Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Getting your kids in the habit of investing at an early age can help them maintain and grow their wealth once they start working. When it comes to investing, possibly the biggest factor that will create success is the time horizon. The longer your investment lasts, the more chances you will see your savings pot grow.

In this article, we’ve provided an overview of stock investing for kids, the best stocks for kids, and how to get started building intergenerational wealth in the most tax-efficient manner possible.

How Old Do You Have to Be to Buy Stocks?

Kids certainly have plenty of time, and that only goes in their favor. Any 20-year or 30-year period you can pick, if you stay invested you will always come out on top. What kids need to understand is the difference between investing and speculating.

One way to get your kids started is to open a custodial account. Depending on the state they can only have their own account from the age of 18 or 21. Until then, you would have to be in control of the account. Or you can open an SDIRA in your name and keep control of the assets until it’s time to transfer them.

We will look at types of accounts a bit later, but you will probably need to garner their interest before you set that up. You’ll also need to educate them a little on the matter of investing, so they at least know the basics.

Let’s keep things simple

Start by getting their attention, maybe you know which gadgets or devices they are into. For example, you know they love Apple. A simple question like “How would you like to own a part of Apple?” Something that sparks their interest.

The next step is explaining the parts that make up the world of stock investing. Start with explaining what stocks are, then move onto the stock exchange, then funds, and finally indices. We’ll see a bit later why you need to explain the last one.

You might find they have a lot of questions. Remember they probably don’t know many of the words or concepts you take for granted. So, bear in mind that you need to explain everything from square one.

Investment Versus Speculation

It’s very easy for kids to get excited and get carried away with the Wall Street complex and imagine themselves becoming stock tycoons. The first concept we need to explain to them is that there is a very large difference between investing and speculating.

The concept of investing involves buying and holding assets for the long term, based on fundamental analysis. Speculation, on the other hand, is a short-term activity, and very risky. This activity is remarkably like gambling.

Here, having explained what a fund is, you can also guide them into considering buying shares in ETFs or mutual funds. This way their money is managed by professionals. And their money will be invested in tens or hundreds of different companies. They should catch on quickly, that not having all your eggs in one basket is less dangerous than having invested everything in a single stock.

Regular Payments

Making regular payments into their accounts will help keep them interested. It will also create the habit of saving, and hopefully they continue it when they have their own incomes. It’s good practice to allocate some of their revenue into their investment accounts.

Making regular payments means that they will be investing as the stock markets go up and down. Getting some shares at discounted prices is always a good thing. We have seen that time and time again no matter at what price you bought the broad stock market you will eventually make a profit.

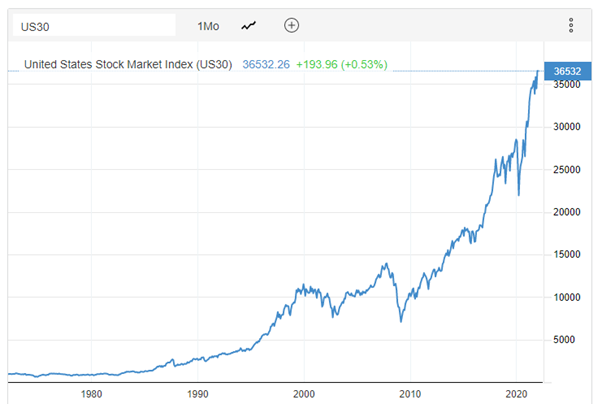

The chart below shows the stock market performance of the Dow Jones Industrial Average over the past 50 years. Take any 20-year period and at the end of it, you have earned a positive return. Whether you bought at the peaks in 1987, 1999, or 2007 just by staying invested you would have come out on top.

Source TradingEconomics

This is where you need to have explained what an index is. It is not always obvious for kids to understand what it is. As a starting point, the definition: Average price of a set of stocks quoted on an exchange, seemed to work for my kids.

Investing for Growth

You may be an investor who likes to pick their own stocks and has a diverse portfolio. Perhaps you want to transfer your portfolio construction skills to your kids. A good option is to concentrate a larger allocation of the portfolio to blue-chips and growth stocks.

Your kids have a relatively long-term investment horizon and should benefit greatly in the long run from these stocks. For growth stocks consider companies that have a long runway, adding extra value later on. Investing in blue-chips will make sure their money is in companies that last and that have top-tier governance.

Another way is to choose cheaply priced ETFs or funds that invest in growth stocks. Growth funds will usually track a benchmark such as the Russell Midcap Growth Index. While blue-chip funds should track the Dow Jones Industrial Average Index.

In either case, you should get your kids to participate in the research. The work you do with them will help them understand the mechanisms of investing. Hopefully, this knowledge will help create good investing habits. It will also teach them plenty of investing and financial terminologies. Knowing the jargon should make it easier for them when they want to decide about investing on their own.

How Much Will I get?

That was one of the first questions my kids made. In their opinion they saw saving a few hundred bucks a month to invest in stocks simply wasn’t worth it. It seemed futile to them. In the end, it would be better to have that money in their pocket when they reach earning it.

I did some calculations and produced the table below considering a 1% monthly growth rate. I calculated how much your money would grow with 3 different amounts for 20 and 30 years. I used the 1% monthly growth rate because I saw it as a prudent estimate. The Dow Jones has grown 439% over the past 25 years. That’s an average of 17.2% per year.

As you can see, the more money we commit to our investment pot the greater the benefit at the end of the two periods. But when we consider each amount for 20 and 30 year investment periods, we see that staying invested for an extra 10 years more than triples your investment for 20 years.

Of course, no one has a magic ball, and we cannot foresee how well the general stock market may perform in the future. But past performance may give us some clues. It certainly looks like being invested in a broad portfolio of stocks can bring its benefits.

Investing Rules

The famous 80/20 stock-bond split rule has many detractors as well as pundits. Personally, I’m all in favor of this asset allocation strategy. The rule is derived from subtracting your age, or your child’s age, from 100. So, if your child is 20, then 100 minus 20 equals 80 and that is the percentage of funds that should be in stocks.

I’m in favor of this rule simply because, in the long run, with a broad allocation in many diverse stocks your investment will likely be a positive one. And our kids have a very long investment horizon.

Needless to say, 80% is the percentage of funds you have allocated to traditional assets and doesn’t consider your allocation to alternatives. To this rule, I would also add the 10% rule, which is to save a small percentage of your income monthly.

This factor is often overlooked. To get them to invest when they start working, they also need to understand they need to save. Saving as little as 10% of income for investments can be highly rewarding and will go practically unnoticed.

Custodial Accounts

A custodial account allows you to put money into an investment account in your child’s name, while you stay in control. The money you transfer into this type of account is to all affect the property of your child. Until they reach the age of 18 or 21, depending on the state, they will not be able to take control of the funds or assets in the account.

You will not be able to withdraw the funds from the account once you have paid in. There are exceptions for certain expenses you may have to make for your child. These expenses may not include day-to-day costs, such as food or clothing.

If the occasion arises, it may be worth speaking to a financial advisor or attorney before spending money from a custodial account. Incorrect use of funds from an account in your child’s name may be cause for legal penalties, other than replacing the money that was in the account.

Types of Accounts

What type of account you open for your child will depend on whether they have earned income or not. And whether you wish to stay in control of the funds for as long as you wish, with an IRA. Or you would rather hand over control when they become 18 or 21, with a custodial account.

The most popular investing apps for teens and youngsters like Robinhood don’t offer custodial accounts. You wouldn’t be able to make tax-advantaged contributions, and you wouldn’t be able to have control.

Custodial Accounts

If your child has earned income, you can open a custodial IRA in their name. You will be able to decide which types of investments you want to hold in these accounts. The funds remain the property of your child, once they reach adulthood, they will be able to take control of the account.

There are limits as to how much your child can contribute to the IRA. The limit is currently at $6,000 of their earned income. For example, if your child earned $5,000, they could contribute the full amount, if they had an income of $10,000, they could contribute up to $6,000.

For children that are most likely to have a higher tax bracket later in life a Custodial Roth IRA is more advantageous. Roth IRAs allow for after-tax contributions, meaning they pay little or no taxes when making the contributions. When your child eventually withdraws the funds, they won’t be paying the higher tax rate.

If your child has no earned income, then you may want to open an investment account under one of the following arrangements:

Uniform Gift to Minors Act (UGMA) Account

This type of account allows you to make contributions in your child’s name such as cash, stocks, bonds, or insurance policies. The money you invest in these accounts belongs to the child, while you keep control of the funds until they reach 18 or 21, depending on the state.

Uniform Transfer to Minors Act (UTMA) Account

This type of account is the same as the one mentioned above. However, with this type of account, you will be able to make investments in any type of asset, including physical assets such as real estate. Each state determines which types of assets can be included in these accounts.

Taxes paid on the incomes of these accounts will depend on the normal tax rate of both the custodian and the beneficiary. If your child is under 19, or under 24 and a student, the tax rate will be the following:

- Up to $1,050 of unearned income no tax paid

- Over $1,050 the child’s tax rate applies

- Over $2,100 the adult’s tax rate applies

Keeping Control

Another option is to open a Self-Directed IRA which will allow you to stay in control of the assets until you need to use them. The main difference between a self-directed IRA (SDIRA) and a normal IRA is that the former allows you to invest in a vast array of assets.

You can hold physical assets such as precious metals, real estate, or commodities with an SDIRA. The same limits apply to the amount of money you can contribute yearly. You will also be able to choose between a Roth or standard contribution.

Having full control of the funds you contribute might be an option for some parents especially when your children are younger. Plus, SDIRAs let your stock gains appreciate in value on a tax-free or tax-deferred basis. You can still get your kids involved in the investment process. With an SDIRA you can pick and choose with your kids among a variety of traditional and alternative assets.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst