Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

In 2020, U.S. student loan debt eclipsed $1.56 trillion. The median debt burden for the graduating Class of 2019 is nearly $30,000, up over 2% from the year prior. It seems that every year, American students are becoming more indebted and less economically advantaged than the graduating class before them.

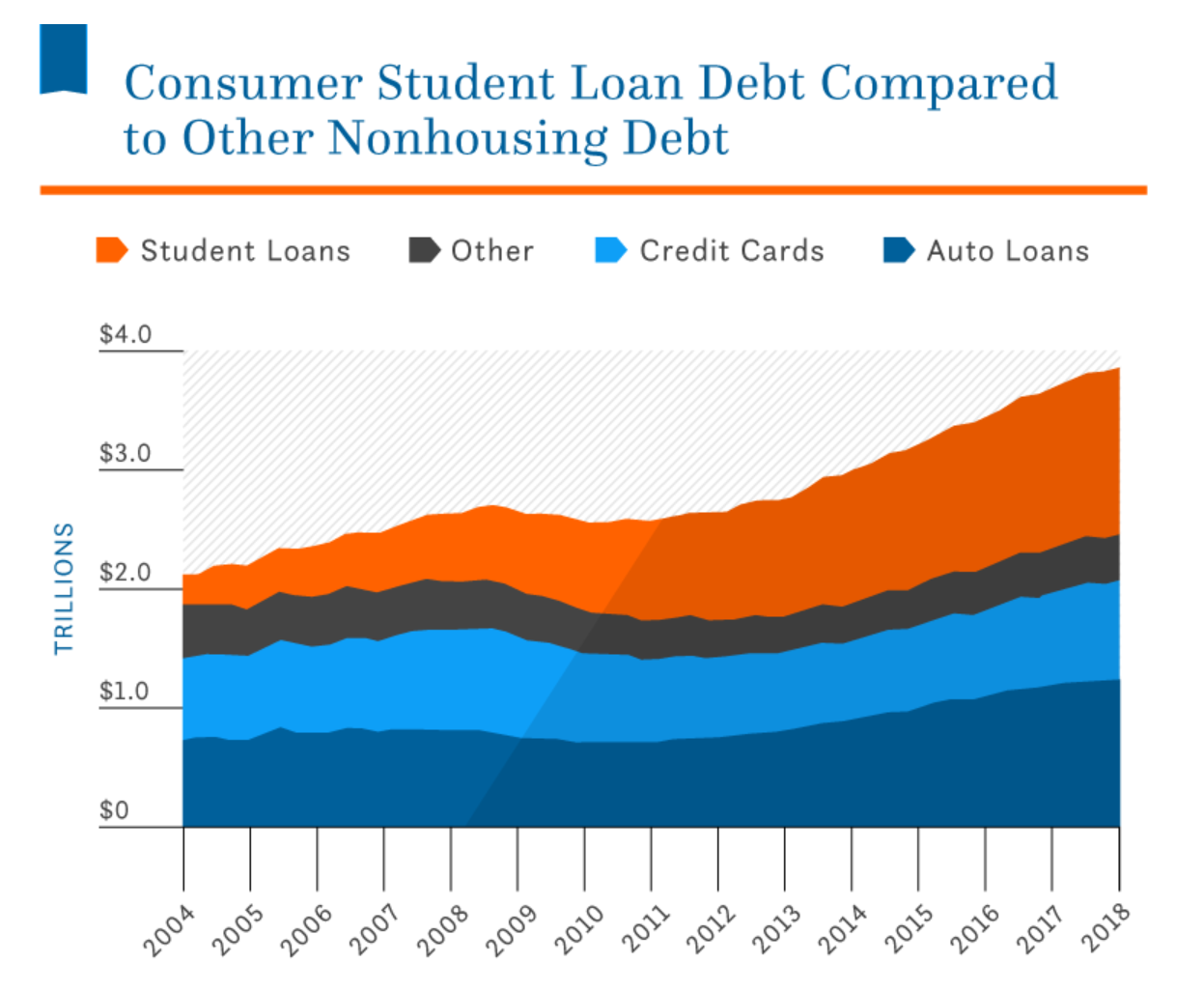

To the surprise of no one, a recent study by the U.S. Federal Reserve found that student loan debt is a major barrier to homeownership, a drag on Millennial retirement investing, and an impediment to the growth of the housing market. For every $1,000 that the median student debt burden lowers, homeownership rates increase by 1.5 percent among Millennial-aged college graduates. Plus, every year student loan debt takes on a greater share of the U.S. nonhousing debt load.

Source: Nitro College

The evidence casts little doubt on the matter—rising student debt is an increasingly significant societal burden. Fortunately, there are strategies that you can utilize to pay down your debt faster. Here are my top five rules for paying off student loans faster so you can get a headstart on the path to financial freedom.

Consider Loan Forgiveness Options

First, check to see whether you qualify for a student loan forgiveness pathway. In the U.S., there are two federal programs that allow for public student debt to be forgiven.

Public Service Loan Forgiveness

The U.S. federal government forgave nearly $72 million in student debt between January and September 2019 under the Public Service Loan Forgiveness (PSLF) program.

PSLF lets borrowers have the outstanding balance of their student loan account forgiven after having made 120 monthly payments while employed full-time by the government or a non-profit organization.

Teacher Loan Forgiveness

Teachers at low-income elementary or secondary schools who teach full-time for a minimum of five consecutive academic years are eligible for loan forgiveness of up to $17,500. Eligible borrowers may not apply for both the PSLF and the Teacher Loan Forgiveness program.

Split Your Payments in Two

Let’s say you’re currently paying $500 a month on student loan repayments. That amounts to 12 payments of $500 ($6,000 total) over the course of a year.

By merely dividing your payment amount in two ($250 each) and making each payment on the 1st and 15th of the month, you end up making 26 payments per year or the equivalent of 13 months. In other words, this simple trick lets you knock out an extra month’s payments every year and you’ll barely feel the effect on your bank account.

To make sure that you never miss a payment, make sure you sign up for auto-pay through your bank or student loan servicer. Even if you only occasionally miss a payment by only a few days, the accumulated interest can end up prolonging the life of the loan.

Consider Refinancing

If you’re employed and have a FICO score above 600, you should consider refinancing your student loans. Since you cannot refinance federal student loans, you have to take out a new loan and use the loaned amount to pay off your federal loan in full. Then, the new loan replaces your public student loan.

Refinancing a $30,000 student loan for an interest rate of 4 percent over 7 years instead of, say, 5% over 10 years, your monthly repayment amount becomes $425 instead of $336. However, you would have your loan repaid 3 years earlier and would only pay $5,766 in interest over the lifetime of the loan as opposed to $10,405 under the original financing terms.

Cut Costs and Budget Wisely

Aside from supplementing your income, cutting expenses and budgeting is the best strategy for finding more money at the end of the month to contribute to your loan repayments.

First, detail your spending habits and create a list of your recurring monthly expenses. If any are unnecessary or can be reduced, try to lower or eliminate the expense and use the saved money to top up your monthly repayment.

Merely cutting out expensive meals at restaurants, fancy coffees and lattes, and unnecessarily expensive car insurance or data plan phone bills can save you hundreds of dollars per month that can shave years off your student loan.

Get a “Student Loan” Side Job

Supplementing your income with a part-time side hustle on weeknights or weekends is often the most effective strategy for increasing one’s monthly repayments. The key is to hold yourself accountable for how you spend the income earned with your second job.

If you think of your side hustle as “extra income”, you’ll find that it will quickly deplete and you won’t have anything left to throw at your loan balance. That’s why it’s crucial that you only allow yourself to spend your side income on increasing your loan repayment amount.

Putting It All Together

There’s no better feeling for a college graduate than to make that final repayment on their student loan and watch as their balance hits zero. To fast-track your way to this major financial milestone you’re going to have to put in some hard work, make a few sacrifices, and be a bit of a savvy opportunist when it comes time to refinance your loan.

Paying off student loans fast isn’t easy, but it can be done. By following these rules above, you can set yourself on the path to financial freedom and eliminate your student debt for good. To accelerate your journey to financial independence, check out our investment newsletter reviews so you can stay ahead of market developments, and invest your money with confidence.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.