Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Higher interest rates can have an adverse effect on certain assets especially Bonds and Stocks. So too will other Alternative assets be effected, at least initially during the transition to higher rates. Gold and other precious metals will probably continue to head south as investors will find coupon paying securities more attractive. Private Equity funds may suffer due to the high levels of leverage used. To implement Buyout strategies some funds borrow up to 9 times the amount of equity to finance their strategy. Higher interest rates therefore may diminish their overall performance. Hedging a portfolio against higher interest rates may have a positive effect on overall return.

Interest rate outlook

As we move into 2016 it is looking more and more likely we will see a higher interest rate regime. The December Federal Reserve meeting will most likely bring the first hike of ¼% and the following press conference should give clues about the pace of further hikes. Considering you have a set of well diversified assets and that the outlook for your holdings remains stable in view of a positive forecast for the portfolio as whole. In this case you may not want to exit any of your current investments. But it may be helpful to protect performance by putting on some protective positions against higher interest rates.

Hedging strategies

One of the easiest ways to protect against higher interest rates is to gain direct short exposure to government bond & treasury futures and long positions in Put options or by short selling bonds & treasury notes. The CME exchange has futures contracts for US treasury notes for maturities of 2 years, 5 years 7 years and 10 years, as well as for Bonds which have a 30 year maturity.

These futures and option markets are extremely liquid and offer high price transparency. The various contracts for bonds and notes of different maturity help you off-set the risk on your notes and bonds holdings within your portfolio in an effective way. They are a derivative of the bonds and notes in your portfolio and have enough maturities to be able to match your portfolio duration.

What futures contracts are available?

Treasury notes and bonds are often used in hedging interest rate risk as Stocks and Gold for example will react negatively to an increase in interest rates. But bonds also carry credit risk. The US government is considered often as risk free, so using treasury or bond futures to hedge interest rate risk is often considered as appropriate. There are however other products that give you exposure to interest rates only, such as Interest Rate Swap futures. For example the CME 5 year Swap note or the ICE 10 year Swap future, or Libor Futures.

These products give you exposure to interest rates only, without the possible credit exposure you would access when you trade a treasury security. The price of these futures are quoted in the same way as a bond. They quote how many dollars it would cost you to buy or sell $100 of the interest rate swap note.

Apart from Libor futures Liquidity is a lot lower for these swap futures contracts compared to the bond and treasury note futures. But they may be more appealing if you just want interest rate risk exposure.

High correlation of rates to other assets

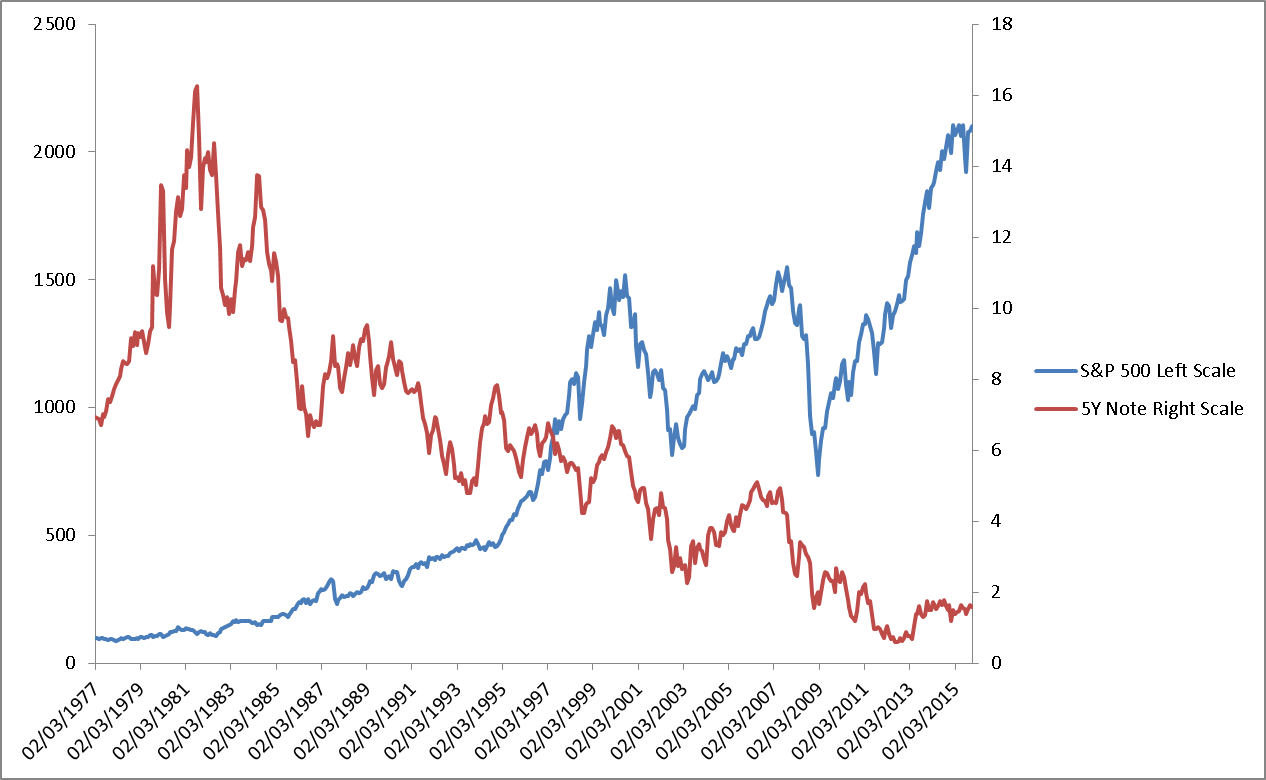

The correlation between the assets in your portfolio and interest rates is not so straight forward. Correlations across assets may also break down and change drastically over short periods which may last weeks or months. The correlation between Stocks and Rates may not have always been stable through time, but from my calculations the 5 years treasury note and the S&P 500 index have a correlation of -0.817. The calculation was made for the whole period since March 1977.

Correlation is measured as a number between +1 and -1, where +1 is maximum positive correlation and -1 is maximum negative correlation This number shows that when stocks go up the yield in 5 year notes goes down on a considerably reliable basis. This number also indicates that selling treasury note futures would be a pretty good hedge against rising rates for a large cap stock portfolio.

The correlation was calculated using monthly returns for the 5yr treasury note ^FVX and the S&P 500 index ^GSPC. The graph below shows how the two securities performed from March 1977. We can see that as the yield on the 5 year note increased the stock market had a subdued performance, once the yield started to drop so too did the Stock index begin to increase.

How many Notes do I sell?

This is the trickiest question when it comes to hedging a portfolio. With a broad portfolio of large cap stocks it is pretty easy to hedge total exposure. If you have $500,000 in your portfolio of stocks then you would need to sell 2 S&P 500 futures contracts.

5 year Treasury Notes futures are for a notional value of $100,000 but that doesn’t mean you have to sell the same amount of notional futures for the amount you hold in stocks. When gauging how many futures contracts you need to sell you have to consider convexity. That is you need to consider what a 1% change in price for your hedge would produce as a change in US dollar value, then compare it to the change in the Asset you are hedging. In the case of stocks every 1% change in stock price will change the US dollar value of your portfolio by 1%. However the 5yr treasury note futures on the NYSE are quoted at 167.93 for a notional value of $100,000. This means a 1% change in the price of this futures contract will actually see your position change by $1670 and not by $1000. You therefore need to divide the value of your portfolio by 167,930 to determine a more proportionate number of futures contracts rather than dividing simply by 100,000.

It also depends on your appetite for risk during the transition to higher interest rates. Selling more treasury futures contracts may even allow you to gain a higher return than that lost by other assets in your portfolio.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst