Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

In theory, the recent rebound in equity markets—especially in technology-related shares, which were major laggards as the year unfolded—should be great news for young companies.

As discussed previously (see here and here), valuations, activity and interest in private market growth businesses and initial public offerings have been subdued, to say the least. But with investors seemingly upbeat again, it is only natural to think that finance-hungry startups should be seeing a corresponding improvement in their fortunes.

Unfortunately, that does not seem to be the case. While there are signs of hope, they are few and far between.

Not Coming to Market

Take the IPO market. Normally, a growing appetite for stocks, as evidenced by a resilient secondary market, would see investment bankers rushing to bring deals to market. So far, the opposite has held true. As CNBC recently reported, “Initial public offerings are at a standstill in the U.S.”

Specifically, the business news channel noted that “there have been no IPOs on the New York Stock Exchange since December 18, when financial technology company Yirendai went public, marking the second-longest drought in the exchange’s history, according to Dealogic, a New York-based financial services firm.” The last time such a drought occurred, CNBC added, was during the financial crisis.

Not helping matters has been the ongoing fallout from LinkedIn’s disastrous fourth quarter earnings report, released in early February. The shares of the former high-flyer, which came to the market in 2011, crashed 44% after the company announced disappointing fourth quarter results and weaker-than-expected full-year guidance. Although LinkedIn has had a modest bounce since then, the effects of its negative surprise are still being felt, particularly among younger and smaller technology firms.

Unicorns Losing their Horns?

The pre-IPO market, notably the $1-billion-plus “unicorns,” has not shaken off the doldrums, either. Since the troubles in the segment were first highlighted (see here and here), newsflow has been more negative than positive. An article at Quartz sums things up:

Each week brings fresh bad news for Silicon Valley’s would-be “unicorns.” There are layoffs at LivingSocial, warnings about LinkedIn, and pivots at valet-parking startups. The “Uber for X” model rarely works except when X = Uber. Valuations are shrinking, funding is falling, and there’s ill-concealed glee at the signs that yet another tech bubble is, if not exactly bursting, at least looking distinctly deflated.

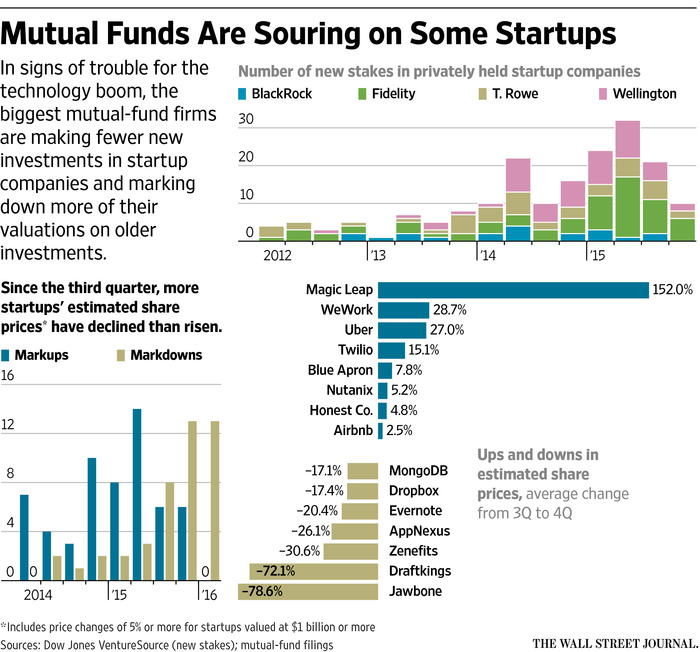

Questions about valuation continue to dog the private market. As detailed previously, some major participants have been steadily downgrading internal expectations. According to the Wall Street Journal, “BlackRock Inc., Fidelity Investments, T. Rowe Price Group Inc. and Wellington Management run or advise mutual funds that own shares in at least 40 closely held startups valued at $1 billion or more apiece.” An analysis by the newspaper found that “for 13 of the startups, at least one mutual-fund firm values its investment at less than what it paid.”

An uptick in down rounds

But it is not just estimates that are moving lower. News regarding the latest financing rounds for some well known unicorns suggest that investors are becoming more demanding with respect to pricing and other terms. BuzzFeed News recently reported that cloud storage startup Dropbox was facing questions about its valuation because of plans “to authorize a sale of its common stock at a 34% discount to its most recent round of private funding,” which took place in January 2014.

Expectations that a number of private market startups will be lining up for additional funding starting later this year is heightening uncertainty. Based on an analysis of VC data, CB Insights found that “over 60% of unicorns will likely need to raise their next round of capital in the next three quarters, [while] nearly 4 of 10 US unicorns will need to raise in the final two quarters of 2016.”

Finally, reports that current and prospective employees of start-up firms are growing nervous and paying more attention to company financial matters only adds to worries about the state of the private market. A Wall Street Journal article, “Tech Workers Get Choosy About Changing Jobs,” notes that many in Silicon Valley are playing it safe amid “sinking stock prices at some tech firms, falling startup valuations and a chill in venture funding.”

Cause for optimism?

With all of this in mind, does this mean that things can only get worse? Not necessarily. If share prices continue to rally and investors grow enamored with technology again, then it is likely that enthusiasm will spill over into the private market and IPO arenas. In fact, according to a manager of IPO-focused ETFs, one indicator already seems to be signaling that “an end to the IPO drought is in sight.”

The firm, Renaissance Capital, notes that its IPO Index, which tracks the performance of the last two years’ worth of IPOs, has significantly underperformed the broader market from last August through the first half of February. However, the firm believes the recent jump in the index, up about 14% since then, indicates “‘that investors are looking at the existing set of IPOs and coming in with more confidence buying them”–in other words, the “window of issuance” will soon reopen.

That said, it is hard not to doubt that the situation will improve anytime soon. For one thing, the recent recovery in equity markets appears to have largely been driven by short-covering and technical factors rather than fundamentals, suggesting it lacks staying power. There is also the fact that interest in startups has, historically speaking, been somewhat cyclical, and that the reversal of fortunes that began last year potentially marked a major peak.

Time will tell, of course, but for now, caution remains the watchword.

Michael J. Panzner is a 30-year Wall Street veteran and the author of three books, including Financial Armageddon, which predicted the 2008 global financial crisis.