Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

The Value of Alternatives

What is known now as the Endowment Model was introduced by David Swensen of Yale in the mid-1990s and consists principally of allocating a large part of a portfolio to non-traditional illiquid and risky assets. David Swensen has been at Yale since 1985 as the Chief Investment Officer, when the Endowment had a value of less than $1 billion. These illiquid and risky assets are the domain of Alternative Investments and mainly refer to Hedge Funds, Private Equity, Real Estate and Farmland and Timberland. The Yale endowment as of June 2014 stood at $23.9 billion, the endowment created a return of 20.2% for the fiscal year of 2014. This year’s returns are at 11.5%, bringing the size of the endowment to $25.6 billion. That seems an incredibly strong performance for any portfolio when compared to the general stock market or its closest peer Harvard. An ETF that tracks the broad market S&P 500, such as SPDR SPY, has a 1 year return of 5.20% and the broad stock market in 2014 had a return of 12.42% when considering the S&P 500 index.

Harvard hasn’t fared so well, with 2015 returns at a low 5.8% and the resignation of some of the investment staff at the endowment.

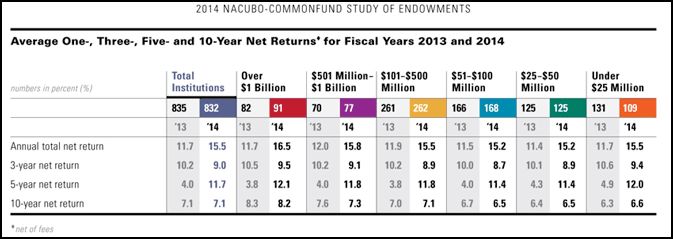

Looking at how it’s peers performed more generally may also shed more light as to how well this type of portfolio may perform. The NACUBO commonfund study of educational endowments for 2014 showed that the average return for 2014 of 832 endowments was 15.5%. More interestingly the top decile of returns was at 19.8% putting Yale with the very top performers.

How a typical Endowment portfolio is allocated

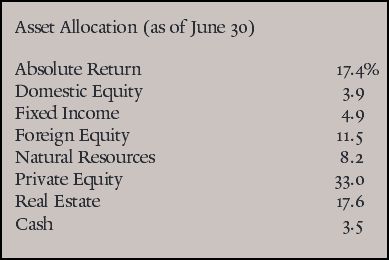

The Yale portfolio allocation model has been copied by many and allocates a large proportion of the portfolio to alternative assets. Asset allocations at the Yale Endowment as of June 30 had 76.2% of the portfolio invested in alternative assets.

The break down in the chart below shows the largest allocation was amongst alternatives which went to Private Equity, with 33% of the portfolio. The target allocations for 2016 change slightly with Private Equity and Real Estate being reduced somewhat to 30% and 13% respectively. While Hedge Funds have an increased target to 21.5%.

Source investmets.yale.edu

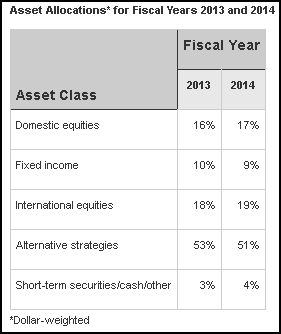

Comparing this allocation with the average allocation of assets from the NACUBO report, see chart below, we can see that the average allocation of endowments to alternative investments was 51% which is down from the 2013 allocation of 53%

The average endowment also allocated 17% to Domestic Equity and 19% to International Equity, Yale’s allocations for these two asset classes were 3.9% and 11.9% respectively.

Understanding return sources

As the average endowment had an annual return of 15.5% for 2014 with a lower allocation to alternative assets of 51% and a higher allocation to Equity than the Yale portfolio, it would seem that having a higher proportion of the portfolio in alternative investments and less in Equity has paid off handsomely. The market inefficiencies inherent to alternative assets allows for investors who have done their homework to take advantage and implement actively managed strategies. This may explain the continued generation of Alpha. In fact Yale has not only had out performing returns as of the past 2 years. The past 10 years the Yale endowment has had a net annual return of 11% out-performing its benchmark and other institutional fund indices. Allocating simply a larger proportion of a portfolio to alternative investments alone may not be sufficient in producing superior returns. There is a lot of work to be done in portfolio construction and investment selection should not be taken lightly. In the NACUBO report the endowments with the largest capital were also the ones that had the best performance in alternative assets such as Private Equity , where the largest endowments had returns of 32.4% for VC and 20.9% for LBOs and M&As compared to 13% and 2.1% for endowments with less than $25 million.

Larger funds allows for hiring more investment specialists and therefore having more resources. The report also finds that endowments with more than $1 billion had on average 9.3 Full Time Equivalent (FTE) employees while endowments with less than $500 million report less than 1 FTE employee, it is reasonable to think that most of these smaller endowments are making use of external investment professionals.

Why all the critique

The critique started after the onset of the financial crisis when assumptions that had previously held out well in portfolio management began to fall apart. Alternatives offer a return premium due to the illiquid nature of some of these investments due to the lumpiness and small private trading market as in the case of Real Estate or Private Equity. They are also known for low to negative correlations to traditional assets like Stocks and Bonds. This brings in the utility of diversification, which potentially reduces they overall volatility of the portfolio. But all these assumptions failed to hold in the 2008 crisis, primarily due to liquidity needs. Many institutions have set limits at which they can maintain a losing investment before the position needs to be liquidated. Those limits where met simultaneously across many assets, creating a downward spiral in price as so many investors tried to exit their positions all at the same time.

Yet the portfolio return for the Yale endowment in 2008 was a remarkable 4.5% against a broad market return of -35.63% when looking at the performance of the S&P 500 over the same period. That year the endowment’s allocation to equity was a total of 25.1% of which 10.1% was domestic. It almost goes without saying even though Real Estate suffered just as much, a higher allocation to alternative investments would have probably given the Yale endowment an even higher return. It’s not surprising then that their portfolio has remained heavily weighted towards alternative assets.

Tenets Of Portfolio Construction

There are typically three aspects of portfolio construction, Asset Allocation, Market Timing and Security selection. David Swensen argues that in reality the most important of the three is Asset Allocation, as the other two are zero some games. Market timing involves buying an asset just before it goes up or selling just before it goes down, therefore if you are on the winning side of that trade someone must be on the losing side. Security selection is also very similar, in this case it’s about picking the security that will out-perform the market, so if you over-weight Ford and under-weight GM and ford goes up faster than GM then you have a higher return. But this also means that someone else has the opposite position and again it is a zero sum game. Asset Allocation which leads to a well diversified portfolio is more likely to withstand broad market shocks, as can be seen from David Swensen’s return for 2008 of 4.5%. At times of crisis, like in 2008, you may see the diversification benefit diminish, but it would seem to pay in the long run.

What is necessary is a thoughtful approach and a good understanding of what your liquidity needs will be , not just now or for next year but on a continuous basis. Endowments typically only need to spend a small percentage of the fund per year, as long as they can produce returns that exceed that percentage plus inflation they are actually adding to the capital of the fund. Holding capital in assets that may be needed before the investment matures can be extremely damaging to the performance of a portfolio.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst