Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

A variable annuity is a type of public annuity and investment vehicle whose value is tethered to the performance of an underlying investment portfolio. Investors close to retirement age often use variable annuities to ensure financial security and supplement their income after they stop working.

Public annuities are an important tool for retirement planning. However, they aren’t without their share of risks. In this article, I’ll explain what a variable annuity plan is, why they’re sought after by retirement investors, and will discuss the investment and tax risks associated with this type of public annuity.

What Is Variable Annuity?

Before defining variable annuities, let’s first unpack the concepts of public annuities and annuities in general. An annuity is a series of payments made at regular intervals over the lifetime of the plan holder (or the “annuitant”). The obligator is required to make payments to the annuitant per the terms of the annuity agreement.

A public annuity is a type of annuity sold by an insurance company or brokerage. As such, they often serve as an insurance product rather than an estate planning tool like a private annuity.

A variable annuity differs from a fixed annuity in that the former directs one’s annuity payments into an underlying investment vehicle such as a mutual fund. Consequently, one’s annuity payout varies depending on the rate of return of the underlying fund. By contrast, a fixed annuity is offered at a static, pre-determined interest rate that is often not adjusted for inflation.

The Risks of Variable Annuity Plans

There are risks inherent to annuities, and risks specific to the subaccounts to which the performance of a variable annuity is tied. Below are some of the main pitfalls of purchasing a variable annuity plan that you should be aware of.

Early Death

It’s not something that we like to think about, but the possibility of premature death can lead to a massive loss of value for an annuitant. An annuity contract is an agreement in which the obligator agrees to make payments for the rest of the annuitant’s life.

In most cases, the annuitant expects to receive several years’ worth of payments to realize the value of the agreement.

An early death can spoil the value of an annuity. Consider looking into variable annuity plans that pay a surviving spouse or next-of-kin for a predetermined period in the event of the annuitant’s death.

Market Risk

Variable annuity payments are determined by the performance of a subaccount, which is often a mutual fund or basket of index funds. Prolonged recessions or down markets, therefore, can reduce one’s annuity payments.

Taxes and Penalties

Annuity payments from variable annuities are taxed as ordinary income and not capital gains when they are withdrawn. Plus, annuitants cannot withdraw from a tax-deferred annuity before the age of 59 ½ without incurring a 10% early-withdrawal penalty.

Hidden Fees

With the exception of single premium immediate annuities, hidden fees are often baked into variable public annuities. Don’t be surprised to see fees such as surrender charges and asset-based fees on a variable annuity plan. After all, insurance companies have to make a profit on the sale of the annuity.

The Benefits of a Variable Annuity Plan

Although variable annuities are not without their risks, they offer several benefits for retirement-aged individuals.

- Flexibility and Personalization: Variable annuity plans offer diversification by purchasing subaccounts invested in a variety of asset classes, including equities, government bonds, corporate bonds, and precious metals. Investing across many asset classes minimizes market risk and allows plan holders to personalize their annuity to their risk tolerance.

- Tax Benefits: When held within a tax-deferred retirement savings account, such as a 401(k) or Roth IRA, the value of the annuity remains untaxed until it is withdrawn.

- Annuitization Income Guarantee: Variable annuities offer guaranteed income over the duration of one’s lifetime. After the account has been annuitized and turned over to the insurance company, the annuitant receives a regular income in the form of annuity payments until their death.

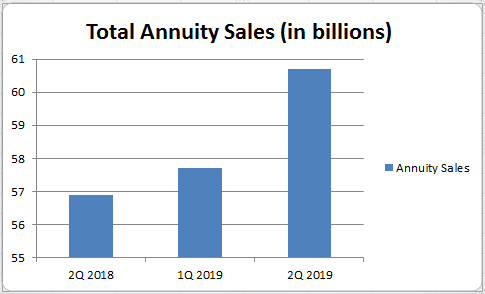

- Peace of Mind: The financial security and peace of mind that annuities offer are behind the growth in annuity sales seen as of late. As markets have destabilized and systemic risk became more present in the financial system between Q2 2018 and 2Q 2019, total annuity sales rose sharply.

Source: InsuranceNewsNet

Is Annuity Income Taxable?

We’re often asked, “Is annuity income taxable?” Although the tax implications of a variable annuity are complex, the short answer is simple. Yes, variable annuity income is taxable as regular income at the time of withdrawal. However, a variable annuity held in a tax-advantaged savings account can shelter your investment from capital gains taxes.

The Bottom Line

Variable annuities are both an investment vehicle and insurance product for retirees looking to mitigate market risk and minimize the risk of outliving their retirement savings. However, in the event of early death, the insurance company pockets the remaining value of the annuity and none is leftover for their next-of-kin as an inheritance. Generally, annuities are designed to be more beneficial the later in life one purchases it.

Annuities are one of the many tools at your disposal for diversifying your portfolio during your retirement. Variable annuities might be a worthwhile investment if one lacks confidence in the Social Security system or is not set to receive a sizable pension during retirement. However, the decision to purchase an annuity should be made in consultation with a licensed financial advisor who understands your unique financial circumstance.

Of course, variable annuities are but one of several investment vehicles that can stabilize your financial future. Opening a self-directed precious metals IRA can hedge your portfolio against systemic risk in the financial system and allow you to hang onto more of your wealth during times of economic downturn. For more retirement investing insights, consider subscribing to some of the top financial newsletters today.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.