Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Annuities can be a viable option for steady retirement income, but there are risks involved in annuities that need considering. Most conceivable risks associated with annuities is something that can be mitigated by the customizable nature of the annuities themselves, assuming you’re willing to pay a price for it.

Annuity riders are provisions that you pay for annuities which lower the percentage of your annual annuity payout. For example, if your annual payout is 7% and a rider costs 0.50%, then your adjusted annual payout will be 6.50%. Therefore, it’s important to weigh their costs against their benefits.

Although we’ve already established that annuities, in many cases, are good retirement investments, the following are some intrinsic risks associated with annuities and the riders available for them.

Liquidity Risks

Standard Annuities tie up your money for a period of time. This inability to access your money quickly without reducing the value of your investment is liquidity risk. Withdrawals from annuities often lead to surrender charges that are levied on its contract. This surrender charge decreases with each passing year until rendered at zero percent, thereby allowing you to withdraw without penalty.

Guaranteed Lifetime Withdrawal Benefits (GLWB) Riders

A GLWB rider forgoes the surrender period and allows withdrawals without penalty. This establishes some level of protection from annuities risk of liquidity.

However, liquidity risk is not entirely resolved with a GLWB. If you’re not paying a price for early withdrawal then you will anyways pay a price for the provision that makes that early withdrawal possible, and this reduces your annuities value.

The Risk of Inflation

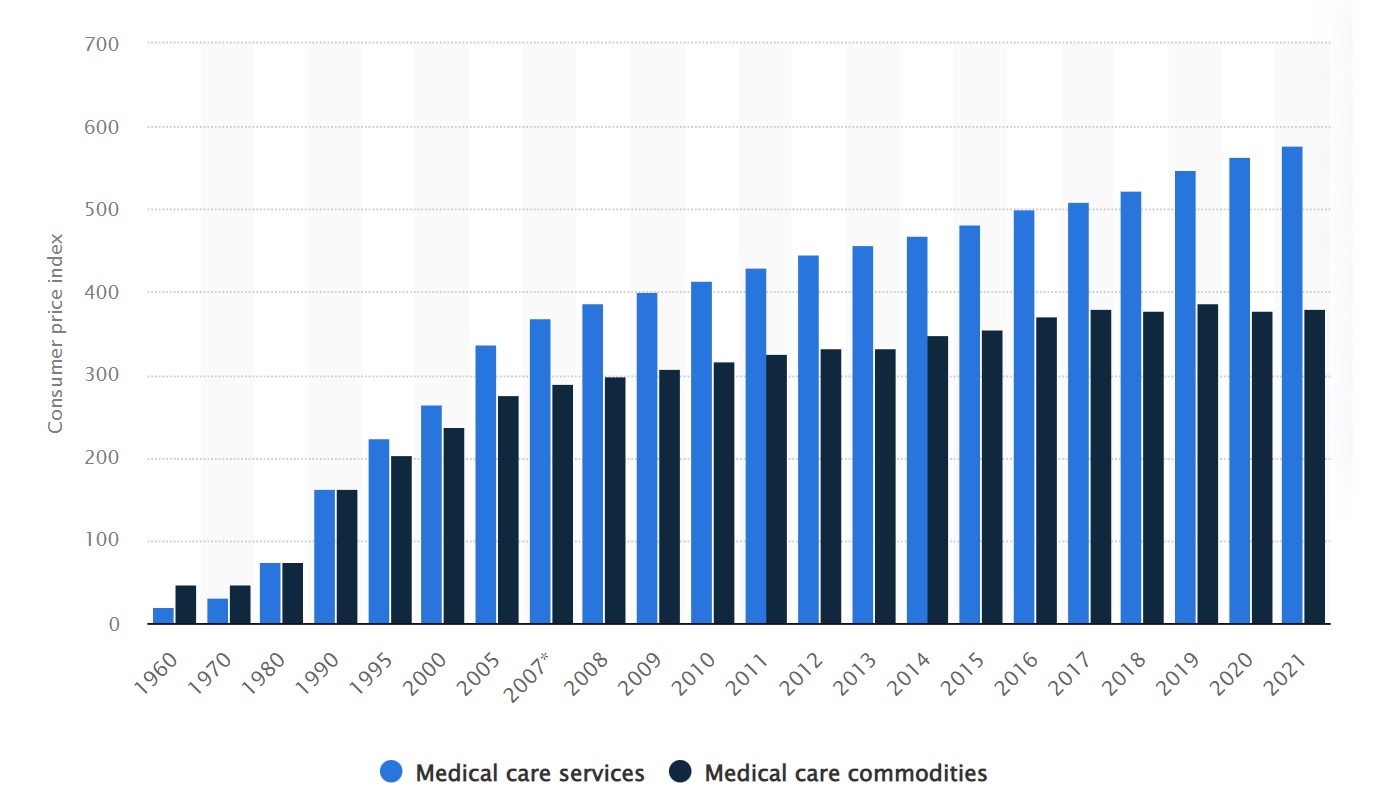

According to American Advisors Group (AAG), the nation’s lead in home equity solution, 66% of retirees aged 60-75 are worried that inflation will impact their retirement in a modern retirement survey recently conducted, and this worry is not unfounded.

The following is a graph published by the U.S. Department of Labor that shows the rise in prices of medical care commodities and services.

Source: U.S. consumer price index: medical care and commodities 2021

Consider that Spending on healthcare tends to increase with age, and if your annuity plays a role in budgeting during your retirement then a change in the purchasing power from the money you receive can be a blow to your financial security. Thankfully, there are riders that seek to establish some safety from rising prices.

Cost of Living Adjustment (COLA) Riders

These riders adjust the income received from your annuity for inflation. They apply either a fixed percentage rate each year regardless of the direction inflation takes, or a rate based on the increase in the consumer price index (CPI).

If however inflation has risen above the fixed rate in your COLA rider, then it will not account for the rise in price beyond that fixed percentage, so a CPI linked COLA may be better in this case. Conversely, if inflation hasn’t risen and you have a CPI linked COLA, then your annuity payments will not rise at all.

Determining which is better for you relies on your prerogative to weigh their benefits against the cost they incur, so reviewing your annuity contract is very important.

The Risk of Early Death

Essentially, you are purchasing an annuity in the hopes that you will live out the contract’s duration, but this is an uncertainty, and it establishes yet another annuities risk: the risk of early death. If an annuitant dies before the duration, then there is the possibility that the insurance company will keep the premiums.

While the money has to go somewhere, it will probably be a peace of mind for you to know that this money will go on to benefit your family and not the insurance company that essentially bet against your hopeful position. This is where a death benefit rider comes into play.

Death Benefit Rider

Death benefit riders pass over your annuity to a beneficiary. There are primarily two types of death benefit riders: a basic, and an enhanced one. The basic passes over the annuity in the amount it was paid for, and the enhanced passes it down in the amount of the highest recorded value by periodically locking in the gains from your annuity.

For example, if you were to purchase an annuity contract for $100,000, your beneficiary will receive that amount in a basic death benefit. However, with an enhanced death benefit, if you purchased a $100,000 variable annuity contract that increased to a record high of $150,000, then your beneficiary will receive that $150,000 even if the annuity is worth less then $150,000 at the time it’s passed over.

Other Annuity Riders

By understanding annuity riders you can invariably come to understand the risks that give them relevance. Some other annuity riders include:

- Guaranteed Minimum Accumulation Benefits (GMAB). GMAB riders alleviate market risks by guaranteeing a minimum value that is applied if the annuities market value falls below that minimum in a variable annuity

- Guaranteed Minimum Income Benefits (GMIB). These provide a minimum benefit for variable annuities regardless of market conditions. They don’t necessarily operate as a prophylactic measure, but rather as a possibility for the minimum to outperform the market value of the annuity when markets underperform.

- Lifetime Income Benefits Riders (LIBR). LIBR’s curtail the risk of outliving your money by providing income for the duration of your life.

- Impaired Risk Rider. These riders accelerate income payments by increasing payouts under the risk that an annuitant lifespan will shorten due to a health condition

Are Annuities Right for You?

Mitigating an annuities risk doesn’t obscure the fact that different investments offer different returns, so the question remains: will annuities give you the best returns for your retirement? The answer is a matter of understanding the implications of your annuities contract.

Coming to regret an annuity will likely be because you did not fully understand it in the first place. Insurance agents are not in the business of finding the best investment option for you, and they love to sell annuities because they get a commission for as long as you hold the annuity.

At this point, you may be wondering “Should I invest in an annuity through my IRA?” For those who want to invest in an annuity in a tax-advantaged environment, there are possibilities for doing so if the IRA is self-directed (e.g., not provided through a major brokerage like Fidelity or Vanguard). You can learn more about these flexible self-directed IRA plans here.

A thorough plan for your retirement should be met with both an understanding of your investment decisions, and the ability to facilitate such investments. Insurance companies provide you with the latter, but the former should be taken up by you as part of your due diligence. For this reason, I recommend you read up on our “annuities for dummies” guide to establish a more thorough understanding of annuities.

Adam Hamadiya is a financial writer who comes from a family of entrepreneurs. Witnessing success off the beaten path has made him particularly interested in behavioral and personal finance, subjects that he writes about widely in online publications.