Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Commodities are known for being positively linked to inflation and therefore offer protection in periods of high inflation when traditional assets perform poorly. However holding physical commodities is neither practical nor desirable. Storage and transportation costs may be high and investors usually do not have the necessary knowledge. The exception is to be made with Gold. Many investors hold physical Gold as it is considered a safe harbor of wealth. There are many ways to gain exposure to commodity returns without actually owning them. Long only strategies of physical commodities may not offer the highest returns. We are going to have a look at how to enhance commodity returns with the use of Futures.

How to gain exposure to commodity returns with futures

Until recently a common way to gain exposure to commodities, without holding them physically, was through companies that produced those commodities. Crude Oil extraction companies, Precious Metal miners and so on. But these securities come with a high exposure to Stocks. When the broad stock market underperforms these stocks are also likely to underperform. With these securities we don’t have a clear and simple exposure to commodities.

A very effective way to gain pure exposure to commodity futures is through one of the various ETFs that invest in broad baskets of commodity indices that are based on futures. So the funds basically hold long positions in the futures contracts for each commodity weighted according to the index weights. You can also gain exposure to various commodity sectors, such as Grains, Energy or Metals. Sector ETFs are extremely useful as you may have different views for each sector.

Of course you could do it yourself, but then you would continuously have to weight your futures portfolio by rebalancing accordingly. You would also have to implement contract roll overs. These funds hold the nearest contract and before expiry the fund manager rolls the positions over to the next expiring contract. This maintains the funds exposure to the commodity through the most liquid contract, which is the nearest to expiry. For a small fee you can save yourself a considerable amount of hassle and let a manger take care of it.

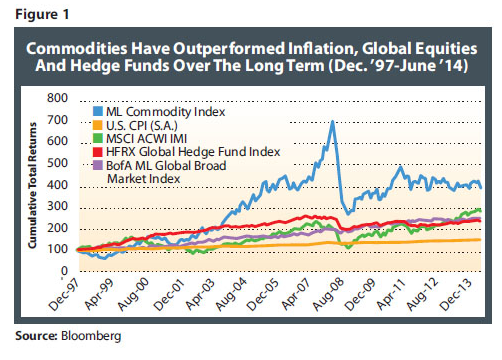

Commodities have had a negative performance for several years

The chart below shows how the Merrill Lynch Commodity index performed compared to other assets for the period from December 1997 to December2014. From inception the commodity index has outperformed Hedge Funds, Stocks, Inflation and Bonds. However we can see that commodities have not performed very well since its high in early 2010. But this has been due to a particular macro scenario that will probably not last much longer. We have seen a prolonged period of low interest rates and therefore low inflation. Commodities are positively correlated, especially in long periods of time, to inflation.

Thanks to the same reason, low interest rates, there has also been an impressive bull market in Stocks and Bonds. These two reasons have created the environment for the poor performance of commodities, and therefore commodity tracking ETFs. This may be about to change soon as we begin to transition into a higher interest rate and higher inflation regime.

What are the drivers of returns for commodity futures?

Funds that hold their commodities investments in futures generate return from 3 different sources, Spot return, Collateral return and Roll return. Spot return is the return generated buy an increase in the spot price of the futures contract of the commodities. Simply put if the fund buys Crude Oil at $45 per barrel and sells the same contract $48 per barrel the $3 of profit is the source of Spot return.

Collateral return is generated by the capital of the fund being invested in Treasury Notes. As the futures positions are fully funded, meaning if the fund has $100 million AUM the manager will buy a basket of commodity futures contracts worth a notional $100 million. The AUM are not left on a cash account and all cash will be invested in Treasury Notes, therefore creating another source of return.

The third source of return is possibly the most important, Roll return. This is the return generated when the manager sells futures contracts that are about to expire to roll them into the next futures contract. For example if the manager sells December Crude Oil at $45 to buy January Crude Oil at $42 there is a positive difference of $3. This difference creates a positive Roll yield. If for example the manger rolls December Gold by selling at $1070.00 to buy January Gold at $1075.00 then in this case the $5 represents negative Roll yield.

Second and Third Generation commodity futures indices

These indices have certain enhancements that may produce superior results, through the ETFs that track them, given the structures with which they are built. Second generation indices include the Merrill Lynch Commodity Index Extra (MLCX) and the Deutsche Bank Optimum Yield Index (DBLCI). The MLCX spreads the roll of the futures contracts over a 15 day period. It also holds the second nearest contract whilst rolling into the third nearest contract. The DBLCI picks the futures contract for each commodity with the highest implied Roll return. This index chooses amongst the contracts expiring in the next 13 months. As we saw earlier futures contracts that have positive Roll yield can generate superior returns.

The third generation of indices includes the UBS Bloomberg Constant Maturity Commodity Index (CMCI). This index invests in the same commodities as the standard UBS index. In this CMCI index however weights are decided according to analysts’ research on expectations for each contract. This index changes tenors and implements overweighting of outperforming contracts and underweighting of underperforming contracts.

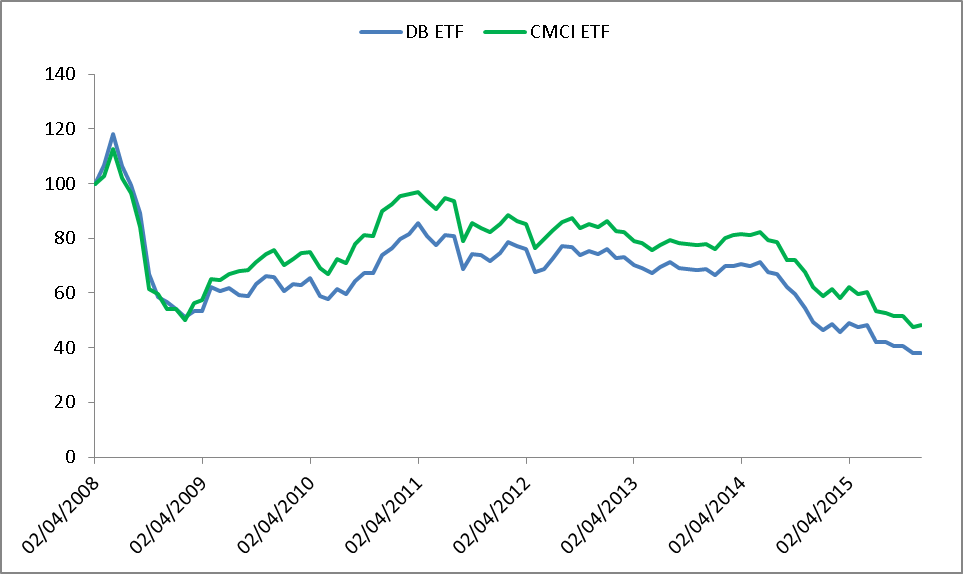

The above chart shows the cumulative growth rate for the DBC, a broad commodity index tracking ETF and UCI which is the CMCI tracking ETF. Despite the bear trend it is clearly visible how the third generation index has outperformed the standard first generation index.

Bottom line

Indifferently of which ETF you choose, whether they track commodity sectors, broad indices or second or third generation indices, you should be able to enhance returns by picking funds that invest in futures contracts. Commodities have shown to have the properties mentioned when held for longer periods of time and that should be taken into account when deciding to invest.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst