Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

If you’ve been reading about retirement investing strategies, you’ve probably heard of the so-called 4% rule by now. For over two decades, this concept has dominated the conversation around optimizing retirement savings withdrawals.

Proponents of the 4% rule insist that it can make your money go further during your retirement, allowing you to maintain your lifestyle deep into your old age. Detractors aren’t so optimistic. Some even allege that the 4% rule can leave you penniless and desperate at an age when you’re the most vulnerable.

In a nutshell, the 4% rule is a simple guideline to prevent retirees from running out of money in their non-working years. For many of us, outliving our savings is our biggest concern during retirement age; for some, the 4% rule helps keep these anxieties at bay.

There are valid cases both for and against the 4% rule. In this article, I’ll go over both sides of the debate to parse out whether it’s in your interest to follow it or not during retirement.

The Origin of the 4% Rule: The Trinity Study

When you retire, your financial goals shift. In a matter of months, you stop trying to “beat the market” and you start trying to secure a steady income for life. But it’s not easy determining how much money you need, and how much you should withdraw every year, in order to not blow through your retirement savings.

Fortunately, researchers have crunched the numbers so we don’t have to. In 1998, three senior professors from Trinity University published what’s now known simply as the “Trinity study”. The authors took a stab at the following question: What is a sustainable withdrawal rate during retirement?

The Trinity Study: Methodology

The study analyzed a variety of retirement withdrawal rates to find those that allowed the highest quality of life without putting the retiree at risk of running out of money. Retroactively, they looked at several portfolios consisting of various allocations of stocks and fixed-income assets at multiple withdrawal rates between 1925 and 1995.

For this time period, they used the S&P 500 index to represent stock market performance, and the fixed-income component of their model portfolios consisted entirely of high-grade corporate bonds. One limitation of the study is that they did not account for taxes or withdrawal fees.

The authors counted any portfolio with money left over at the end of the investor’s forecasted payout period to be successful.

The Trinity Study: Results

In Table 1 (below) displays the outcomes of withdrawal rates applied to various portfolio compositions. These are not simulated data, but actualized, real-life outcomes as calculated using historical S&P 500 records.

Here you can see that, for example, a four percent withdrawal rate is successful 100% of the time under nearly all payout periods. Notably, there are exceptions for all-stock portfolios (i.e., very high risk), which have a 98% success rate for payout periods between 20 and 30 years; likewise, there’s a 98% chance of success for 75/25 stock-bond portfolios over a 30-year time horizon. Still, I’d take those chances.

Table 1. Source: AAII Journal

Note that Table 1 doesn’t account for inflation. If an investor were factoring in inflation, they would adjust the amount of money they withdraw from their savings every year. This way, differences in purchasing power are leveled out and one doesn’t run the risk of being functionally poorer (i.e., being able to afford fewer things) on the same income.

Let’s assume an average annual inflation rate of 3% and a starting withdrawal of $35,000 on Year 1. If you kept your withdrawals constant and inflated-unadjusted, the real value of your withdrawal would reduce to $33,950 in Year 2. By Year 10, your withdrawal would only have the purchasing power of $26,608 during Year 1.

Diminishing Purchasing Power @ 3% Projected Inflation

The list below demonstrates the importance of using inflation-adjusted figures when calculating your retirement withdrawal rate. Over time, the real value of your withdrawal will diminish to such an extent that it becomes unsustainable to live on.

- Year 1: $35,000

- Year 10: $26,608

- Year 15: $22,849

- Year 20: $19,621

- Year 25: $16,849

- Year 30: $14,469

If you assume that an annual withdrawal of $35,000 is sufficient for covering your basic needs and expenses during retirement, you have to adjust for inflation. Otherwise, the purchasing power of your withdrawal will be less than half of your Year 1 starting point by Year 25 and only 41.3% by Year 30.

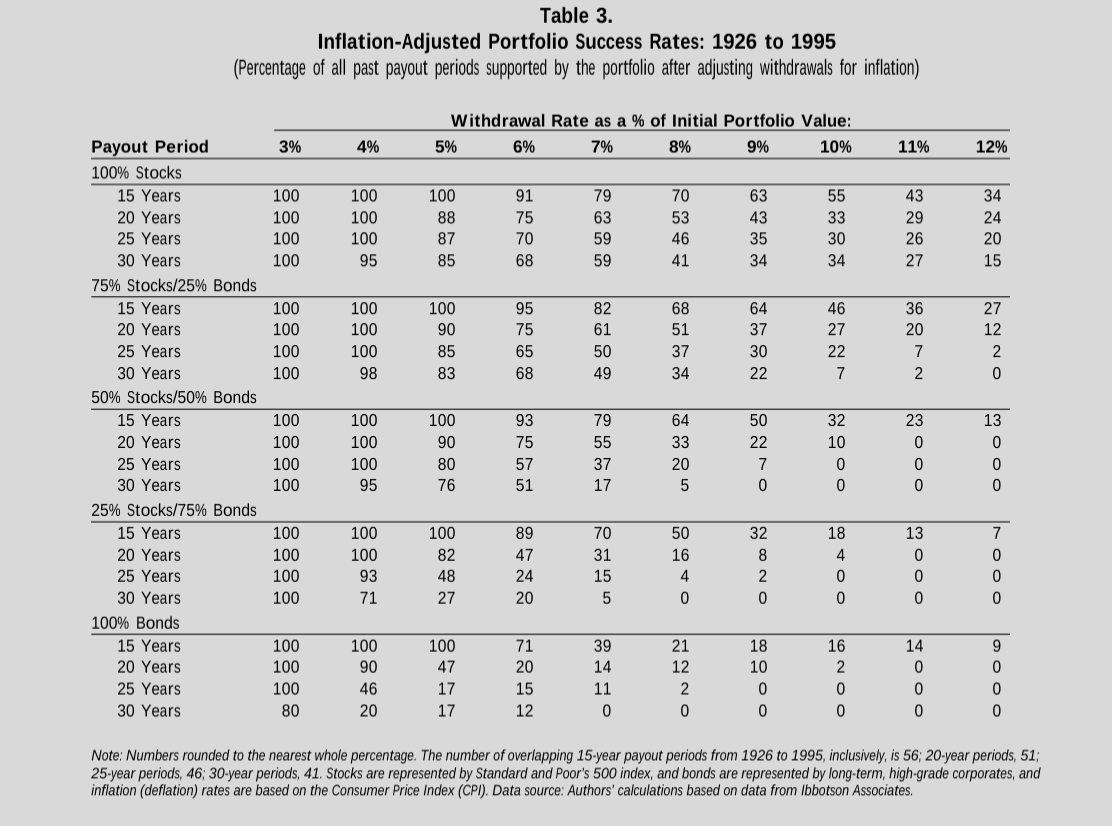

Inflation-Adjusted Trinity Study Results

When we adjust for inflation, we get a different set of results. In Table 2, the Trinity study finds that success rates go down somewhat after making these adjustments. However, the changes aren’t drastic.

For example, the success rate of a 75/25 stock-bond portfolio after 30 years still has a 98% success rate. A more conservative portfolio with a 50/50 stock-bond profile will succeed 95% of the time after 30 years and 100% of the time after 25 years.

In other words, you can increase your withdrawal amount from a risky or conservative portfolio every year to match inflation and still guarantee a successful 25-year retirement.

Table 2. Source: AAII Journal

If we take our projected 3% annual inflation rate and adjust our withdrawals accordingly, we arrive at steadily increasing figures year over year. If we assume a baseline withdrawal of $40,000 for the first year of retirement, the following years look like this:

- Year 2: $41,200

- Year 5: $45,020

- Year 10: $52,191

- Year 15: $60,504

Suddenly, your retirement doesn’t seem so penny-pinched, does it? By scaling up your withdrawal amount you ensure that you give yourself enough to live on such that your standard of living after 20 years is no different than the day you retired.

The Basic 4% Rule Formula

Now that we know that the 4% rule works, let’s take a closer look at how you can apply it to your retirement strategy in practical terms. The 4% rule formula (or, should we say fourmula?) follows a relatively simple procedure:

- Withdraw 4% of your initial nest egg (i.e., $40,000)

- Adjust for the consumer price index (CPI)

- Withdraw the adjusted sum at the start of Year 2 ($41,200)

- Ensure that you withdraw from the initial value of the portfolio, and not the present value after the assets appreciate or depreciate over time

- Repeat initial steps, adjusting the previous year’s withdrawal amount by the real rate of inflation (or CPI)

Pay close attention to the fact that withdrawal amounts are based on the initial portfolio value and do not change as its value fluctuates year over year.

What Inflation Rate Should We Assume (2%, 3%?)

You might argue that we’re making less-than-optimistic assumptions about inflation. And I can’t blame you, considering most other 4% rule formulas seem to assume a 2% inflation rate. However, I would caution against using this figure, since the average annualized inflation rate in the United States since 1960 currently sits at 3.1%.

Although this doesn’t sound like much, at that rate prices would double every 30 years. If you want an accurate financial forecast, your withdrawal projections should reflect this 3% rate, which is supported by historical market data.

Is The 4% Rule (Still) Legit in 2021?

The Trinity Study was first published 23 years ago—not exactly yesterday. Naturally, a lot of investors are skeptical about whether the data collected over two decades ago still holds true today.

An independent analysis from Royal Bank of Canada’s (RBC) Wealth Management division found that the 4% rule is still sustainable across a variety of retirement horizons, even up to 40 years post-retirement. The chart below finds that even after a whopping 40-year retirement, the 4% rule succeeds 86% of the time with a half-stock, half-bond portfolio and 92% of the time with a 75/25 composition.

Source: RBC Wealth Management

The RBC study provided a much-needed update on the 1998 Trinity study by including returns and inflation data up to 2014. Since retirees are living longer today than they were even two decades ago, and now retiring earlier in the post-pandemic era, RBC’s second look at the data is timely.

The results assure us that even in the aftermath of the global financial crisis, we can still safely retire for four decades by living off 4% of our nest egg each year.

Is The 4% Rate Too Conservative? A Second Look at the Data

Notice how quickly these numbers plummet as soon as you start withdrawing more. At a 5% withdrawal rate, suddenly a safe bet (86% success rate) turns into a dangerous move (42%) on a 40-year horizon in a 50/50 portfolio. The same is true of a 35-year retirement, where a near-guaranteed 96% rate falls to a risky 56% under the same stock-bond allocation.

This tells us that, despite its many detractors, the four percent rule is not “too conservative” for many investors. This is especially pertinent for young retirees or the devotees of the FIRE (“financial independence, retire early”) movement, who have to plan ahead for many decades on a fixed income. If you start withdrawing more than 4%, you might be playing with a different kind of fire.

Why The 4% Rule Might Not Be Your Friend

Just because the Trinity Study proved that the 4% rule works, doesn’t mean you necessarily have to follow it. As I mentioned earlier, the 4% rule has its share of detractors.

One of them is Princeton Economics Professor Wafe D. Pfau, who conducted his own self-published update on the Trinity study in 2010. He concluded that the 4% rule was essentially unsafe in a low-yield bond environment. Using Monte Carlo simulations with data gathered across 17 countries, Pfau found that the best success probability is actually 87% across all allocations over 30 years.

Another is author Michael Kitces, Head of Planning Strategy at Buckingham Wealth Partners, who believes that the 4% rule hasn’t held up since the crash of the early-2000s tech bubble. Since the Trinity study doesn’t account for additional income sources, such as Social Security or pensions, Kitces finds it too conservative and likely to preserve a huge amount of money after the retiree’s death—that is, barring a Depression-scale economic meltdown.

Trinity Study & RBC 4% Rule: Methodological Issues & Notes

Readers should be aware that the four percent rule, perhaps naively, only considers portfolio allocations containing stocks and traditional bonds. Since many retirement investors diversify with alternative assets, the Trinity study’s findings may not be representative of the average retirement investor.

Additionally, neither Trinity nor RBC’s studies factor in the service fees that many retirement account administrators charge for withdrawals. These fees force retirees to burn through their savings at a faster rate. (For a list of low-fee or no-fee retirement account providers, check out our top-recommended IRA companies.)

It’s also worth pointing out that the Trinity study and the RBC follow-up are backward-looking. Like all studies that work with historical market data, there’s no guarantee that past results will carry forward into the future.

Financial markets are not totally predictable, and therefore any claim to a “100% success rate” should be taken lightly. The applicability of these findings (from Trinity, RBC, and Pfau) depends on the future stock and bond markets performing in a way that matches the historical record.

Dying Rich: The Problem With The 4% Rule?

For some, the four percent rule errs a bit too far on the side of caution. In very few cases do you end up with no money left over after 30 years of retirement by following the rule with a stock-heavy portfolio. Often, you end up with more money than you started with. If you’re wondering how, consider the example below.

Let’s assume you have an all-equities portfolio invested entirely in the S&P 500 Index ($SPX), a collection of the 500 largest publicly traded U.S. companies. Since 1971, the annualized real return (AAR) of the $SPX is 6.8%.

For simplicity’s sake, we’ll use a base AAR of 7% for our example. Let’s also assume you’ve built a retirement nest egg of $1 million. Following the 4% rule would have you withdraw $40,000 ($1,000,000x[0.04]) on Year 1, leaving you with a remainder of $960,000 to vest in the index and accrue value.

Taking the Example Further

Over the next 12 months, we can expect your $960k to grow by 7%, thus bringing your nest egg’s value to $1,027,200 by the start of Year 2 ($960,000x[0.07]). But now we have to adjust our next withdrawal for inflation, giving us a Year 2 income of $41,200 ($40,000x[1.03]). Once withdrawn from our account balance, we’re left with $986,000 which, after a year in the market, appreciates to $1,055,020 ($986,000x[1.07]).

You’ll notice that the portfolio’s value is already trending up. Even with the occasional down year added to the mix, portfolios tracking the $SPX will follow this trendline for the duration of the owner’s retirement.

Therefore, if we assume normal market conditions year after year, the 4% rule should leave retirees wealthier at the end of their retirement than at its start. Whether you view this negatively or positively might depend on whether you have children and the size of the estate you wish to leave them. For many, enjoying their hard-earned money in retirement is more important than dying with an inheritable fortune.

Should You Use The 4% Rule?

The 4% rule can be used as a useful rule of thumb for retirement planning. It can be used to roughly calculate how much money you might need to last a certain number of years without working, but should still be treated flexibly. Remember that nobody lives out their retirement in a vacuum. Life changes, spending requirements change, and adverse market events can throw a wrench in even the best laid plans.

All told, the 4% rule does skew conservative. At its best, it’s a safe rule for helping retirees avoid running out of money. At its worst, it encourages a miserly retirement, setting up investors to die with a pile of cash that they never got the chance to enjoy.

Ultimately, your retirement withdrawal rate will depend on your risk tolerance, time horizon, and the composition of your portfolio. While dying with too much money isn’t a bad problem to have, at the same time every retiree deserves to enjoy the fruits of their labor. For those planning a 30-to-40 year retirement, the 4% rule is a mathematically sound way to ensure this right is preserved without risking financial insecurity.

How long do you think you can make your money stretch in retirement? To stretch it even further, consider speaking to your financial advisor about diversifying your portfolio with alternative assets like real estate or annuities, or even a precious metals IRA. This way, you can hang onto more of your retirement income during the next stock market downturn.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.