Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

In most aspects of life, it’s probably not a good idea to compare yourself to others. Retirement saving is a different story. Knowing how your 401(k) stacks up against your peers’ can help with post-career planning and can help you set benchmarks on the road to retirement.

The average 401(k) balance across all Fidelity accounts in the U.S. reached a record-high of $112,300 in Q1 2020, which is up from $105,000 in the previous quarter. Don’t fret if you’re not quite there yet—the averages vary widely by the account holder’s age.

Let’s take a look at how your retirement savings compare to those in your age group. Below, I’ve listed the average savings by age in 401(k) accounts as of Q1 2020 according to the most recent data available from Fidelity Investments.

Twentysomethings (Ages 20-29)

- Median 401(k) balance: $5,000

- Mean 401(k) balance: $13,200

- Average income contribution: 7%

Half of 401(k) account holders in their twenties have less than $5,000 in retirement savings. Although this might not sound like much, it’s a respectable start to build on.

We’re often asked by young investors, “How much should I contribute to my 401(k) in my twenties?” As a rule, saving 15% of your pre-tax income from the outset of your career will help you build a solid nest egg even with a low initial income. In this age category, your youth is your greatest asset—over a multi-decade time horizon, even modest monthly contributions can grow into sizeable savings if the money is well-invested.

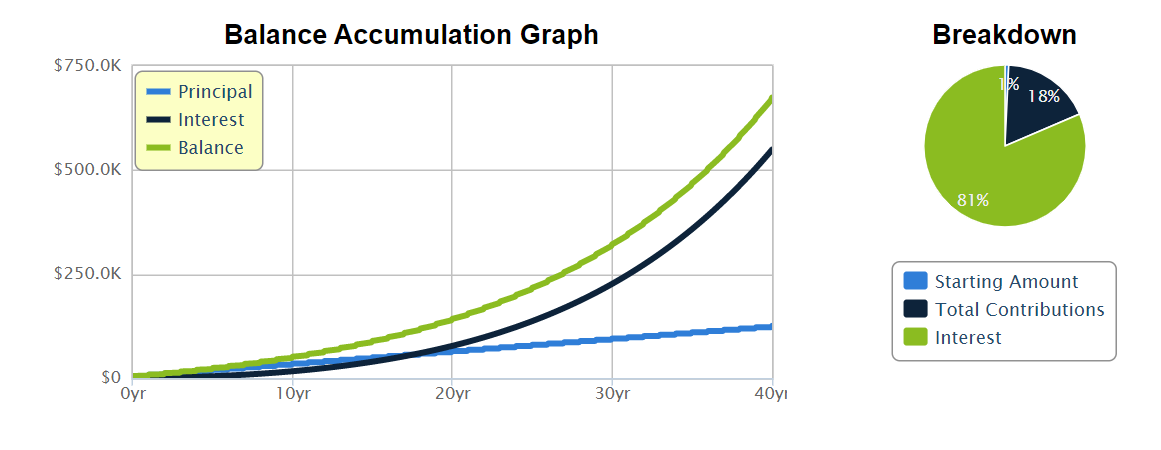

Let’s assume I’m a 25-year-old with $5,000 in savings and I plan to retire at 65. If I invest an additional $3,000 annually ($250 monthly) over the next 40 years and assume a 7% annual rate of return, I’ll hit retirement age with over $673,000 banked, mostly due to returns on the principal, as depicted by the charts below.

Source: Calculator.net

Thirtysomethings (Ages 30 to 39)

- Median 401(k) balance: $18,500

- Mean 401(k) balance: $46,200

- Average income contribution: 8%

In this age category, the mean 401(k) pulls away from the median considerably. This observation is the result of high-income earners skewing the average by contributing far more to their retirement accounts with low and middle-income earners.

According to Fidelity, you should have about three times your starting salary saved in a retirement fund by age 40 to sustain your pre-retirement living standard. To hit this mark, aim for an annual contribution of at least 15% of your gross earnings to your 401(k) during your thirties.

Fortysomethings (Ages 40 to 49)

- Median 401(k) balance: $39,200

- Mean 401(k) balance: $111,100

- Average income contribution: 8%

High net-worth individuals continue to skew the mean 401(k) balance well above the median among those in their forties. Equally notable is that the average contribution to one’s 401(k), as a percentage of gross income, doesn’t budge over 8% in this age cohort.

Fidelity Investments recommends having about six times your salary saved by age 50, which would require most retirement savers in this age category to save above 15% of their pre-tax salary every year.

Fiftysomethings (Ages 50 to 59)

- Median 401(k) balance: $65,300

- Mean 401(k) balance: $188,000

- Average income contribution: 10%

Your fifties are your peak earning years, which means you should scale up your annual 401(k) contributions in step with your increased discretionary income. For many, socking away 20% of one’s gross pay to retirement savings is an achievable target, especially after one’s mortgage is paid off.

When you reach age 50, your 401(k) contribution limit rises by $6,500, which allows you to invest more for your retirement in a tax-advantaged account. By the end of your fifties, aim to have at least eight or nine times your gross salary saved in your 401(k).

Sixtysomethings (Ages 60 to 69)

- Median 401(k) balance: $67,600

- Mean 401(k) balance: $212,600

- Average income contribution: 12%

Retirement savers in their sixties should insulate their retirement portfolio against volatility by investing across a variety of alternative asset classes. When you have less than ten years until your retirement, it may be wise to practice strategic wealth preservation by reallocating a greater share of your portfolio to low-risk government bonds and precious metals.

As we’ve seen with the 2020 bear market and subsequent recession, the U.S. equities market can quickly lose value and tank your retirement savings. To protect your portfolio against financial risk in the equities market, ensure that you’re properly diversified across alternative and traditional assets.

What Does The Average 401(k) Balance Mean For You?

Admittedly, not very much. Knowing average savings by age group can help you keep up with the Jones’s, but it won’t shed any light on your own saving habits or financial outlook. Aggregated data lets you know whether you’re lagging behind your peers, but is too general for drawing actionable conclusions.

There are three principal biases that abound in aggregated 401(k) data.

First is the inclusion of outliers, which skew the way we perceive national averages. Retirement savings accounts with values that are abnormally higher than other values in a distribution—such as that of, say, high net-worth millennials like Joe Gebbia (Airbnb) or Elizabeth Holmes (Theranos)—will create observations in the data that are unrepresentative of the population.

In other words, extremely wealthy individuals pull the average well above the median, which is the middle number in a sorted list of data.

The second is selection bias, which occurs when data is selected subjectively and may not be a good representation of the population. In this case, many workers (in fact, at least 10% of the U.S. workforce and 41% of millennials) do not have access to employer-sponsored retirement plans. There are many who are self-employed, for instance, who are saving for their retirement but whose savings are not represented in the national average.

The third bias is that some people choose not to roll over their 401(k) from company to company and instead hold multiple retirement savings accounts. Therefore, the combined value of their multiple accounts is not represented in the data.

Worried About Retirement Saving?

Don’t count on Social Security checks to get by during your retirement. Saving ten times your final annual salary by retirement age will help you preserve your pre-retirement standard of living and will provide peace of mind in the event of a medical emergency.

Knowing the average savings by age can help you stay on track to make your retirement savings goals. However, without diversifying your portfolio and protecting yourself against market risk, you stand the chance of losing the nest egg you’ve worked so hard to acquire.

To achieve true long-term diversification, consider supplementing your 401(k) with a precious metals IRA. Diversifying across alternative assets can help protect your life savings when equities markets dip or enter a bear market, as we’ve seen in Q1 2020. A well-diversified portfolio will minimize loss, safeguard your wealth from adverse market cycles, and will help you retire earlier and wealthier.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.