Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Only a slim majority of Americans—55%, in fact—own stocks. For many U.S. homeowners, their house is their only retirement investment to speak of. If you find yourself among the roughly one-half of Americans who are underinvested in financial markets, now’s the time to get started.

I’ve put together an “investing for dummies” guide to help you responsibly invest your capital into diverse financial markets, including equities, alternatives, and fixed-income assets. This way, you can better prepare yourself for your retirement and set yourself up for a more secure financial future.

Stock Investing for Dummies: What Is Financial Investing?

Financial investing is the practice of strategically allocating money with the expectation of earning a positive return over time. In other words, an investment is something you buy now with the expectation of one day getting more for it than you originally paid.

A financial investment need not be stocks, bonds, or mutual funds. There’s a wide variety of asset classes, both traditional and not, in which an investor can allocate their capital. In fact, most investing strategies incorporate a diverse mix of assets in order to better manage risk in their portfolio, including the following:

- Cash

- Real commodities (e.g., precious metals, crude oil, copper)

- Fixed-income securities

- Hedge funds and ETFs

- Real estate

- Collectibles (e.g. fine art, wine, watches)

- Cryptocurrencies

There’s a whopping $6.2 trillion worth of alternative assets actively managed in the global marketplace. Among all the world’s institutional investors, including top hedge funds and multinational banks, 79% have some portion of their portfolio in alternatives.

In short, financial investing is the art (and science) of managing wealth across assets in order to manage risk and earn a profit. And when it comes to stock investing for dummies, the first rule of thumb is that diversification is essential to success in the majority of cases. Otherwise, you’re overexposing yourself to unnecessary risk.

The 7 Basic Principles of Investing for Dummies

Now that we understand the fundamental premise of financial investing, let’s take a closer look. Below, we’ve listed ten of the most important principles of investing for dummies (i.e., total beginners—don’t take it personally!).

1. Open a Roth or Traditional IRA

Before you get started building your portfolio, you need an investment account that will hold your stocks, bonds, and other assets. Your best options are tax-advantaged savings accounts such as a Roth IRA or a Traditional IRA.

Although both accounts offer tax advantages to account holders, assets held within a Roth IRA are already taxed, and therefore appreciate entirely tax-free. Traditional IRAs consist of pre-tax dollars and are therefore subject to taxation upon withdrawal.

Generally, investors should opt for a Roth IRA if they’re younger and expect to be in a higher tax bracket when they start making withdrawals during retirement. This way, your money will be taxed at a lower marginal tax rate.

2. Choose a Self-Directed IRA or a Brokerage Account

Whether you select an IRA offered by a brokerage firm, such as Vanguard or Fidelity Investments, or a self-directed IRA depends on your goals. If you want a “hands-off” investing process in which you relinquish a great deal of control to a third party, a brokerage account might be the better option for you.

Independent investors who want full freedom and control over their investment decisions may want a self-directed IRA (or “SDIRA”). These account types offer the same tax benefits as regular IRAs, but do not involve a middleman, like Charles Shwab or Vanguard, managing your wealth on your behalf.

SDIRAs allow investors to hold a variety of alternative asset types that are off-limits to brokerage investors, such as:

- Real estate (i.e., held within an LLC)

- Precious metals bullion and coinage

- Certain altcoin cryptocurrencies

- Hedge fund shares

- Tax liens, debt, and private placements

- Annuities and secondary market annuities

You have to apply for a self-directed IRA through an official SDIRA custodian company. For more information about SDIRAs, and how they can open up a world of potential investment options, check out our guide to self-directed IRAs.

3. Invest in Safe Bets and Blue-Chip Assets

Certain asset types are more secure than others according to their historical performance. Index funds that track a diverse basket of securities (i.e., fungible financial instruments) tend to perform well over time and net reliably positive returns in the long run.

For example, the S&P 500 fund is a benchmark index tracking America’s 500 largest publicly traded companies. Any investor can buy a share of the S&P 500 fund, each of which represents a small ownership stake in each of the companies held within the fund—these include mega-cap firms such as Amazon, Walmart, and Apple.

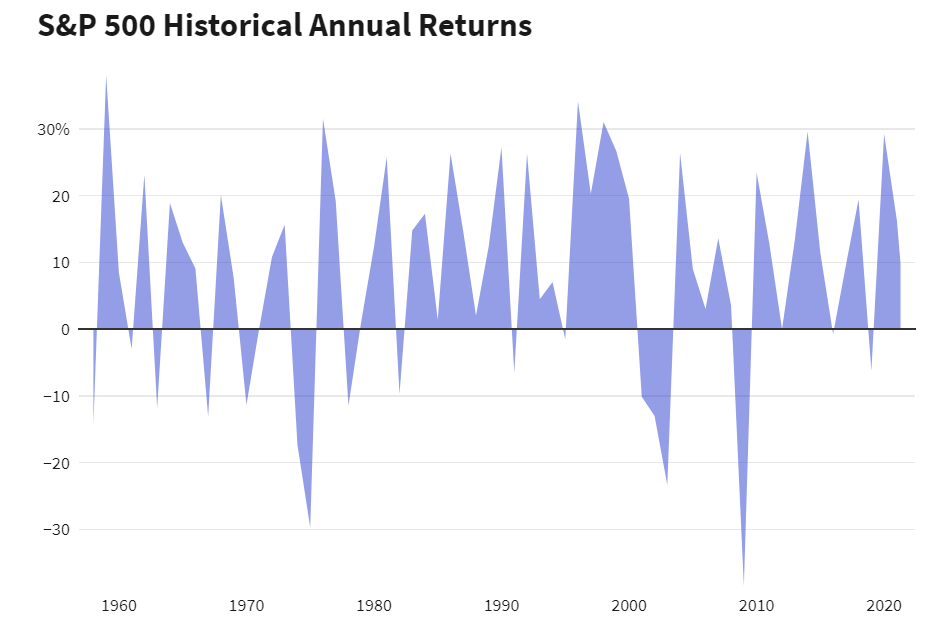

The average inflation-adjusted performance of the S&P 500 is about 7% per annum. That means we can assume an initial investment of $10,000 will practically double ($19,671) after 10 years in the market. However, as demonstrated below (Fig. 1), the S&P 500 suffers from high volatility, with some years experiencing drastic lows followed by sharp highs.

Fig.1. Source: Investopedia

Retirement investors often cannot afford to allocate all their capital to risky investments. Although index investing is a viable strategy for many, more risk-conscious investors should consider safer assets that experience less volatility year over year, such as:

- Government Bonds: 4.9% annual return

- 3-Month Treasury Bills: 4.23% average long-term return

- Real Estate: 8.6% annual return (i.e., residential/commercial portfolio)

- Fixed-Indexed Annuities: 3.27% annual return

- Physical Gold: 10.61% annual return

Don’t be suckered into an all-equities portfolio on account of their potential returns. Although they may look attractive at first glance, they carry significant volatility risks. Diversifying with blue-chip asset classes, such as those listed above, can help you manage risk while concurrently generating a handsome return.

4. Sign-up for Employer 401(k) Match

One of the fundamental rules of investing is that, if available to you, you should maximize your employer’s 401(k) match. While it’s becoming increasingly rare for employers to match their employees’ 401(k) contributions, many companies offer matching up to 50 cents on the dollar up to 6% of their pre-tax salary.

Unfortunately, only 56% of U.S. companies offer a 401(k) program. Of those that do, the median match is a mere 3% of one’s income. Still, employees should always reap the full benefit of this program. After all, it’s as much a part of your salary as your paycheck—not capitalizing on it would be leaving money on the table.

5. Set An Appropriate Time Horizon

Your investment style should match your time horizon, or the period of time you expect to hold the investment until the money is needed back. For some, they might need their money to vest for 10 years until they need the funds to provide a down payment on a house. Others might need their investments to grow for 30 years until they retire.

The longer one’s time horizon, the more risk one can afford to have in their portfolio. Those with long horizons (e.g., >10 years) might want to opt for riskier assets such as equities and cryptocurrencies. Those who need their money back in fewer than 10 years may want to opt for safer assets such as bonds, Treasury bills, and precious metals as part of a capital preservation strategy.

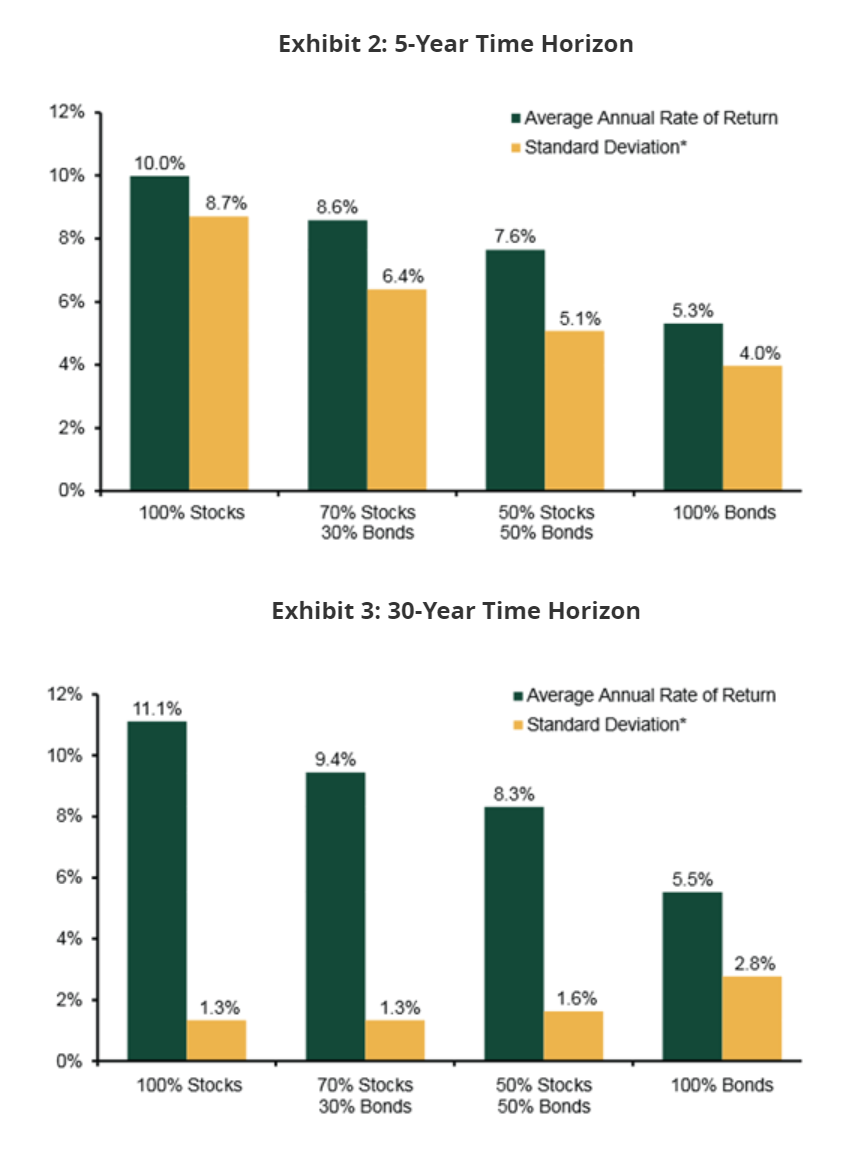

The chart below (Fig. 2) does a good job of demonstrating the importance of investing in less-risky assets if you have a short time horizon. However, investors need not limit themselves to stocks and bonds alone—indeed, there are a variety of potentially lucrative alternative asset types that also manage risk.

Fig. 2. Source: Fisher Investments

For a closer look at how your retirement portfolio might look depending on your time horizon, check out this handy guide to retirement investing strategies based on your age. It’s an “Investing in Stocks for Dummies” crash course with loads of useful, practical advice for investors of all stripes.

6. Avoid Predicting the Markets

A “set it and forget it” style of passive investing is, more often than not, more successful than actively managed portfolios. Predicting the highs and the lows of the market is a difficult task, and often multibillion-dollar hedge funds fail to do so successfully. It takes a certain degree of hubris to assume an amateur investor would do a better job.

Instead of timing the market, concentrate on building time in the market. The longer your investments sit, the more likely you are to build wealth—regardless of whether those investments were originally made during an upswing or down period in the market.

Taking positions in the market at regular intervals, in small installments, is referred to as dollar-cost averaging (DCA). According to the Charles Schwab Center for Financial Research, on average, those who attempt to time the market end up with significantly fewer gains than those who practice DCA.

In sum, diversifying your entry points in the market is important. This way, you can avoid the pitfalls of investing at inopportune times via poor market forecasting.

The Torino University DCA Study

A 2015 research paper by behavioral economists at the University of Torino ran real data simulations to test whether DCA is always optimal. Although they found that DCA didn’t always result in profit maximization, they remark that the practice does help “avoid common investment mistakes.”

Nonetheless, they maintain that “asset allocation diversification seems to be a less controversial suggestion than temporal diversification.” This conclusion broadly reaffirms the importance of diversifying across a variety of asset types (e.g., stocks, commodities, bonds) while focusing less on timing the market.

7. The Earlier, the Better

Although it’s an old cliche, when it comes to financial investing, the best time to start investing was yesterday. The second best time is now.

The graph below (Fig. 3) beautifully illustrates the importance of getting your money in the market early and making routine contributions. The difference between starting at the ages of 25 and 35 is massive, with the former resulting in nearly double the savings that someone would earn if they had started only 10 years later.

Fig. 3. Source: Lifehack

One of the cardinal rules of investments for dummies is that it pays to invest as early as possible, even if that means making small initial contributions. Don’t be discouraged if you’re over the age of 35 and haven’t started, or if you don’t have enough disposable income to contribute $5,000 annually.

Start today, regardless of your age, and contribute whatever you can reliably afford, even if that’s no more than $50 or $100 per month. There’s no age limit or contribution minimums to investing—so there’s truly no excuse to not get started right away.

Ready to Get Started?

Now that you know the basic ground rules of investing for dummies, consider supplementing your knowledge with more advanced learning material. A great place to start is with our free guide to creating an investment diversification strategy. Or, if you’d rather learn by experience, feel free to open an investment account and start building wealth today.

Remember, asset classes perform differently. Don’t lose out on potential gains, or expose your portfolio to unnecessary risk, by overconcentrating in one asset type. Your first step is to open a self-directed IRA, and get started investing in a wide array of investment options. Check out our list of the top self-directed IRA companies today to sign up for an account and jumpstart your limitless investing journey.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.