Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Two-thirds of Millennials have nothing saved for retirement. Can you blame them?

Millennials, born between 1981 and 1996, entered the job market amid one of the worst periods of wage stagnation and unemployment in recent history—not to mention an average student loan debt of $33,000 per graduate in Q2 2019. For many of us, immediate financial need simply trumps the higher-order desire to invest in our retirement.

Despite this, not all young people are doing away with retirement investing. Surprising as it may be, 16% of Millennials have $100,000 or more tucked away for retirement. There’s no reason to feel guilty if you’re not a part of this moneyed Millennial minority—there are actionable steps you can take to start investing young so that you too can retire early, wealthy, and financially free.

Max Out Your Employer-Sponsored 401(k) Plan (If You’re Eligible)

It’s a no-brainer that full-time employees with a 401(k) employer matching program should take full advantage of the privilege. In most cases, employer matching programs offer “100% of the first 6%” of the employee’s annual gross pay. Once an employer has matched up to the 6% threshold, the employer’s contributions stop until the following year.

Let’s take the example of an individual who earns the median individual income among Millennials: $47,034. If their employer offers matching of up to 100% on the first 6% gross income, then they should contribute no less than $2,822 per year to their 401(k) for as long as they remain at this income level. To do otherwise would leave free money on the table.

What About Part-Timers and Gig Workers?

Unlike the generations before them, a sizeable share of working Millennials do not qualify for an employer-sponsored 401(k) retirement savings plan.

Since only full-time employees are eligible for most employer contribution matching programs, part-time workers and gig economy workers are left to fend for themselves. Among Millennials, part-timers and gig workers make up at least 25% of the workforce.

Therefore, about a quarter of Millennials need to more aggressively contribute to their 401(k) plans or other tax-advantaged retirement savings accounts. To meet their retirement goals, Millennials who don’t qualify for employer matching programs should aim to double what their employer-matched counterparts contribute—roughly 12% of their gross pay, or $5,644 if they earn the median Millennial income.

What About Student Debt?

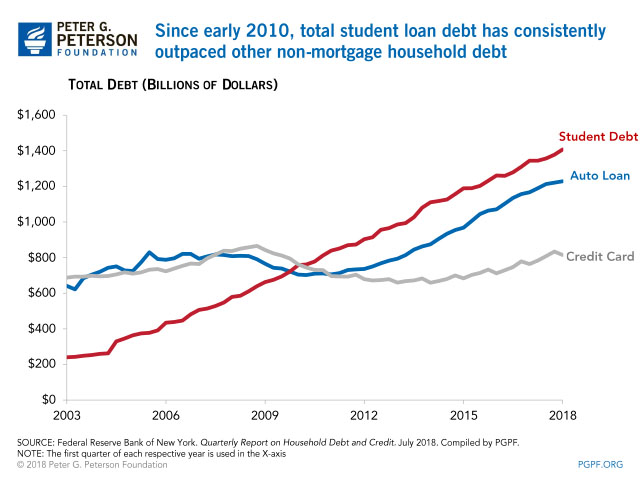

As of 2019, for U.S. borrowers aged 25 to 34 (a sizable share of the Millennial population), there was $497.6 billion in outstanding federal student debt spread across roughly 15 million individuals. This figure dwarfs the sum of all student debt owed by U.S. borrowers only 15 years earlier in 2004, which amounted to $345 billion.

Source: Peter G. Peterson Foundation

Student debt is a mounting problem for North American Millennials looking to get a start on their retirement savings and is a contributing factor to the longstanding decline in home ownership rates for 25 to 34 year olds. Although 38% of Millennials aged 25 to 34 currently own a home in the United States, this figure is down from 55% in 1980. A delay in home ownership will ultimately limit one’s capacity to build long-term wealth and a lack of home equity may contribute to retirement insecurity later in life.

Millennials, then, are confronted by a dual-pronged problem: the competing interests of saving for retirement and paying down one’s student debt. Where one decides to put their money should be made on a case-by-case basis in consultation with a financial advisor, but there are some general guidelines that can help you make a case-specific decision.

Not paying one’s debt beyond the minimum required payment makes sense only if you are near-certain that an alternative investment will provide a greater return than the cost of having the debt. In other words, if you’re charged 6.08% interest on your unsubsidized graduate student loan then you might be better off throwing additional discretionary income at your loan unless you’re confident you can net a >6% return on the investments made in your retirement savings fund. Generally speaking, however, it’s advised that student debt holders still make monthly contributions to a retirement savings fund regardless of their debts outstanding—even if their contribution is one percent or less of their gross income. As the principal is paid down, whatever freed-up income is left over should be put toward retirement investing.

Building an Emergency Fund

Before you sock money away for retirement, it’s a good idea to first set aside an emergency fund. Typically, emergency funds are meant to cover at least three months’ worth of living expenses in case you lose your job or have an unexpected expense arise. Your emergency fund’s raison d’etre is to prevent you from going back into debt.

Millennials often have fewer expenses than older folks, which means we can often get away with putting aside a smaller share of our income into an emergency fund. Single Millennials without dependents can sometimes make do with simply squirreling away 75-80% of two months’ expenses.

Having extra cushion in your savings account can carry the temptation to spend it. That’s why it helps to first define what a true emergency means given your particular financial circumstance. For example, transferring money out of your emergency fund to prevent your savings account from going into overdraft and incurring fees is a justifiable reason to make a withdrawal. Using your emergency fund to cover the repairs needed on your blown furnace? Also justifiable.

Splurging on a pallet of Fiji water for your hot tub? Not justifiable. Buying your fourth Apple Watch because you don’t feel like changing the band out? Power move, but also unjustifiable. Better to first define what constitutes an emergency before you build a fund dedicated to their response.

Assess Your Risk Tolerance

If you stayed awake through it, you might remember the terms “risk-loving” and “risk-averse” from Microeconomics 101. The gist, for our intents and purposes, is that younger investors are generally more accepting of risk than older ones nearer to retirement due to the longer time horizon of our investments. Longer time horizons are generally associated with lower volatility.

While Millennial retirement investing strategies often encourage a majority allocation of one’s portfolio in growth stocks, older investors (i.e., five to ten years from retirement) are better off safeguarding their wealth by reallocating a larger share of their holdings to precious metals or fixed-income securities that provide reliable interest income over a defined period of time. This way, periods of volatility won’t disrupt their short-term retirement goals.

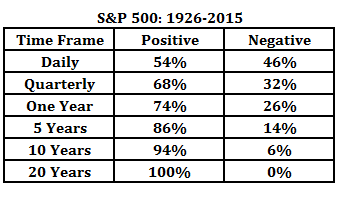

Source: A Wealth of Common Sense

The chart above perfectly demonstrates the advantage of a long time horizon. As a young investor, the chances of a negative return (i.e., losing money) by investing broadly across the U.S. stock market is 46% on any given day but recedes to 0% after 20 years.

For the more conservative Millennial retirement investor who wants steady, predictable growth, fixed-income securities are a better option over tech stocks or index funds. While stocks represent the “growth” portion of your portfolio, precious metals and fixed-income securities represent the “safety” component.

Some of the more popular fixed-income securities include:

- Bonds: A security issued by a national government with a promise to repay periodically at a given interest rate, backed by the full faith and credit of the issuing government. (Since U.S. interest rates fluctuate over time, these still carry interest rate risk for those who buy long-dated bonds that mature after 15, 20 or 30 years).

- Bond ETFs: Bond exchange-traded funds (ETFs) or mutual funds that invest in many government and corporate bonds help reduce one’s exposure to risk via diversification.

- Treasury bills (T-Bills): A short-term U.S. government debt obligation with a maturity of only one year or less and often sold in $1,000 denominations.

Make Your Portfolio Recession-Resistant

Before you fire up your Robinhood account and choose a preset portfolio based on your risk tolerance and time horizon, consider optimizing your portfolio to reduce your exposure to the business cycle. Recessions naturally come and go, and it’s important that you exercise basic precautions to shield your wealth from assets that could flounder in a down economy.

Many of the world’s most successful investors, such as Shark Tank’s Kevin O’Leary, dedicate between five and ten percent of their portfolio to precious metals. Adding gold or silver bullion to a self-directed traditional or Roth IRA (or RRSP/TFSA in Canada) can insulate the value of your portfolio from the natural cyclicality of the economy as well as broader risk in the financial system as a whole.

For centuries, precious metals have been used as a hedge against inflation, currency devaluation, and stock market decline. It’s no surprise, then, that the price of gold reached multi-year highs during the late-2000s global financial crisis and the 2020 stock market crash.

Those who invested in precious metals ahead of these crises fared significantly better in their wake than those who invested in the stock market alone. In fact, the S&P 500 index lost roughly 50% of its value during the bear market from 2007 to 2009, while gold bullion rose from $869 to $1,087 per ounce—a gain of over 25%.

If you’re considering getting started investing in precious metals, check out our gold IRA comparison chart. For a more in-depth look at retirement investing strategies, I strongly recommend subscribing to some of these Millennial investing and stock trading newsletters.

A Word on Stock Picking

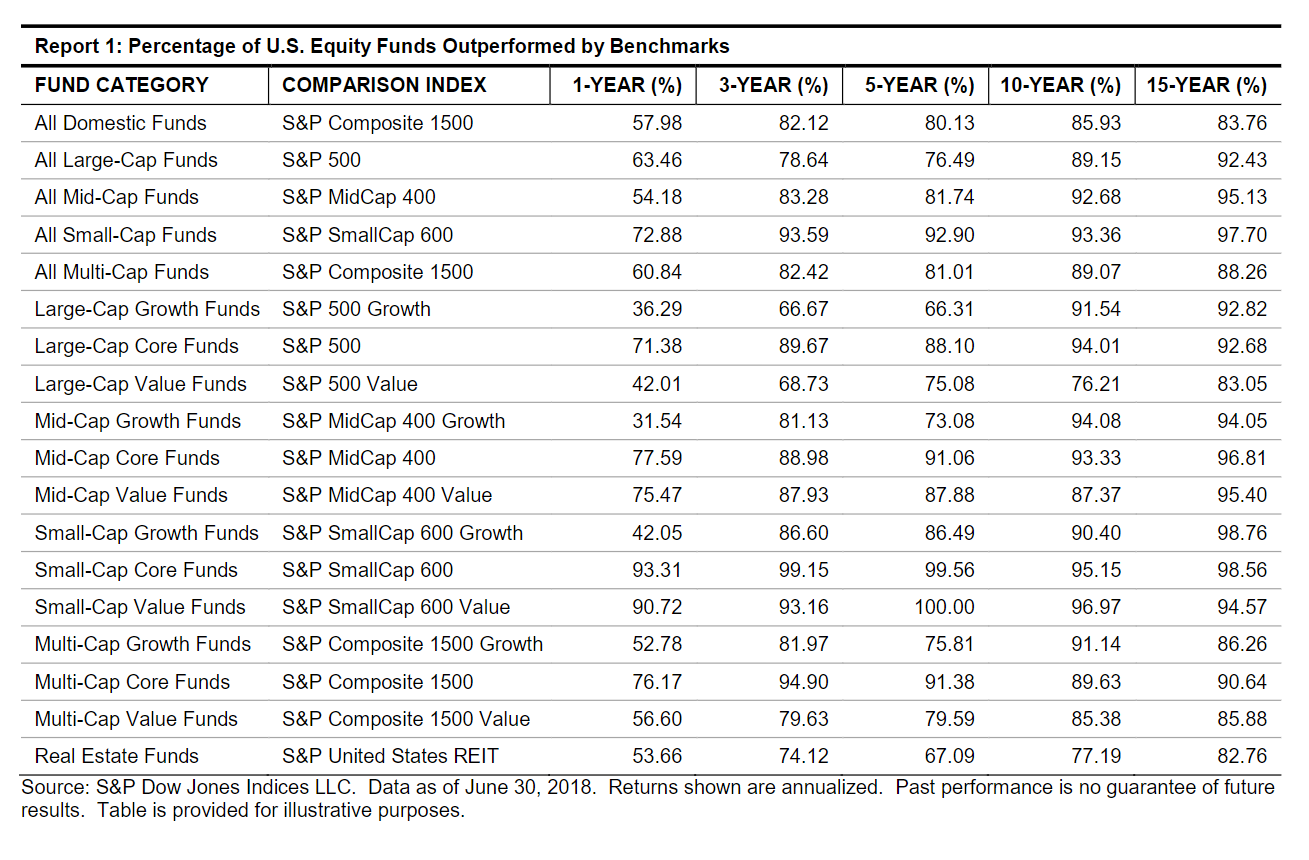

Nobody has a crystal ball to predict price movements on individual stocks. For this reason, most non-expert investors are better off dollar cost averaging across trusted index funds if they want exposure to the equities market. Although stock trading presents plenty of opportunities to turn a profit, statistics prove that you’re unlikely to beat the market (i.e., economy-wide benchmarks such as the S&P 500 or Dow Jones Industrial Average) over time.

For example, the 2018 SPIVA U.S. Scorecard found that 63.46% of large-cap and 72.88% of small-cap fund managers underperformed the S&P 500 in the prior year. Over a 15-year period, less than 17% of all domestic U.S. equity funds outperformed the S&P Composite 500.

However, for younger Millennial investors willing to accept more risk, there are a few key elements of a publicly-traded company’s fundamental value that can help guide you in the right direction regarding buying or selling stock:

- Price/Earnings Ratio (P/E Ratio): A method for valuing a company based on its current share price compared to its per-share earnings. To find a company’s P/E ratio, divide the current stock price by their earnings per share (EPS). A higher P/E indicates positive investor sentiment regarding expected future earnings growth compared to companies with lower P/E ratios. The P/E ratio also tells us what an investor is willing to pay per dollar of earnings (e.g., a P/E ratio of 10 indicates that investors are willing to spend $10 for every dollar of current earnings).

- Price-to-Book Ratio (P/B Ratio): A measure of the market’s valuation of a company relative to its book value (i.e., total assets minus intangible assets and liabilities). A company’s book value represents the total value of the assets the company’s shareholders would receive in the event of a liquidation. Companies with P/B ratios under one (1) are generally considered to be safe, growth-oriented investments.

- Debt-to-Equity Ratio (D/E Ratio): A company’s total liabilities divided by its shareholder equity, which are both found on a company’s financial statements. This metric determines the extent to which a company is leveraged. Companies with high D/E ratios generally present a higher risk to shareholders because it suggests that a company may not be able to cover their outstanding debts following a downturn.

- Free Cash Flow (FCF): The cash that a company has leftover after factoring in cash outflows required to maintain operations and capital assets. FCF is a measure of a company’s current profitability and represents cash available to pay interest or dividends to investors and repay creditors.

Ultimately, stock picking can feel a lot like playing the lottery. But at least when gambling you know the odds. The chart below depicts the one-year to 15-year percentage of professionally-managed funds that “beat the market” compared to benchmark indexes. If senior managers with decades of tenure at the world’s largest mutual funds cannot reliably pick winning stocks, why should you trust your own ability to do so?

Source: 2018 SPIVA U.S. Scorecard

Remember that you can always buy individual shares on top of index funds if you want to shuffle the weight of certain holdings in your portfolio. To match your desired risk profile, you can change your asset allocation (i.e., the percentage of wealth stored in index funds vs. individual stocks). The underlying logic is that it’s a safer bet to have positions in hundreds of companies at once as opposed to only a select few hand-picked stocks that can tank your portfolio in the event of a market downturn or technical correction.

Building Financial Habits: The ‘Long Game’ of Compound Earning

The upside of Millennial retirement investing is that your youth is your greatest asset. Even if you only start today, you can build a lot of wealth over a 30-year time horizon. It starts with ingraining financially responsible habits which, over time, accumulate to make a big impact.

The consequences of delaying your retirement savings are high. Assuming a seven percent annual return, you have to save double for every ten years you delay starting. Of course, the inverse is also true. With seven percent annual returns, a contribution of $25,000 at the age of 25 will amount to almost $375,000 by age 65 due purely to the compound value of money.

If you’re not a high-income earner, don’t feel as though you have to contribute any predetermined share of your net pay to your retirement savings. A sum as low as $25 or $30 per month is enough to realize the benefits of compound earnings and to grow a small nest egg. A monthly contribution in this range is a great place to start when you enter the job market, which can (and should) be scaled up as your income-to-expenses ratio rises.

Millennial investing doesn’t have to be complicated, but it should be responsible, prudent, and habit-forming. By regularly adding to your diversified portfolio—6% of gross pay for employer-matched 401(k) plan holders or 12% for non-matched investors—you can set yourself on course for early retirement and a more secure financial future.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.