Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Private annuities are valuable tools for estate planning. In essence, a private annuity is an agreement between an individual (the “annuitant”) and the obligator to whom property is being transferred. As such, private annuities are one of the most important tools for strategic wealth preservation.

Because annuities are integral to the process of estate planning, they also impact your retirement goals. To better prepare yourself for retirement, take a moment to familiarize yourself with private annuities, and learn more about why they’re an essential component of estate planning.

Annuities 101

Private annuities are often used by affluent families who want to pass their estate on to their children or grandchildren while minimizing their exposure to gift and estate taxes. When used properly, private annuities benefit the annuitant in the form of tax savings.

The advantage of a private annuity is that the annuitant transfers property—which can take the form of real estate, securities, precious metals, or other assets—to the obligator in exchange for regular payments that usually recur periodically until the end of the annuitant’s life.

Benefits of a Private Annuity

The main benefit of a private annuity is that it offers a fixed source of income over the course of the annuitant’s life. Furthermore, the income provided by a private annuity is mostly taxable at capital gains rates, which is generally preferable to regular income tax rates.

Another primary benefit of an annuity is that, once the transfer is completed, the property value and all future appreciation is removed from the annuitant’s taxable estate. In other words, the annuity reduces the overall tax burden owed by the annuitant.

Following a slate of regulatory changes introduced in October 2006, there are no gift taxes levied on private annuity transactions if the present value of the annuity is approximately equal to the property’s calculated fair market value (FMV).

In the event of the annuitant’s death, the beneficiaries of the annuity receive a financial windfall and are no longer required to make annuity payments. Therefore, an early death would result in the inheritance of the property at a financial discount for the beneficiary.

The Risks and Disadvantages of a Private Annuity

One disadvantage of private annuities is that they present an investment risk for both parties. On the one hand, the annuitant assumes risk because the estate could depreciate in value which would mean the size of the estate would be larger than if the transfer had not taken place.

On the other hand, the obligator assumes two primary forms of risk: investment risk and mortality risk. If the annuitant far exceeds their life expectancy, the obligator remains on the hook to make payments. Therefore, the transferee party may be obligated to make decades’ worth of payments after they expected to stop. Second, there is investment risk involved because the obligator may not always have cash on hand to make annuity payments.

The annuitant assumes the risk that the obligator may predecease them. To minimize the risk of default, the annuitant can purchase insurance on the obligator or make the annuity with a trust so that the beneficiaries guarantee annuity payments.

Difference Between Private and Public Annuities

An annuity is considered private when it is made by an individual rather than a commercial insurance firm. Therefore, a public annuity plan is any sold or facilitated by a brokerage or insurance company.

With a public annuity plan, an individual can “insure” their retirement by receiving periodic payments after they stop working. There are two types of public annuities:

- Fixed Annuity: The insurance company or brokerage offers a fixed interest rate and a fixed number of payments as regulated by state commissioners.

- Variable Annuity: The insurance company or brokerage offers the option of directing one’s annuity payments into mutual funds or other investment options. Therefore, one’s payout depends on the investment’s rate of return, the amount invested, and the associated fees.

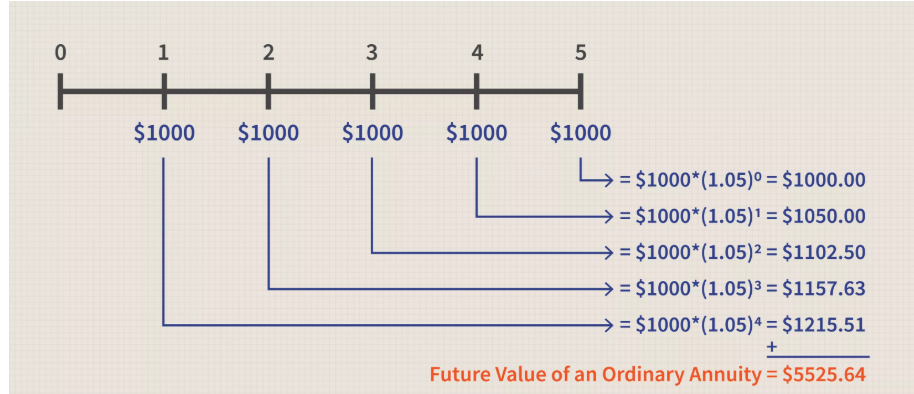

There are two phases to a public annuity: the accumulation phase and the payout phase. During the former, payments are made into a trust or an investment fund, depending on the type of public annuity chosen. During the latter phase, the annuitant receives their payments and any associated gains in periodic installments or in a lump-sum.

The chart below describes how the future value of a variable annuity can increase over time due to the compound effect of money.

Source: Investopedia

The 2006 Regulatory Changes

In 2006, the Internal Revenue Service (IRS) made sweeping changes to the laws that affect annuities. The release of Prop. Treasury Reg. §§ 1.72-6(e) and 1.1001-1(j) changed the regulatory environment governing the issuance of annuities.

The new rules require taxpayers to ascertain the FMV of the property traded for an annuity and for any losses or gains to be incurred immediately. Consequently, annuities are partially excluded from one’s income as a return on the annuitant’s investment and therefore taxed only partly as regular income.

In simpler terms, the IRS’s 2006 regulatory changes make it such that gains and losses are now acknowledged and recognized by the IRS and Treasury at the time of the property’s exchange. These rules make alternatives to annuities more competitive, such as installment notes or installment sales.

The Bottom Line

Private annuities are one of the fundamental pillars of wealth preservation and estate planning in one’s retirement. Although they present the opportunity to establish financial security after retirement, they also carry investment and mortality risk for both parties. For this reason, it’s best to speak to a licensed financial advisor about whether they’re right for your situation.

To better your financial situation ahead of retirement, consider opening a silver or gold IRA or subscribing to our top investment newsletters to stay abreast of the latest trends and developments in the world of retirement investing.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.