Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

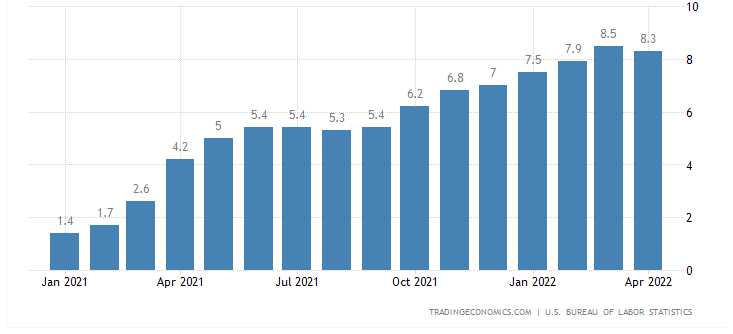

We keep seeing headline news telling us inflation is higher than ever for a generation. The last inflation data shows that prices have increased by 8.3% as shown by the Consumer Price Index. We can see it coming, but inflation risk is hard to determine for duration and depth.

This bout of higher inflation started in April 2021, when it suddenly jumped from 2.6% to 4.2% in one month. The rise in inflation and inflation risk has continued to grow steadily. In fact, many economists and market pundits are sure that higher inflation is here to stay for a while.

Source: TradingEconomics

And worse yet, many also believe this bout of higher inflation will also occur with an economic slowdown. The combination of the two, known as stagflation, would have a damaging effect on the livelihoods of many, as well as punish the broad stock market.

Experience of Inflation Risk

The last period of stagflation which started in the 1970s, and continued throughout that decade, is a stark reminder of what may happen. We can’t know for sure, but history tends to repeat itself and economic cycles also.

By December 1973, inflation had jumped to 8.71%, and the S&P 500 was at 610.09, down 24% from the previous year. As inflation continued to rise to 12.34% by December 1974, the S&P 500 fell another 37.5%. By the time the inflationary period was over in December 1981, the S&P 500 had fallen to 376.96, or 53%.

So, we are going to have an in-depth look at inflation risk and answer the most common questions:

- What causes inflation?

- How long will high levels of inflation last?

- How does inflation risk affect the financial markets?

- How can I hedge against inflation risk?

What Causes Inflation

Various reasons can cause inflation. In simple economic terms, greater demand for goods and services can push prices higher. This happens until manufacturers and suppliers can adjust and catch up with new levels of demand.

This type of inflation is linked to an expanding economy and is seen as healthy, as long as inflation is not excessively high. However, we are in a different scenario from anything we have seen before. The measures the government took to fight the pandemic greatly reduced the country’s capacity to produce goods.

And with the Federal Reserve now in the need to unwind its quantitative easing. The Federal Reserve needs to drastically reduce its bond holdings and increase interest rates. Both measures are going to put a strain on the economy.

The general shutdown of much of the economic activity has now produced a glut as people have started going back to their everyday lives. Manufacturers and suppliers are racing to be able to match the demand. And then the invasion of Ukraine put greater pressure on the price of commodities, such as wheat, natural gas, and iron ore.

How long will high levels of inflation last?

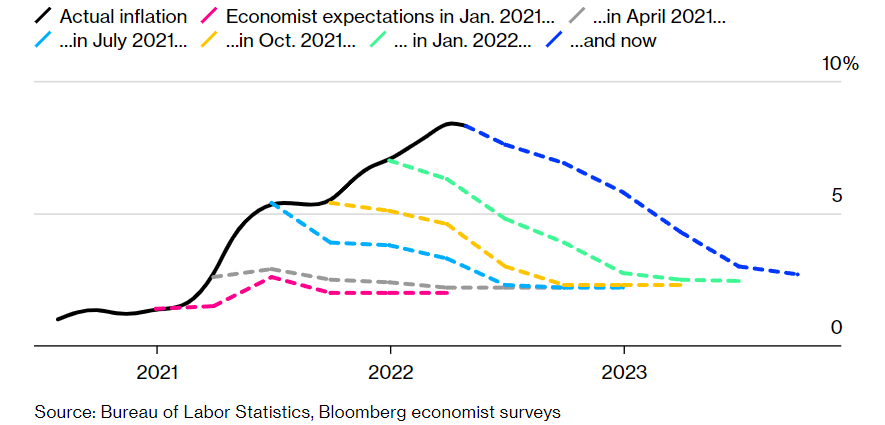

This is a tough question to answer with any real precision. A lot of economists try to put a timing on when inflation risk will recede, and price increases begin to slow down. But it is no easy task. One thing is for sure, over the past months since January 2021, economist expectations have been for inflation to rise and stay for longer.

The chart below shows economists’ expectations for inflation over 6 different periods since January 2021. You can see that as time has progressed so have their forecasts for higher inflation and longer periods.

Source: Bloomberg

How long inflation will last depends mainly on two factors: clearing the supply chain glut and the speed of interest rate hikes. The former is in the hands of private entrepreneurs for the most part. While the latter depends on the Federal Reserve’s balancing act. They need to dampen inflation by increasing interest rates, yet they also need to consider the adverse effects on the economy if they do it too quickly.

How Does Inflation Risk Affect the Financial Markets?

Inflation risk can negatively affect most financial markets, we will have a look at how further down. However, some securities are better positioned to bear the negative effects of inflation than others.

Inflation Risk in the Stock Markets

High inflation by itself is not necessarily a bad thing for the stock market. But it can be punishing when the factors causing the inflation are coupled with supply constraints leading to an economic slowdown.

As mentioned above stagflation does not bode well for the broad stock market. In the current scenario, there is also another factor that will weigh heavily on stock prices. Company balance sheets have profited from historically low interest rates. And corporations have had access to extremely cheap money for more than a decade.

This factor leads me to believe that companies with a high debt ratio will suffer the most. However, corporations, in general, will be limited in financing new operations as higher interest rates may eat into their profit margins. If they see a smaller potential profit from financing new operations, they most likely will postpone these new business activities.

Inflation Risk in the Bond Market

Inflation risk has a negative effect on the price of bonds and treasury notes. Bond prices are inversely proportional to the yield. So, if inflation rises bond investors will want to buy bonds at a lower price to increase the bond’s yield to reflect the higher inflation rate.

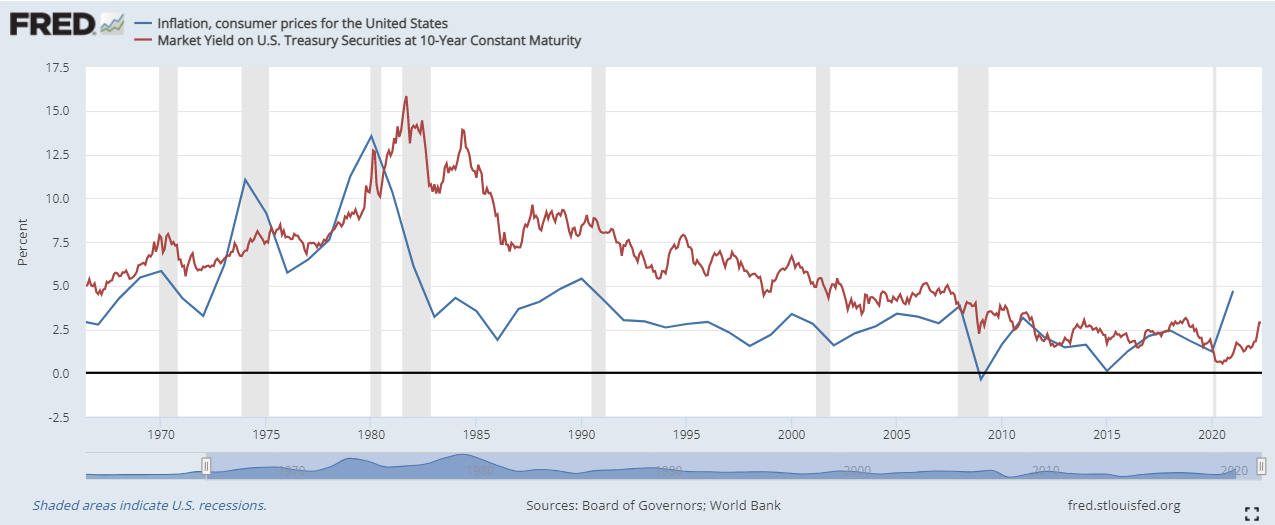

Currently, the 10-year Treasury note yield is around 2.86%, which is considerably below the inflation rate, for the moment. From the chart below we can see how the treasury yield has been higher than the inflation rate for the most part. Yet we haven’t seen treasury yields get anywhere near the inflation rate for now.

Source: St.LouisFed

The bond market may perceive the inflation risk as low, and therefore a 10-year Treasury note may outlast the current higher inflation rate and still yield a positive real interest. The real interest rate is important because a yield below the inflation rate means you are actually losing money.

If high inflation rates stay around for long enough, the price of Treasury notes will at some point fall to adjust for the higher inflation risk. The current 10-year Treasury note is priced at around 100, meaning that for every $1,000 of this note you will pay $1,000.

However, for the price of this note to yield a rate that is more in line with current inflation, it would have to drop to around 80. This price level would give the note a yield to maturity of 5.5%, still not above the current inflation rate but a lot closer. Most importantly that would be a drop of 20% from current prices.

Inflation Risk for Real Estate

Real estate can fare well in moments of high inflation risk, depending greatly on how much the economy is affected. The resilience of real estate comes from the fact that rental contracts are adjusted for inflation. So, every 2 or 3 years most rental contracts will automatically increase the rent on the property.

This feature is valid as long as the economy does not shrink by a large amount. Most people, including companies, will tighten their belts a little to continue in their current dwellings. Moving your residence or business to a new location has many costs and undesirable efforts. Usually, changing places is the last resort option.

However, homeownership will be hindered by higher interest rates as banks will have to charge more for their mortgages. REITs that rely on equity revaluation rather than rental incomes may be adversely affected. So, it’s not so obvious what the outcome may be for real estate overall if inflation risk continues to rise. At least it is not as clear as the outcomes for stocks and bonds.

Inflation Risk for Precious Metals

Precious metals are considered a natural hedge against inflation. Gold in particular, as other precious metals have a higher usage in industrial and manufacturing processes. Gold is probably the most sought-after precious metal when it comes to investing.

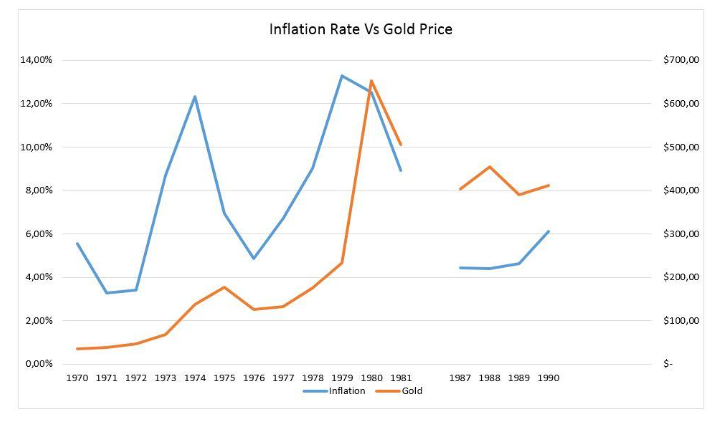

In previous high inflation periods, the price of gold managed positive returns. The past high inflation risk periods refer to two periods from 1973 to 1980 and from 1987 to 1990. In the first extended inflationary period, gold rallied from around $78 an ounce to just over $650.

Source: MacroTrends

The stagflation period of the 1970s was a prolonged one, which also saw the gold standard dropped, and the price of gold free to float from 1973. However, gold’s performance despite the constant rise in prices was constant and to be expected. If you hold a finite and valuable asset and dollars are worth less, then you would want more of those dollars to compensate for its decreased value.

Inflation Risk for Cryptocurrencies

Cryptocurrencies have not been around long enough to make comparisons during previous inflationary periods. So, with this asset gauging inflation risk is harder since we lack enough historical data to compare past performance.

Cryptocurrencies are a high-risk asset, and we know very well how prices can fluctuate with sharp drops and gains. So, in an environment where investors are looking for less risk, this asset may be suffering due to the risk-off appetite of investors.

The current sell-off in digital coins may therefore be a consequence of intrinsic factors and less one of inflation risk. However, cryptocurrency investing is seeing an increase in demand by institutional investors. While the use of digital coins such as Bitcoin is seeing greater adoption.

Source: TradingView

Having said that, we can see from the chart above that during the initial phase of rising inflation Bitcoin managed to continue rising in price. With the main sell-off happening in late 2021.

Hedges Against Inflation Risk

As we have seen some assets may fare better than others when looking for protection from inflation and a possible economic downturn. Let’s have a look at how you can access these assets and some implications for holding them in a portfolio.

Inverse Bond ETFs

This type of ETF invests in bonds but takes short positions in the asset. By taking short positions the fund will benefit from higher interest rates as the market perceives a higher inflation risk. Bond prices will have to decline for investors to receive a yield that is higher and compensates them for a higher interest rate environment.

ETFs of this type can invest in a specific maturity say 10 or 20 years and target the bond issues of a specific government or company. For example, the largest inverse bond ETF on the etfdb.com database is the ProShares UltraShort 20+ Year Treasury ETF.

This fund targets 20-year or longer treasury notes from the US government through the Barclays Capital US 20+ year Treasury Index. The ETF uses a leverage of two. So, the fund has double the exposure to its short positions. Remember that leverage magnifies returns but also magnifies losses. However, if you are considering investing in a fund of this type, the easy way around the extra leverage is to buy fewer shares.

Physical Gold & Gold ETFs

Holding physical gold has the added benefit of not carrying any kind of corporate risk. You own the gold, and it is safely stored and literally indestructible. It is a buy-and-hold long-term investment, which means you need to practice some patience. Most importantly, as seen above, gold seems to have a capacity to protect against inflation risk.

However, long-term historical charts show that gold has only risen in price. Although we are still not past its all-time high of over $2,000 it is fairly close, with the current gold spot price at $1,842.20. If you don’t want to take care of owning physical gold, you have the option of gold ETFs. These funds invest in physical gold and store it safely.

Of course, you do have corporate risk from investing in an institution. However, you can also invest in relatively small amounts and sell your investment quickly if the need arises. For example, the SPDR Gold Shares is the largest gold ETF with $61.15 billion in assets.

Portfolio Diversification

Investing in assets such as the ones mentioned above allows you to diversify your portfolio. Diversification brings you the benefits of lowering the overall risk on your portfolio. When you add alternative assets such as precious metals or Inverse Bond ETFs you gain exposure to investments that have a very low correlation to stocks and bonds.

In the case of gold, the correlation of returns with traditional assets such as stocks and bonds is very low. While the correlation between the inverse bond ETF and the Bond market is inverse, and by logic would also be inverse to the stock market.

Wrapping Up

We do not doubt that recession fears and inflation risk are on the increase, as talked about by various pundits. However, as mentioned above there are ways to hedge your portfolio against the adverse effects of inflation and stagnation. We haven’t covered all the possibilities, but we have had a look at a couple of the more popular and well-tested strategies.

You may want to hold these assets in an IRA to take advantage of an enhanced tax environment. To invest in the assets mentioned above you would need to open a Self-Directed IRA. Several companies offer top-notch and specialized services. You can get more information in our top self-directed companies reviews.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst