Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Building your portfolio gives you complete control over which investments to include but it also opens you up to greater downside risk. After all, most people simply don’t have the time to spend every day from 9:30 am to 4 pm, New York time, monitoring their portfolios and those who do, may not be able to absorb the fees from making many different transactions.

Image via Flickr by StockMonkeys.com

{kind=link}

Building a Portfolio

In the end, the smart money ends up taking a few long positions, a couple choice short ones, and a few investments to help hedge any losses. The idea behind hedging is simple. You pick an investment that moves contradictory to the rest of your portfolio. Ideally, when one loses, the other gains. It is never that simple, but you get the concept.

When one investment is losing money, another is making some. Your returns are never as high as they could beef you had only invested in that one successful investment, but your returns also are never as bad as they could be if that investment tanks. Think of it as placing a big bet on your favorite team then placing a smaller bet on its opponent. If your team wins, you get a little less than you would have – after all, you placed a bet on the losing team – but, if your team loses, the other bet pays off, and you do not lose quite as much as you would have.

In theory, the idea is a solid one. However, finding that perfect hedge is a little more difficult.

The Perfect Hedge

Every investor and analyst has different ideas about what makes the perfect hedge. Some will advise people who invest in long stock positions to buy protective put options while others make suggestions based on the currency or commodity that would most be impacted. Take gold for example. If the price of gold goes down, gold mining shares will also go down. You could take a put option to hedge any downturn.

Using Gold to Hedge

Some hedges also follow conventional wisdom. For instance, when the economy is rocky, people tend to like gold, making it a top choice for hedging volatility in the stock market as a whole. For the most part, that works out.

Look at this chart comparing the price of SPDR Gold Shares (GLD) versus the S&P 500 over the past five years. When one goes up, the other goes down.

Using Bonds as a Hedge

Some people prefer bonds as a hedge. In fact, some asset managers advise it. However, the focus is a bit different. Instead of moving counter to equities the way gold does, bonds as a hedge serve to act as a stabilizer for your portfolio’s returns. They smooth out the high points and boost the low.

Bonds as a hedge is a traditional strategy, but bonds do not protect against equity declines as well as they used to. “We don’t find bonds to be the natural diversifier for equities anymore,” says C. Hayes Miller, head of multi-asset strategy for Barings Asset Management. “Global markets are so aligned with central bank actions, what’s negative for equities could be for negative for bonds and vice versa.” Instead, Barings Asset Management advises its clients to keep roughly one-quarter of their portfolios in short-term bonds and cash equivalents.

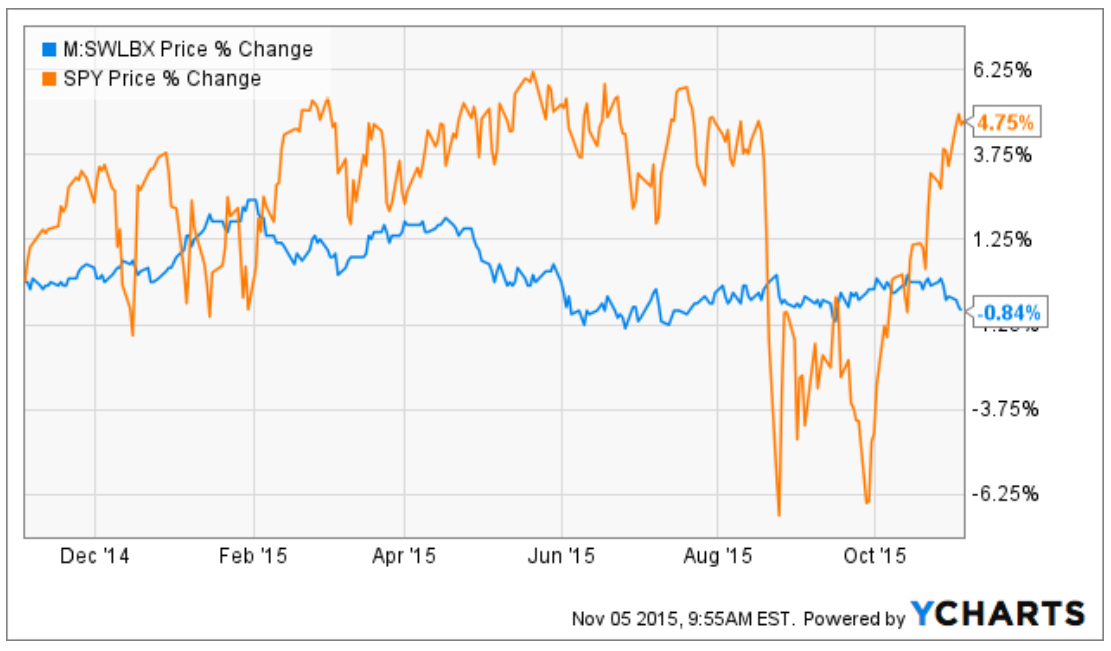

Using Schwab Total Bond Market (M:SWLBX) as a way to invest in bonds without actually purchasing any and comparing that to the SPDR S&P 500 (SPY), an ETF that mimics the S&P 500, you can see one moves counter to the other.

Which is Right for You?

The answer to that question depends on several different things. You will need to consider how investing in a certain investment as a hedge will affect your portfolio, as well as your unique tax situation. You will also have to consider the unique makeup of your portfolio and take your risk comfort level into account. Lastly, think about your overall goals.

Type of Hedging Investment

First, consider how you might invest in gold. If you are thinking to buy actual bouillon, remember that if you hold it for over a year, that investment is now classed as a “collectible” and as such is subject to a 28 percent federal long-term capital gains tax rate. Depending on your tax situation, this could really hurt your pocket. Treasuries like bonds are most advantageous, but only when you buy the actual bond.

Portfolio Holdings

Consider your portfolio holdings as well. You probably don’t have all your investments tied to the stock market as a whole. Different stocks will have different correlations with gold and bonds. Moreover, your portfolio probably consists of more than one stock. You will need to take this into account too by looking at the performance of the portfolio as a whole.

Risk Aversion

The level of risk you prefer also makes a difference. Investing in bonds nets a standard percentage as long as you do not mind holding the bond to maturity. You can always invest in a bond mutual fund, thus removing the need to wait until the bond matures, but as you can see from the graph above, its return varies over time. Gold can also be very volatile, so it takes some careful consideration.

Ultimate Goal

Your goals make a big difference too. Always remember that you have to assume some risk to get a reward. Gold has been a pretty good hedge against the S&P 500 for the past five years, but if something is hedged perfectly and you invest the same amount in each investment, your net return could be zero – like two people of the same weight on a see-saw.

The Bottom Line

More risk-averse investors may want to look into gold if their investments mirror the market as a whole while bonds are better suited to those investors who would like to reduce the volatility of their portfolio returns but are still willing to assume a fair degree of risk. In the end, the question of gold versus bonds in your portfolio will depend on several factors that differ for each investor.

Renee Ann Breiten is a freelance finance writer and former management consultant with over 15 years of experience in business management and strategy. She earned an MBA in financial management from Exeter in 2007 and has enjoyed a variety of international business experiences, working primarily in England and Australia. Breiten's work is centered on technology, consumer trends, and investing strategies. Her writing has appeared on TheStreet, Marketwatch, Insider Monkey, Seeking Alpha and Motley Fool.