rents paid by tenants. Since the prices of real estate rise with inflation, REITs are often effective as an inflation hedge and a portfolio diversifier against the stock market.

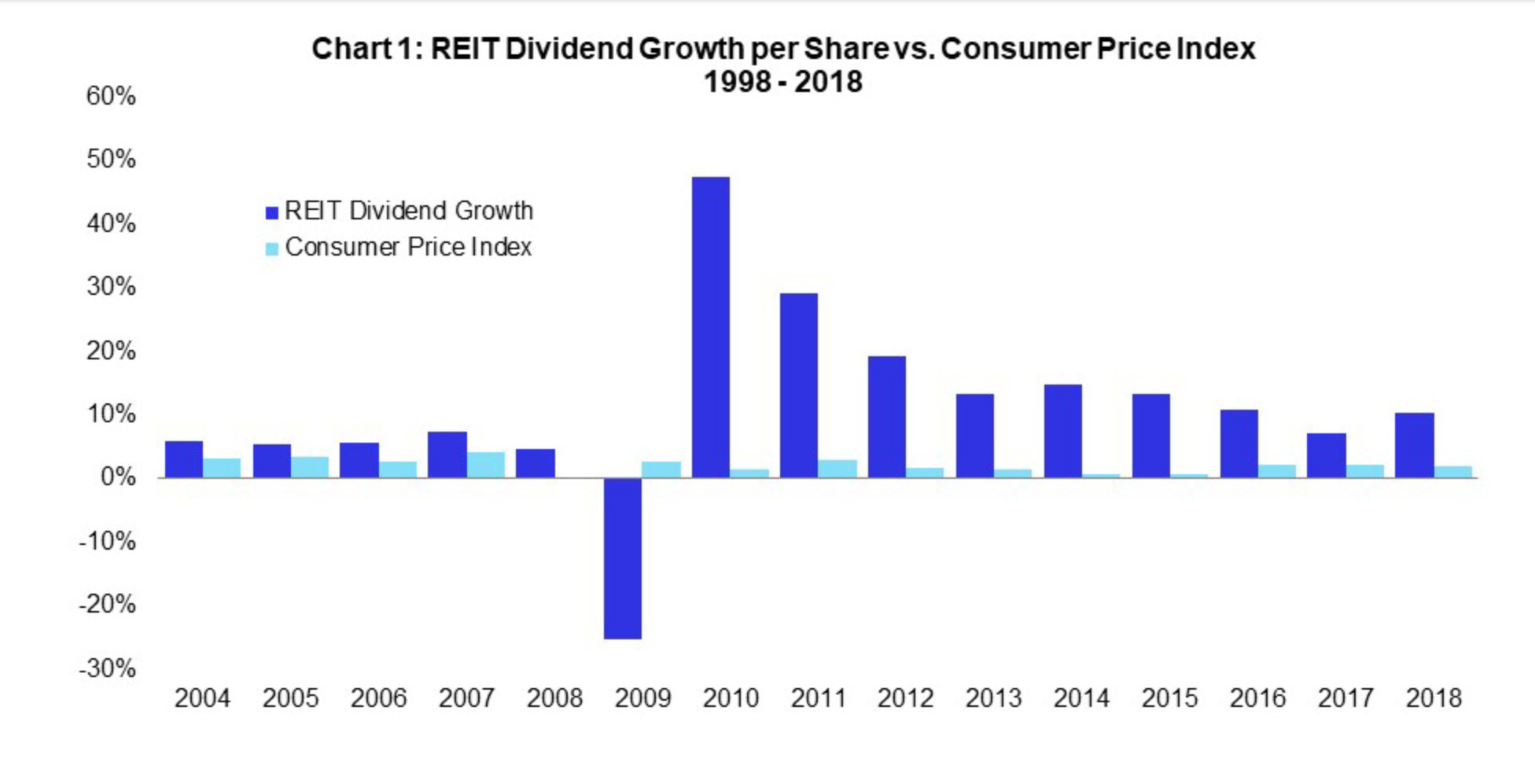

Source: NAREIT

Above, we have a direct comparison of REIT dividend growth per share and the inflation rate (CPI). Since 1998, all but two years have seen REIT market-wide growth per-share outpace the CPI. This is largely caused by real estate rents increasing when the general prices of goods and services increase since, generally, leases are tied to inflation.

Historically, REITs are excellent performers with total returns that rival the S&P 500 over long time horizons. For instance, the Vanguard Real Estate ETF total returns in 2019 was +13.3% versus the S&P’s 9.4%. The downside is that a real estate market crash, like in the late-2000s, could have an outsized negative effect on your portfolio’s performance. Less so, however, than if you had invested in individual REITs or real estate properties.

Examples of a REIT Index

Although there aren’t any publicly-traded REITs that brand themselves as “indices” per se, there are several mutual funds that track equity REITs. The first that comes to mind is the Vanguard Real Estate (VGSIX) mutual fund, which is a de facto broad index of various cross-sector REITs with holdings in commercial US real estate, including:

- American Tower Corp.

- Vanguard Real Estate II Index Fund

- Crown Castle International Corp.

- Digital Realty Trust Inc.

- Simon Property Group Inc.

The largest composite index tracking the REIT market is the Dow Jones Equity All REIT. This index has a balanced weighting structure such that no single company can comprise more than 10% of the index’s value and that the aggregate weight of all companies weighing more than 4.5% cannot exceed 22.5%. This allows the fund to get around the “top-heavy” issue that impacts REIT indices, as many of the world’s largest REITs take up a disproportionate share of many major indices, which poses diversification problems and greater vulnerability to market crashes.

A few other notable examples of U.S.-based REIT indices include REET Global REIT ($2.5B), iShares Mortgage Real Estate ($1.6B), and Schwab US REIT ($4.4B). These are low-fee (.07-.15% ERs) benchmarks that are tethered to the performance of public REITs and their local equivalents in developed, emerging, and US markets. In Canada, the PRO Real Estate Investment Trust (PRV.UN) is one of the better-performing REITs on the market. To date, it’s up about +22.5% since January 2016, despite suffering a massive crash in March 2020 that more than halved its value.

REIT index funds and ETFs provide widespread coverage of REITs as an asset class. In effect, they make it easier to jump into REIT investing without having to spend as much time on investment research. All told, REIT indexes like the VGSIX provide risk-managed real estate exposure for laissez-faire investors who otherwise wouldn’t be able to afford a diversified real estate portfolio on their own.

The Risks of REITs

Like any asset class, REITs have their share of risks and trade-offs. Due diligence is paramount before investing in a REIT or an index that tracks the market. Below, I’ve listed a few of the most common trade-offs associated with these assets.

Information Asymmetry

By their nature, a REIT index is a diversified basket of real estate holdings across various sectors and industries. Investing in individual REITs, however, entails risks when the unitholder cannot research each holding with the REIT’s portfolio to verify whether they can generate rental income in the long-term.

Interest Rate Risk

In a rising interest rate environment, REIT demand is reduced as unitholders sell off their shares and flock to safer income plays like bonds and U.S. Treasuries. At the same time, a rising rate environment usually signals a strong, expanding economy which is associated with higher occupancy rates that, in turn, command higher rent prices.

Variation in Holdings

An issue unique to REITs is that their risk profiles differ greatly depending on the geographical locations and functional specializations in which the fund is invested.

Given current market conditions, REITs specializing in healthcare, residential properties, or industrial or e-commerce storage spaces are less risky than, say, retail or mall REITs. There are also special-purpose REITs that should be examined on a case-by-case basis to determine whether they’re viable long-term holds, such as those in:

- Student housing

- Gas stations

- Telecommunications towers

- Public self-storage

It’s also important to be mindful of the distinction between equity and mortgage REITs. The former are involved in real property, whereas the latter invest in mortgages, mortgage-backed securities, and other derivative investments that can pose a greater risk.

Capital Appreciation

A REIT index isn’t going to help the capital appreciation problem that’s inherent to this asset class. Consistent income, not capital appreciation, is the main selling point of REITs and REIT indices.

For instance, the share price of iShares S&P/TSX Capped REIT Index (XRE.TO) has only increased a little over 10% since 2006. With REITs, you’re simply not going to see much capital appreciation because they’re obliged to payout 90% of their net income to unitholders, leaving little cash left behind to reinvest in the business.

Source: Yahoo Finance

The capital appreciation issue is important to understand before getting involved in REITs. If the trust’s management isn’t effective in deploying capital, the per-share metrics might stagnate far behind other investment vehicles like stocks and mutual funds.

Fees and Expense Ratios

REITs charge unitholders fees upfront, which can reach as high as 15% in some cases. When external managers are brought on board, expense ratios upwards of 0.5% are not uncommon, as is the case with iShares Residential Real Estate (0.48%). Check the management fees of the REITs an index is invested in to make sure you’re not overpaying for your exposure.

Dividend Tax Events

Unlike dividends on a stock, REIT distributions are taxed as ordinary income. For some, this can trigger a sizable tax event that far exceeds dividend tax rates or the capital gains rate. For more favorable tax treatment, consider investing in REITs or REIT indices through a tax-sheltered investment account like a self-directed 401(k) or IRA.

What Is Unit Dilution in REITs?

One of the major draws of a REIT index is that it partially circumvents the dilution effect. When you invest in an individual REIT, you run the risk of the fund managers issuing more units and, in doing so, diluting the relative interest of each unitholder’s share in the REIT. Conceptually, dilution risk in REITs is a lot like inflation risk in currencies.

REITs sometimes dilute stock intentionally as a way of raising capital. Given that REITs must distribute at least 90% of their net income to unitholders, dilution is a natural effect of the trust model. This effect greatly limits REIT share price appreciation.

Investing in a broad number of REITs through an index fund lets investors diversify their holdings across multiple trusts with varying track records of dilution.

The Benefits of a REIT Index

REIT indexes pose a number of benefits to retail investors who otherwise wouldn’t have the capital to make gainful investments in real estate. Aside from getting around capital constraints, I’ve listed a few other notable benefits to REIT index investing below.

Competitive Returns

As we’ve already touched on, the top REIT index funds are major performers and are one of the few assets that regularly match or outpace the growth of the S&P 500. Although their per-share growth is nothing to write home about, their dividends are extremely competitive—for example, the Dow Jones Equity All REIT boasts annualized returns of 9.46% since inception.

Portfolio Diversification and Risk Management

A REIT index is a vital tool for managing risk in one’s portfolio. Financial research published in the Journal of Real Estate Portfolio Management by Chaudhry et al. found that REITs have “at least two cointegrating vectors” with energy-related assets like crude oil, but have few, if any, linkages with the broader stock market. This means that REITs can act as a hedge against volatility in the equities market while providing greater returns than conventional fixed-income securities like government bonds.

Liquidity (Private vs. Public REITs)

A key difference between a private REIT and a public REIT index is their respective liquidity. If you’re in a publicly-traded REIT and want out, you can sell it as you would a mutual fund or security. However, private REITs leave you open to difficulties with closing your position because they’re illiquid.

Let’s say you’re invested in a private REIT but want to cash out your position. In a non-traded REIT, there might not be a potential buyer available with whom you can make a transaction. By contrast, REIT indices are highly liquid securities that can be bought or sold within minutes on public exchanges like any index fund.

The Bottom Line

Investing in a REIT index gives you diversified access to the real estate market without having to deal with the stress or costs of property management. Plus, there’s a handsome dividend payout. If your REIT holdings are kept in a self-directed IRA, you get to hang onto 15-30% more of your dividend income per annum until you withdraw during your retirement. This, of course, assumes you will be in a lower tax bracket during retirement age.

Self-directed investors looking for lower-risk, passive exposure to real estate might want to consider allocating a small portion (i.e., <5%) of their portfolio to REITs. Investors more interested in buying, selling, and swapping, are probably better off sticking to regular stocks or other alternatives like gold, silver, and cryptocurrency.

Ultimately, if you’re going to use a REIT index to make a real estate play, consider doing so within a tax-advantaged retirement account. This way, the dividends earned on your REIT aren’t subject to taxation every year as ordinary income. To get started, check out our list of the best self-directed IRA companies offering some of the lowest fees and full checkbook control of your assets.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.