Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

The report released recently by Prequin shows how institutional investors are increasing their allocations to alternative assets and intend to continue increasing allocations in the future also. Infrastructure, Private Equity and Debt come out as being institutional investors’ new favorite asset classes. Investments in Alternative Assets grew by $500 million in 2015, reaching an all-time record of $7.4 trillion, according to Prequin. The report surveys 460 institutional investors from around the world, 42% of investors were from North America, 35% from Europe, 15% from Asia Pacific and 8% Rest of World. Breaking down investors by type, 35% were pension funds, either private or public while Insurance companies and foundations each represented 10% of investors surveyed. Other categories were smaller than 10%.

Increase in Allocations to Alternative Investments

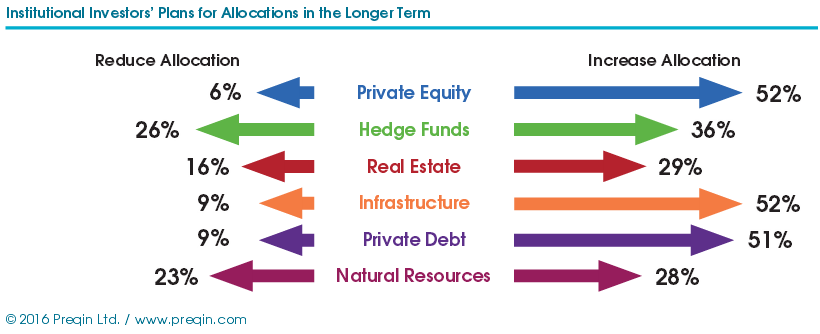

Amongst the investors surveyed 79% held investments in at least one Alternative Asset class. The most popular Alternative Asset was Real Estate with 66% of institutions holding allocations to this type of investment. When asked about their intentions for long-term allocation plans in the Alternative investment space; 52% said they would invest more in both Private Equity & Infrastructure, and 51% said they intended to invest more in Private Debt. The asset which investors intended to decrease allocations in the long-term the most was Hedge Funds at 26%.

When asked about how they would allocate in 2016, investors showed a very similar preference to their long-term intentions for increases in Alternatives. 48% said Infrastructure would receive more investments than the previous 12 months and 45%, and 43% said they would invest more in Private Equity and Debt respectively. The Asset class that investors intend to reduce the most in their portfolios is Natural Resources. This reduction may be due to the underperformance relative to other assets and a decline in excess returns over more recent years. Worthy of note, however, that Timber futures have had a great start to the year with a YTD of 21.4% and so far this month alone, have increased in price by 22.1%.

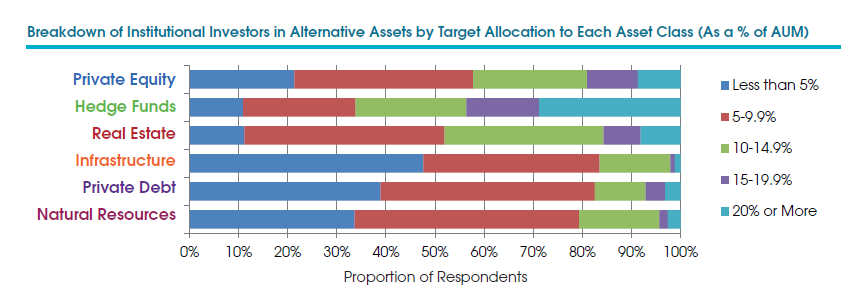

Allocations to most Alternative asset classes remain fairly modest compared to Traditional asset allocations. The most popular allocation range is still below 10% for more than 80% of institutional investors in Infrastructure or Private Debt and for slightly less than 80% of investors in Natural Resources.

Satisfaction driving allocation increases

Taking a look at the Investor satisfaction and performance of various Alternative assets may explain why the increase in intended allocations to certain investments. In the case of Private Equity, of 100 investors surveyed 65% said that they had a positive perception of the industry, while only 6% said they viewed the sector negatively. A lot of that satisfaction probably comes from record levels of distributions, cash paid back to investors, compared to capital invested. In fact, 95% of the investors surveyed had higher expected returns for their Private Equity portfolios than for Public Equity.

Infrastructure still shows a high level of satisfaction; with 77% of investors interviewed saying their investments had met or exceeded their expectations for 2015, last year that percentage was 86%. In terms of perception of the industry, 56% of institutional investors have a positive view of this sector. As this asset class becomes more familiar and more investors are involved there should be an increase in interest. Positive sentiments will help the industry achieve growth, and when considering confidence in this asset class to meet expectations in the future, 64% stated there had been no change in their confidence while 23% stated their confidence had increased. Infrastructure investors tend to be extremely large 74% of institutional investors had at least $1 billion in assets invested in this space. Sophisticated Investors shouldn’t be deterred by this, as there are various publicly listed infrastructure companies out there.

In the Private Debt class 68% of investors felt their performance expectations had been met over the past year, while 18% responded they had been exceeded. In terms of industry perception a healthy 54% stated they viewed the industry positively at present. The current state of the private and public credit market is probably conducive to a positive sentiment of this sector.

Strategies most targeted

For Private Equity the strategy, according to investors, which offered the most promising opportunities in 2015, was Small to Mid-Market Buyout funds. Last year 61% percent of investors found that strategy to offer the best opportunities. Expectations for 2016 show the trend continues, 73% of investors say they are seeking to invest in this area. All other strategies also see an increase in the number of investors who intend to invest for next year. Intentions for investing in Venture Capital over the next year are on the increase, rising from 24% to 31%. The second most popular strategy for the following year will be Large to Mega Buyouts rising from 21% to 36%.

In Private Debt 60% of investors say they intend to commit part of their portfolio to mezzanine funds over the next 12 months. While the largest amounts of capital are being sought for Distressed Debt funds, with $45 billion in fundraising. This increase is in line with investor intention to commit to this area, which has risen since last year, from 53% to 64% of investors.

A bright picture

Overall the report paints a rosy picture for the three asset classes with the largest intentions from institutional investors to allocate larger portions of their portfolios to these alternative investments. As allocations to Alternative Asset classes increase, I see the endowment model becoming the model portfolio of many institutional players. Which for some investors with easier liquidity demands probably makes sense, and for sure this portfolio model has worked very well for colleges like Yale or Harvard amongst others.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst