Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

It was big news on Wall Street when the California Public Employees’ Retirement System announced just over a year ago that it was planning to axe its $4 billion stake in hedge funds, saying that they were “too expensive and complex.” Calpers is America’s largest public pension fund, with around $300 billion in assets, and it has often been seen as both a bellwether and pacesetter for other institutional investors. Many viewed the decision as the beginning of the end for hedge fund investing.

Indeed, in the wake of Calpers’ announcement, other institutions moved to either reduce their exposure or reconsider investments in the space. Among those on the list were the Teacher Retirement System of Texas, which manages $132 billion, the School Employees Retirement System of Ohio, New Jersey’s State Investment Council, and the city of Austin, Texas police retirement fund. In sum, it appeared that the hedge fund doomsayers were right, and that the outlook for the industry was anything but positive.

But events since then suggest that this is not the case. For one thing, there have been a number of public and private sector fund managers who have not only indicated that they will stick with hedge fund investing, but who will be looking to increase the amounts they allocate. In February, for example, the $20 billion San Francisco Employees’ Retirement System issued a request for proposal (RFP) for a hedge fund consultant, according to Preqin, “prior to making a maiden allocation of 5% of total assets to the hedge fund space. The hiring of managers is expected to take place at the end of 2015 through to early 2016.” In June, the Wall Street Journal reported that companies such as Ford and Intel, which were already major players in hedge funds, remained upbeat on the sector.

Ironically, the most notable of the hedge fund optimists may well be the nation’s second largest pension fund, the California State Teachers’ Retirement System, which oversees $191 billion and whose office is just a stone’s throw away from Calpers’ . According to a September 2nd Wall Street Journal article, Calstrs was considering shifting up to $12 billion away from stocks and bonds to Treasurys, hedge funds, and other investments, in what was deemed as “one of the most aggressive moves yet by a major retirement system to protect itself against another downturn.” The article added that state pension plans currently have “nearly three-quarters, or 72%, of their holdings in stocks and bonds, according to Wilshire Consulting.”

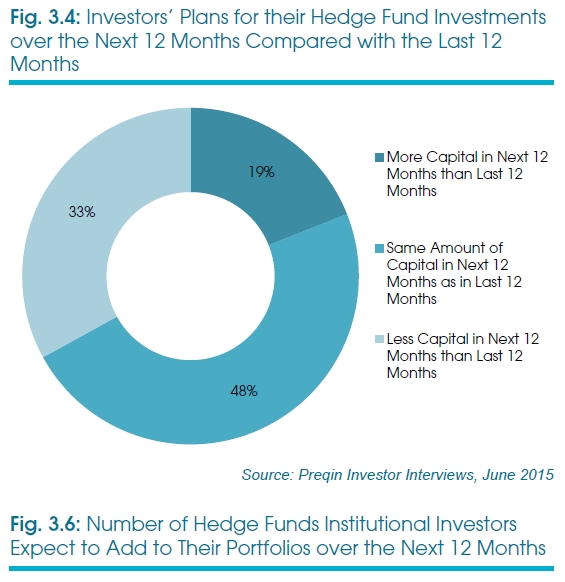

Other data appears to bear out the continuing interest in hedge fund investing. In their H2 2015 Investor Outlook: Alternative Assets survey, research firm Preqin reports that 28% of institutional investors planned to increase hedge fund allocations over the long term, while only 22% were considering a decrease. In addition, two-thirds were planning to invest the same amount or more capital in hedge funds over the next 12 months, as compared to the last 12 months.

Even amid the turbulence that rocked stock, bond, currency and other markets in the late-summer and early-fall, this segment of the alternative investment universe has remained somewhat resilient. While assets fell by $95 billion to $2.87 trillion during the third quarter, representing the first drop in hedge fund capital in three years and the biggest since the depths of the 2008 global financial crisis, total assets under management are still ahead of where they were at the end of 2014, according to HFR, which regularly analyzes the sector. In fact, inflows outpaced outflows by $4 billion during the July-September period.

The reasons why investors remain optimistic on hedge fund investing have not changed that much since institutional interest in the sector first began to grow. According to the Preqin survey noted earlier, three key drivers play a role in the decision to allocate capital to hedge funds: the need for portfolio diversification, the funds’ low correlation to other asset classes, and the desire to reduce overall portfolio volatility. If anything, it would seem that in the aftermath of recent market turbulence, there may be an even greater interest in hedge funds based on these rationales.

Needless to say, as with any investing style or approach, interest can and does wax and wane based on a variety of factors, including short-term performance trends, fiscal and monetary policies, and political pressures. Reports that star hedge fund managers with long track records, including Ray Dalio’s Bridgewater Associates, David Einhorn’s Greenlight Capital and Bill Ackman’s Pershing Square Capital, have recently stumbled after years of success may lead some to question whether it makes sense to invest (or invest more) in such funds. On the other hand, further upheavals in global stock and bond markets of the sort that we saw during 2015, especially in the wake of a potentially dramatic change in Federal Reserve policy, could strengthen individual and institutional investor resolve to seek alternative ports from what could be a choppy traditional-asset-class storm.

Michael J. Panzner is a 30-year Wall Street veteran and the author of three books, including Financial Armageddon, which predicted the 2008 global financial crisis.