Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

It doesn’t matter whether you’re late to the game or if you’re still in college, it’s never too late or too early to invest for your retirement. But no matter how young you feel, your retirement investing strategy has to reflect your age.

Your exposure to risk should scale down the closer you get to retirement. While a 20-something can weather the storm in the event of a sudden market downturn, a 60-year-old nearing retirement can’t afford such luxuries. You should consider these limitations when choosing the kinds of assets in which you invest.

For those of you considering opening a self-directed IRA or 401(k) for your retirement planning, I’ve put together a comprehensive guide to get you started. While this doesn’t constitute investment advice, it does provide general information aggregated from various investing authorities to help you decide, with a financial advisor, how to best manage your retirement investing strategy.

Disclosure: I’m not a financial advisor. The information provided herein is not investment or financial advice. You should consult with a licensed professional for advice regarding your specific situation before investing your money.

Retirement Investing Strategy: The Foundations

Above all, it’s crucial that you exercise due diligence and be cautious when coming up with a retirement investment plan. Don’t be fooled by money-making schemes looking to profit from your ignorance. There’s no shortage of them in the DIY finance space. Instead, stick to proven principles that have lasted the test of time.

The methods of investing have changed since Benjamin Graham’s The Intelligent Investor was first published in the 1940s, but the underlying principles have remained. Here’s a non-exhaustive list of foundational principles you should consider if you want to take a sensible, self-directed approach to long-term financial investing:

- Buy and Hold: Don’t invest without the expectation of making a short-term return. Plus, the longer you go without selling, the longer you hold off on paying tax on your capital gains.

- Avoid Fees: Choose an investment platform that doesn’t charge fees or commissions, like Robinhood in the U.S., or QuestTrade or Wealthsimple in Canada.

- Diversify: Don’t over-concentrate in a single asset class, no matter how appealing, like mega-cap tech or healthcare stocks. Past performance is not indicative of future results.

- Consider ETFs: To play it safe, consider investing in broad economy-wide ETFs or market indexes, like the Vanguard S&P 500 ETF (VOO) or iShares Russell 2000 ETF (IWM), which are baskets of securities that track the top 500 and 2,000 U.S. equities, respectively.

- Exercise Restraint: Don’t panic sell when a temporary event in the news cycle makes the market react. Time in the market is more important than timing the market.

- Avoid Daytrading: Both gains and losses on trading activity are subject to taxation, and every transaction must be recorded so you don’t misreport your income at tax time. Most day traders lose money, and are not as successful as the S&P 500 in the long run—index investing is almost always the safer and more lucrative approach.

Adhering to the principles above can help secure, but doesn’t guarantee, sustainable long-term returns. A sound retirement investing strategy is one that is predicated on time-tested principles such as those outlined above, but should ultimately be made in conjugation with a financial advisor.

Understanding Asset Classes & Correlations

Your options aren’t limited to stocks when it comes to financial investing. There are multiple asset classes, each with its own risk-reward profile.

Asset classes behave uniquely depending on the overall health of the economy and the general level of confidence held by investors. For example, times of economic uncertainty and disruption usually prompt a decline in the stock market as investors liquidate their positions and seek stability in precious metals or government bonds.

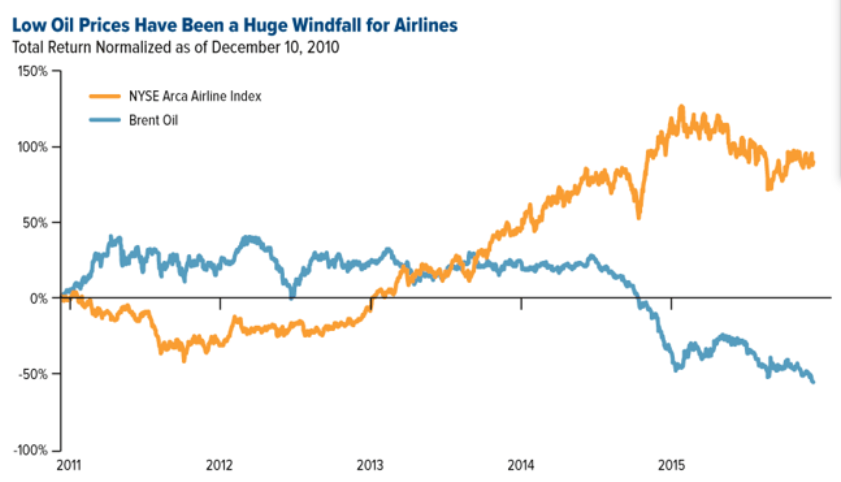

Correlations measure the degree to which movement in one variable reliably predicts movement in another. In some cases, assets share a negative correlation, which means Asset A’s movement in one direction leads to movement in the opposite direction for Asset B. For instance, two assets that have recently shared a negative correlation are airline stocks and oil prices, as depicted below:

Source: SeekingAlpha

Why is this important? Because negative correlations in financial markets teach us a basic yet crucial lesson about diversification. When constructing an investment portfolio, the inclusion of negatively correlated assets protects against volatility across the portfolio as a whole.

Losses incurred by one asset are offset by gains made in another. In this sense, negative correlations are the essence of hedging and can stabilize your portfolio over time.

Other examples of assets that often, but not always, share a negative correlation include:

- Gold and the S&P 500 or DJIA

- Gold and the U.S. dollar

- Insurance payoffs

- EUR/USD to USD/CHF

Success in retirement investing depends on your ability to practice sound risk management. As I’ll explain later, your portfolio’s risk tolerance should scale with age toward more risk-averse allocations. As you age, you should gradually minimize your exposure to risk by dedicating a greater share of your portfolio to negatively correlated assets.

Asset Allocation and Balancing

As I discussed above, it becomes increasingly important to include negatively correlated assets in your portfolio the closer you get to retirement age. There are a vast number of assets you can invest in, each with varying levels of liquidity and risks, including:

- Individual stocks

- Mutual funds

- Exchange-traded funds (ETFs)

- Municipal and private bonds

- Government bonds

- Money market funds and certificates of deposit (CDs)

- Real estate

- Cryptocurrencies

- Precious metals

- Fine art

- Royalty trusts

- Convertibles

- Preferred shares

I’ll stop there, because I could spend all day listing the myriad sub-categories of each individual asset class. The point is, there are many stores of value available to investors looking to spread their wealth around, and entrusting only one of them with your money leaves you vulnerable to steep losses if an investment performs poorly.

A well-diversified retirement investment strategy includes a combination of asset classes weighted as a share of their overall wealth. It’s inadvisable to go all-in on one asset type because doing so could end up squandering your wealth in the event that the asset class collapses.

Just as it’s important to diversify your diet—no matter the short-term returns of pizza and ice cream—it’s equally important to diversify your shopping cart with various asset types.

If you’re like me, you might break down your monthly grocery budget 30/30/25/15 between meat, fruits and veggies, dairy, and snack foods. Think of your portfolio the same way, where you have a predetermined allocation dedicated to each of the four main asset types.

Equities

Equities, or stocks, are shares in a company. They represent an ownership stake in a private corporation and its profits, and are bought and sold on public stock exchanges like the TSX, NYSE, and NASDAQ.

Stocks have a higher risk-reward profile than other traditional assets. The average annualized return in the stock market is about 10%, or about 7.5% after adjusting for inflation. Therefore, a $10,000 contribution in the stock market would be worth about $20,600 in real terms after 10 years.

Source: PoliticalCalculations

The chart above depicts the rolling monthly average of the S&P 500, a standard benchmark of the U.S. equities market, over a roughly 150-year time horizon. Investments in the stock market are generally marked by periods of rapid returns followed by precipitous declines—a pattern known as boom and bust market cyclicality.

The volatility of the stock market makes it a risky short-term investment, but its general uptrend in the long-run handsomely rewards investors who have long time horizons. As such, young investors who aren’t yet considering retirement often hold a stock-heavy portfolio, composed, in large part, of individual stocks, mutual funds, index funds, and ETFs.

Bonds

A bond is a debt obligation that acts like an I.O.U., whereby an investor lends to a borrower a principal sum that’s repaid with interest by a determined end date. They are a form of corporate or government debt issued to finance projects and expenses.

As a fixed-income security, bonds are less volatile than stocks, thus they are more widely sought after by older investors who are nearer to their retirement. The average annualized return of a government bond is about 5-6% without adjusting for inflation.

Bonds can be issued by private corporations (corporate bonds) or sovereign governments (government bonds). The latter is considered less risky because they’re backed by the full faith and credit of the United States government. Bonds do, however, carry the risk of declining in value in a high interest rate environment.

Cash and Equivalents

Risk-averse investors often hold a portion of their portfolio in cash and cash-like equivalents. These assets are considered the safest because they aren’t subject to the same market forces as equities and most cash equivalents are guaranteed by the federal government, such as:

- Treasury bills

- Certificates of deposit

- Money market deposit accounts

- Savings deposits

The downside is that these assets garner the lowest returns and are subject to inflation risk, or the threat of the inflation rate (e.g., 1.8% in 2019) outpacing your investment returns. Generally, the chances of losing money with a cash equivalent is very low. Thus, they’re often staples of conservative investors near retirement age.

Alternatives

Alternative assets such as precious metals, real estate, annuities, and cryptocurrencies, are non-traditional financial investments that can be used to diversify your portfolio. Not unlike stocks and bonds, most alternatives can be included in a tax-advantaged retirement savings plan, like a 401(k), IRA, or a 457 plan.

Investments in alternative assets mitigate portfolio volatility, minimize transaction costs over time, and may be subject to lower long-term capital gains taxes if held for longer than 12 months. Moreover, the chart below demonstrates the low correlation (<.65) between the stock market (S&P 500) and alternatives such as currencies, commodities, and real estate (REITs).

Source: Guggenheim Investments

Liquidity is often a drawback to alternatives, as these assets usually take some time to sell on an exchange or marketplace. However, illiquid alternatives, like real estate, gold, or silver, have the benefit of being resistant to knee-jerk reactions by the investing public—thus, they’re less exposed to volatility and rapid price swings.

Taken together, the unique properties of alternative assets—including illiquidity, scarcity, and market non-correlation—make them powerful diversifiers for investors of all ages and risk tolerances. This, in part, explains why alternatives like gold have skyrocketed in value in today’s uncertain market. In Q3 2020, global investment demand for gold eclipsed 494.6 tonnes, about 21% higher than Q3 2019.

Recalibrating Your Portfolio

As your investments grow over time, your portfolio will need to be periodically rebalanced to maintain your diversification targets.

To illustrate the necessity of rebalancing, let’s take the example of a simple $200 portfolio with a 50/50 allocation evenly between Stock A ($100) and Bond B ($100). If Stock A appreciates by 25% and Bond B goes down by 15%, then you now have a $125 and $85 position.

Now, your allocation is no longer 50/50, but closer to 60/40. If you want to maintain your former portfolio allocation for risk management purposes, you’re going to have to sell $20 of Stock A and buy an additional $20 of Bond B. This way, you’re back to a 50/50 allocation in a portfolio now worth $210 after having realized 5% returns.

Remember that past performance is not indicative of future results. Although it may seem counterintuitive to “sell winners and buy losers”, doing otherwise would bias your portfolio toward one industry, sector, or asset type and therefore expose it to more risk.

Periodically reallocating your wealth lets you maintain your diversification targets as your portfolio changes with time. This is a necessary tenet of risk management that often goes overlooked by investors caught up in the success of their best-performing assets.

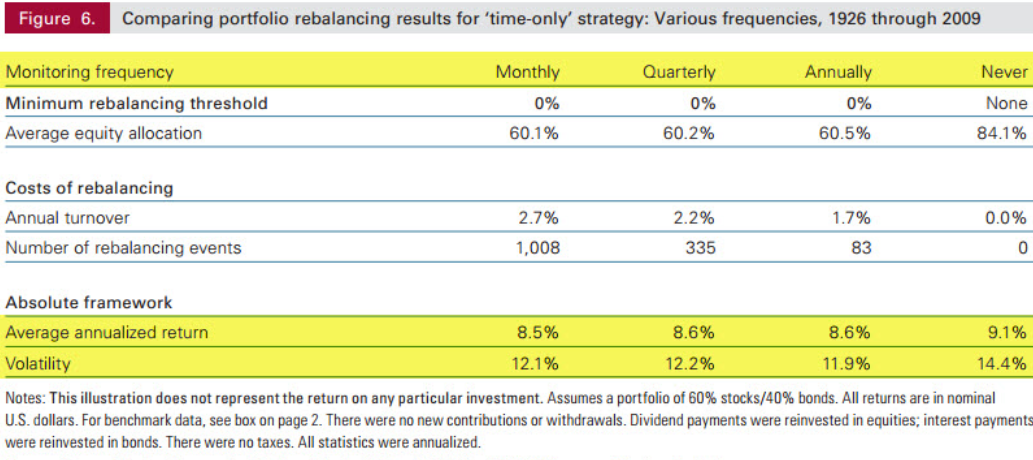

Threshold-Based Reallocation

Some investors set a threshold variance (e.g., 5%, 10%) that, if crossed by any asset, automatically triggers a rebalancing event. For example, if the total weight of stocks in one’s portfolio exceeds more than 5% above or below its target allocation, they or their broker will have to buy or sell a portion of their stock holdings to bring it in line with their target.

Source: ETF Guide

The chart above demonstrates the trade-offs of a heavily rebalanced portfolio. The lower your threshold, the more rebalances you’ll need to make, which will eat into your returns in the form of brokerage transaction fees. As depicted above, a threshold that triggers one rebalancing per year elicits lower volatility (11.9%) and annualized returns in keeping with S&P 500 benchmarks (8.6%). Therefore, a once-a-year rebalancing strategy might obtain the best results for risk-conscious investors who don’t want to compromise on their returns.

Understanding Time Horizons

As an investor, your youth is your most valuable asset. But even if your retirement is in sight, it’s important that you understand how long your money expects to grow

A time horizon is the allotment of time you expect to hold an investment in order to reach a specific goal. The longer your time horizon, you more risk you can assume in your investment portfolio as the extra time lets you recover from any short-run downswings in the market.

If you’re 27 years old and intend to invest until you reach the full retirement benefit age of 67, you have an expected time horizon of 40 years (67-27). That allows your initial investment to accrue compound returns over four decades. In that span, $1,000 will have turned to over $18,000 (depicted below) if we assume the average rate of returns in the $SPY (7.5%).

Investors less than ten years from retirement don’t have the luxury of multi-decade compounding returns, nor the ability to weather the storm if the market turns south. For this reason, older investors would do well to take a more conservative approach by allocating more of their portfolio to fixed-income securities and alternative assets such as precious metals.

Utilizing a 401(k), IRA, or Roth IRA

Active investors who want to pick and choose the assets they invest in should consider opening a self-directed 401(k) or IRA. These are tax-sheltered investment accounts that let your assets appreciate in value tax-free. One key difference between these two accounts is that 401(k)s are offered by employers and often include a company contribution match.

Within either self-directed retirement account, investors can purchase traditional or conventional assets and enjoy tax-deferred growth. For example, I’ve written a guide to self directed IRAs and real estate if you want to learn more about buying investment properties on a tax-deferred basis.

If you expect to earn significantly more later in your career, it might be in your interest to opt for a Roth IRA, which consists of after-tax dollars. With a Roth IRA/401(k), you’re taxed now—when you’re presumably paying less in income taxes—and can withdraw later in life completely tax-free.

Investing outside of an IRA or 401(k) will trigger tax events as your investments in brokerage accounts are subject to short-term or long-term capital gains taxes. For this reason, it’s always a good idea to first max out your IRA or 401(k) before opting for a brokerage.

How To Get Started Investing for Retirement

Traditionally, investing for one’s retirement started with opening an IRA with a brokerage like Charles Schwab, Fidelity, or TD Ameritrade. The problem with standard brokerage accounts is that they aren’t self-directed, so you won’t have full authority regarding which assets can be included. Plus, you’ll be on the hook for brokerage fees and commissions.

If you want to get started with active investing where you pick and choose the asset classes to add to your portfolio, check out this list of the top IRS-approved self-directed IRA vendors.

Alternatively, mobile apps such as Robinhood, Stash, and Acorns provide an intuitive, low-barrier entry point for investors looking to gain exposure to stocks. However, these platforms are limited in scope. For instance, you can’t invest in any stock that isn’t listed on the NYSE/NASDAQ (e.g., Nintendo, Samsung, or Tencent), you can’t invest in alternative assets, and you can’t buy government or corporate bonds.

Keep in mind that there are no capital requirements for investing. Start investing for retirement today, regardless of your income level, even if only with a nominal sum ($25-50) to learn the fundamentals and to watch your money grow with time.

Retirement Investing Strategy By Age: 20s-50s

There’s no one-size-fits-all approach to retirement investing. Above all else, your age and risk tolerance determine your investing strategy. Below, I’ve listed standard asset allocations by age group that can be as templates for novice investors starting from scratch.

Retirement Investing In Your 20s

At this age, you’re in the beginning stages of retirement planning and can afford to assume more risk than older investors nearer to their retirement.

- Stocks: 80-90%

- Bonds: 5-10%

- C&E: 0%

- Alternatives: 5-15%

Retirement Investing In Your 30s

As a thirty-something, you’re young enough to invest in a stock-heavy portfolio and assume a higher degree of risk while still enjoying the benefits of long-term compounding. However, at this age, most investors start dedicating a much larger share of their discretionary income to retirement investing.

- Stocks: 65-80%

- Bonds: 10-20%

- C&E: 0%

- Alternatives: 10-25%

Retirement Investing In Your 40s

For added safety in your forties, consider allocating a greater share of your portfolio to bonds and alternatives. At the midpoint in your career, investing in a more diverse array of non-correlated assets can protect your wealth from volatility as you approach retirement.

- Stocks: 50-70%

- Bonds: 15-30%

- C&E: 5-10%

- Alternatives: 10-30%

Retirement Investing In Your 50s

In your fifties and sixties, dedicating much more of your portfolio to cash and equivalents, as well as bonds and safe haven alternatives like precious metals, can help you retire on time. Having too much of your wealth tied up in equities makes your portfolio vulnerable to market downturns that can delay your retirement by years.

- Stocks: 30-40%

- Bonds: 25-35%

- C&E: 10-20%

- Alternatives: 15-35%

Don’t Wait—Start Retirement Investing Today

A successful retirement investing strategy hinges on your ability to diversify and mitigate your exposure to risk. By now you know that there’s no such thing as an optimal investment strategy. The right solution for you depends on your age, nearness to retirement, and personal circumstance.

If your retirement is looming on the horizon, consider opening a self-directed precious metals IRA today. Your holdings aren’t limited to gold and silver—and can include stocks, bonds, and even real estate—but you’ll be glad you have the option in the event of a sudden market crash. Historically, gold and silver hold their value during recessions, which makes them a crucial safe haven for investors getting close to retirement age.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.