Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Especially among retirement investors, “annuities” have become a hot but not always a well-understood topic. Some of us may have learned about it back in high school. But let’s do a quick revision, so you can make an informed decision about whether you want to diversify with this investment product that’s sometimes even considered an “insurance product” due to its low-risk, fixed-income structure.

Simply put, an annuity is a series of payments made over a typically long period of time in exchange for a lump-sum payment upfront.

The deduction you see each month from your salary towards the pension plan is an example of an annuity. Your monthly salary hits your account even after retirement (in the form of post-retirement benefits). The amount of benefit might not equate to your pre-retirement salary, but you get it without doing any work.

Previously, pension benefits were the easiest and simplest ways to describe annuities. But it has now taken the form of an established cottage industry, evolving from simple to more technical features, terms, and products.

Sometimes annuities can be so technical that you’d rather look for an alternative, easy-to-understand investment option. But not anymore, since we’re going to keep it simple and explain what annuities are in accessible terms.

Key Terms at a Glance

Let’s go through the most commonly used terms:

- Annuitant: the person subject to an annuity, same as the annuity contract owner

- Annuity Due: an annuity in which you receive payment, at the start of each period, as per the annuity contract

- Annuity Issuer: person(s) selling annuity product, usually insurance companies

- Annuity Rate: the growth rate embedded in an annuity

- Beneficiary: person(s) receiving benefits after “Annuitant” demise

- Ordinary Annuity: an annuity in which you receive payment, at the end of each period, as per the annuity contract

What’s the Difference?

Besides the point in time when a payment is made (i.e., at the end or start of a period), an ordinary annuity is a better option when you expect interest rates to drop.

Interest rates (annuity rates) are the cornerstone for annuity calculation. They are used to discount future payments to today’s value (irrespective of ordinary annuity or annuity due). Money loses value over a period of time. Therefore, paying $100 after five years is a better option than paying $100 today.

Choosing an ordinary annuity insurance plan with fixed payments means lower payment amounts later.

Which Option is Good for Me?

So here are the rules of thumb when you are juggling options:

- Whether you get an ordinary annuity or annuity due, the bottom line is you get a guaranteed regular income.

- An annuity with a longer tenure yields higher total returns than a comparable shorter one.

- An annuity with a longer tenure yields lower regular individual payments than a comparable shorter tenure.

- An annuity with a lower payment frequency yields higher returns than that with a higher frequency. You will earn relatively more with semi-annual payments versus monthly payments over a long period.

- An annuity contract with an insurance company with a higher credit rating will yield a slightly lesser return than a company with a lower credit rating. (Warning: you trade-off investment stability against short-term higher returns, so avoid it!)

Are Annuities a Good Investment?

In short, yes. With the influx of new alternative investment options, the importance of annuities has not seen a drop in the eyes of risk-conscious investors.

Guaranteed income payments for as long as you live give you mental freedom. You do not outlive your benefits unless, well, you burn the dollar bills intentionally. A post-retirement employee gets nearly the same salary (in benefits) as before, without working.

You can choose from a variety of options to best match your needs. Make your loved ones joint survivors or a beneficiary to ensure uninterrupted benefits after your death. Upgrade or downgrade benefits after death, or share the benefits between beneficiary and estate.

Check in the option to receive guaranteed fixed income if it is the only income source you depend on. Be flexible to opt for variable income if the annuity is one of the multiple income sources. Variable income does not necessarily mean lower than a fixed amount, it can be higher. It all depends on the matrix to which it’s linked. (Tip: If you’re a newbie annuity investor, we recommend considering a fixed income option.)

What Does the Data Suggest?

If we see the investment options on the table today, chances are that you might prefer investments in high-valued bullish stocks, cryptocurrencies, or affordable bonds. While all these options are not discouraged, why not do now what you will likely inevitably do in the future?

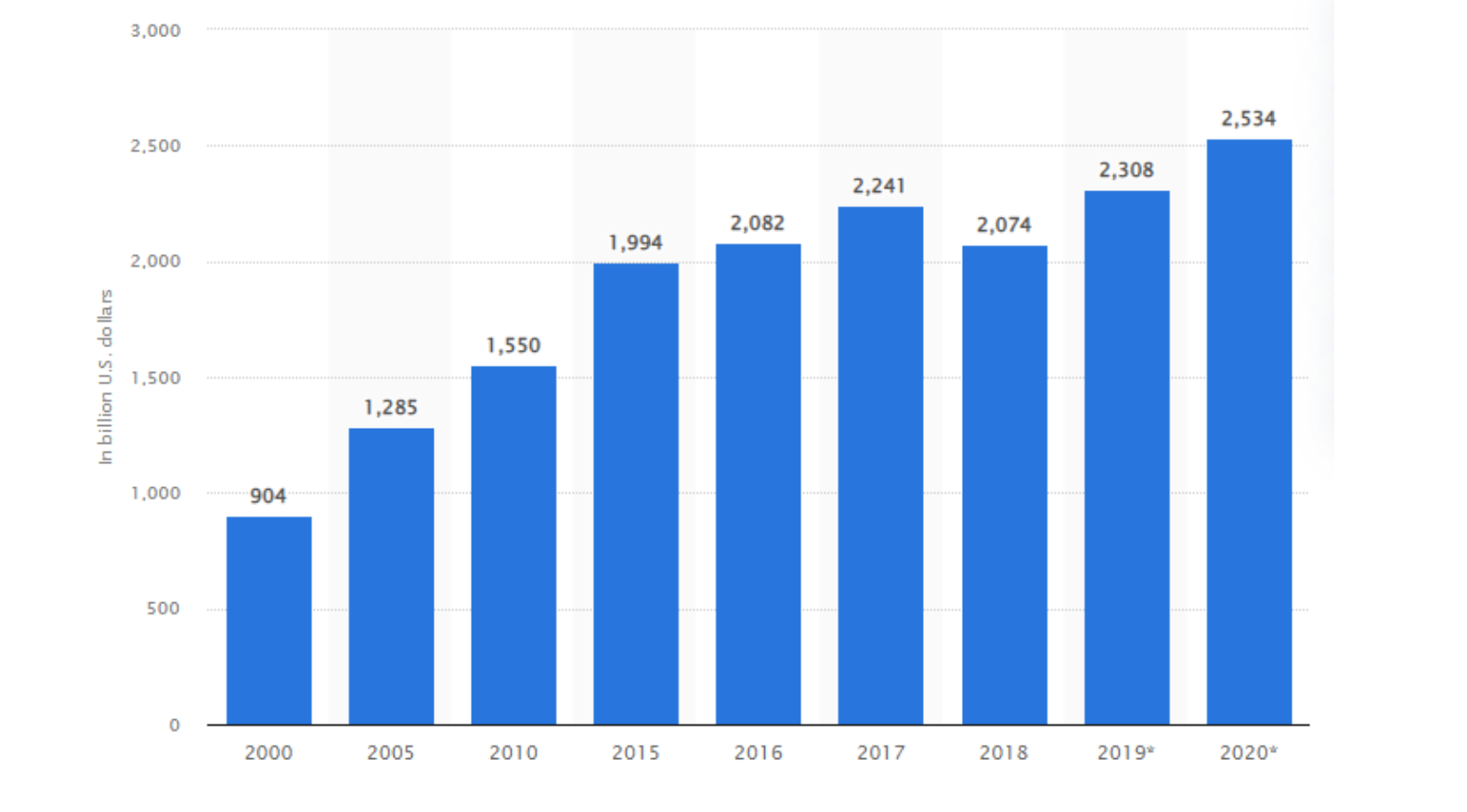

Data gives solid evidence that investments in US retirement annuities show a consistent surge. Take a look below:

Source: Statistica

You might notice a temporary decline in 2018. Being a prudent investor, you should evaluate it with other options like stocks and bonds over the same 20-year period. Investment in annuities will stand out. Give it a try!

I Am Retiring Soon, What Should I do?

If you feel that you still need more information, I recommend going through our comparison of annuities vs. other retirement accounts.

If you are already retired or are close to retirement without an annuity investment, don’t worry—you can still catch up.

A Trusted Annuity Investment will save you time sweating about the stability of your investment. Although you are going to get a modest yield, the chances of losing the principal amount are almost non-existent.

Mustafa K. (CA, CIA) is an accounting professional with over a decade of experience in financial audits, compliance, and advisory. Currently, Mustafa serves as a tax associate and finance writer.