Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

October saw what looked like a reprieve from the high inflation we’ve seen this year, with the slowest increase in the consumer price index we’ve seen in nine months.[1] Of course, even though the 7.7% CPI looks good in the context of this year, it’s still not too far away from recent 40-year highs.[2]

Even still, it’s a good sign, and it seems like some of the recently spiking prices could be due to level out. But even as inflation starts to let up, there’s a belief among some that the drivers of that high inflation aren’t going anywhere soon, and that Americans should seriously consider higher inflation to be a part of their economic outlook.

Kenneth Rogoff believes that’s the case. Rogoff is an economics professor at Harvard University and senior fellow at the Council on Foreign Relations. His long and distinguished career involves time spent as the International Monetary Fund’s chief economist and service at the Federal Reserve Board of Governors. Professor Rogoff knows what he’s talking about—and what he’s talking about is less than optimistic.

In a recent article for the outstanding journal Foreign Affairs, Rogoff suggests we’ve gone into what he calls “the age of inflation.”[3] In this new era, a variety of foundational inflation drivers will thrive long after drastically high prices have subsided. One of these drivers, according to Rogoff, is a long-term embrace of fiscal and monetary assistance on a level previously unseen.

If Rogoff is right, the consequences for retirement savers could be huge. Economic volatility stemming not only from high inflation risks but also from central bank efforts to contain it has made life tough for savers this year. Americans have lost a net worth of as much as $10 trillion, in addition to other effects.[4]

If inflation above the Federal Reserve’s 2% target continues for an extended period – as Rogoff suggests will happen – it’s worth considering that the difficulties retirement savers have encountered this year will keep going, as well. And if that happens, those retirement savers might want to give some serious thought to what they can do to help reduce the impact on their hard-earned nest eggs.

We’ll talk more about that later. First, though, let’s spend a few minutes taking a closer look at what Ken Rogoff had to say in Foreign Affairs as he made a case that we now are living in an “age of inflation.”

Governments and Banks Underplayed Risks of Expansionary Policy, Says Rogoff

Fiscal and monetary policy aren’t the only villains of Rogoff’s 5,000-word article, for the record. According to Rogoff, the worldwide move away from globalization and a large-scale move to green energy have also played a large part.[5]

For this article, however, we’re going to focus on what Rogoff has to say about how expansionary fiscal and monetary policies have the potential to drive inflation. Rogoff is the one who succinctly told all of us previously that “since the invention of money, pressure to finance government debt and deficits, directly or indirectly, has been the single most important driver of inflation.”[6]

On that note, Rogoff in his Foreign Affairs piece puts a big part of the blame for current high inflation on generous governments and central banks scrambling to keep their economies – and citizens – buoyant during the heights of the pandemic:

Fearing a pandemic-driven recession, governments and central banks were instead preoccupied with jump-starting their economies; they discounted the inflationary risks posed by combining large-scale spending programs with sustained ultralow interest rates.[7]

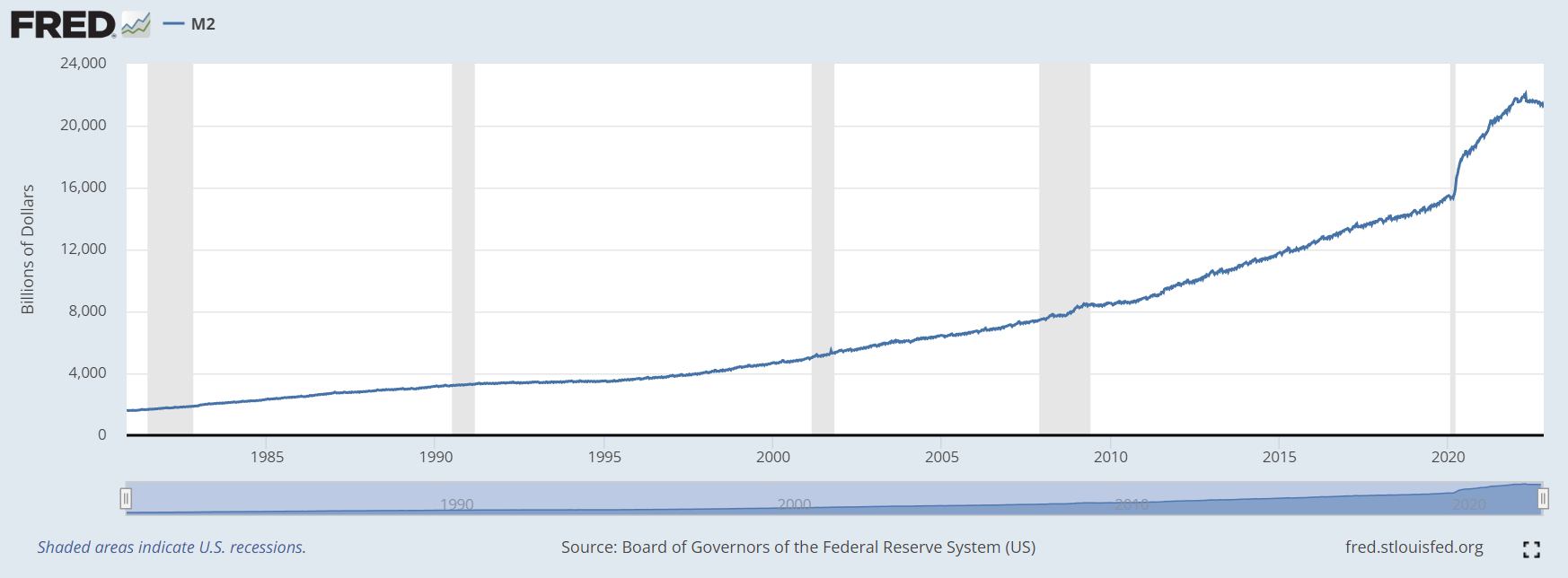

Rogoff believes – as most seem to – that near-term drivers of what has become drastically high inflation will lose steam soon. America’s entire M2 money supply rose by a stunning 41% between early 2020 and mid-2022 as fiscal and monetary policy worked together to keep the economy functional during the most difficult days of the pandemic.[8] As the money supply now (slowly) decreases, the biggest inflation numbers also should recede.[9]

Source: St. Louis Fed

So what makes this the age of inflation – as Rogoff calls it – if high inflation is expected to fall? While inflation is expected to descend from its loftiest heights, price pressures may continue to press on, thanks to factors he thinks are likely to show themselves again and again.

One such factor is ongoing expansionary fiscal and monetary policy. Rogoff says when governments and central banks add money to the system during times of crisis, they’re not always so good at stopping the influx when the crisis has passed. Stimulus is often well received for its short-term benefits, and the long-term consequences are left for someone else to handle:

Inevitably, stimulus spending is political, and those who promote large rescue packages are often also motivated by the opportunity to expand social programs whose approval in Congress might in ordinary times be impossible [emphasis added]. This is one reason why there tends to be far less talk about reducing stimulus once a crisis is over.[10]

Case in point:

Just three months later [following passage of President Trump’s COVID-19 relief package], although the economy was continuing to recover, Democrats under Biden passed a new $1.9 trillion stimulus package, with a number of prominent economists, including New York Times columnist and Nobel laureate Paul Krugman, cheering them on. Krugman and others argued that the package would enhance the recovery and provide insurance against another wave of the pandemic and that it carried minimal risks of igniting inflation.[11]

In other words, Rogoff is saying that crises can be great opportunities for governments to make what amounts to permanent expansions to the social safety net. Those efforts, in turn, help to perpetuate fiscal and monetary policies that can have a dramatic impact on inflation.

Pandemic Spending Holds Origins of Build Back Better and Inflation Reduction Acts

The Build Back Better Act, the $3.5 trillion bill that eventually turned into the Inflation Reduction Act and passed into law, was a massively expansive bill that Johnathan Weisman, reporter for the New York Times called “the most significant expansion of the nation’s safety net since the war on poverty in the 1960s”. Weisman also claimed the bill “would touch virtually every American’s life, from conception to aged infirmity.”[12] [13]

Weisman had more to say about how the bill got as far as it did:

The pandemic loosened the reins on federal spending, prompting members of both parties to support showering the economy with aid. It also uncorked decades-old policy desires — like expanding Medicare coverage or paid family and medical leave — that Democrats contend have proved to be necessities as the country has lived through the coronavirus crisis.[14]

The bill in its original form didn’t become law. And when it was eventually passed in the form of the Inflation Reduction Act, it was a $740 billion piece of legislation – not $3.5 trillion.[15]

But Professor Rogoff’s point is that crises tend to justify spending sprees and ultra-easy monetary policies. These times of fiscal and monetary excess can be perpetuated by opportunistic politicians in the name of expanding the social safety net. If that continues, it could become a fundamental driver of inflation effectively embedded in the nation’s economic fabric.

Ken Rogoff suggests we’re in store for a continuing stream of global economic shocks, noting, “Today, large-scale global shocks such as war, pandemic, and drought seem to be coming one after another or even at the same time.”[16]

The chance that we’ll see such ongoing volatility, together with the apparently greater tendency for governments and central banks to help alleviate the resulting impacts to citizens, could help perpetuate the era of higher inflation about which Rogoff speaks. And as Rogoff says, as those “reasonable” justifications for outsized fiscal and monetary assistance continue, so, too, will the efforts to morph those supposedly shorter-term “helps” into something more permanent.

Preparing for the “Age of Inflation”

But what does this so-called “age of inflation” mean to retirement savers?

To start with, whether or not persistently higher inflation is something that continues, retirement savers will still want to take action to give themselves the best possible chance at retaining the value of their savings. It is, of course, impossible to predict the future, but it’s important to prepare for the possibility that that value could take a significant hit. Since April 2021, when inflation first jumped well above the Federal Reserve’s 2% target, the headline consumer price index has averaged 7%.[17] That means in just the last 19 months, a retirement savings account valued on paper at $500,000 has lost more than $50,000 in purchasing power.[18]

There’s no need to absorb those risks without making an effort to hedge against them, given the ease with which some inflation-fighting measures can be taken. One of the most time-honored and universally respected of those measures is the addition of physical assets viewed as safe havens and stores of value. Precious metals – including gold and silver – are great examples of these assets.

Are precious metals appropriate components of your inflation-fighting strategy? I can’t tell you that—you’ll have to evaluate it for yourself. But I encourage you to give a little thought to doing something that could reduce the impact to your savings of potential chronic inflation or even possible recession.[19]

Now is a good time to consider obtaining assets that have the potential to help you retain the value of your savings, but that doesn’t mean there’s ever a bad time to think long and hard about what could have an impact on your savings. To get started, I recommend checking out Sophisticated Investor‘s list of the top precious metals companies in America. If this inflation really is here to stay, doing your due diligence to find the assets that are best for your retirement strategy could provide you and your family with peace of mind in the years to come.

Works Cited

[1] Bureau of Labor Statistics, “Consumer Price Index Archived News Releases” (accessed 12/8/22).

[2] Ibid.

[3] Kenneth Rogoff, Foreign Affairs, “The Age of Inflation” (November/December 2022, accessed 12/8/22).

[4] Robert Frank, CNBC.com, “Stock market losses wipe out $9 trillion from Americans’ wealth” (September 27, 2022, accessed 12/8/22).

[5] Rogoff, “The Age of Inflation.”

[6] Kenneth Rogoff, IMF.org, “Globalization and Global Disinflation” (August 29, 2003, accessed 12/8/22).

[7] Rogoff, “The Age of Inflation.”

[8] John Greenwood and Steve H. Hanke, Wall Street Journal, “The Fed Ignored the Money Supply, and a Recession Is Coming” (July 7, 2022, accessed 12/8/22).

[9] Federal Reserve Bank of St. Louis, “M2” (accessed 12/8/22).

[10] Rogoff, “The Age of Inflation.”

[11] Ibid.

[12] Li Zhou, Vox.com, “How Democrats plan to overhaul taxes, climate spending, and health care before the midterms” (July 28, 2022, accessed 12/8/22).

[13] Jonathan Weisman, New York Times, “From Cradle to Grave, Democrats Move to Expand Social Safety Net” (November 1, 2021, accessed 12/8/22).

[14] Ibid.

[15] Shawna Chen, Axios.com, “Biden signs Democrats’ $740 billion tax, climate and health care bill into law” (August 16, 2022, accessed 12/8/22).

[16] Rogoff, “The Age of Inflation.”

[17] U.S. Inflation Calculator, “Historical Inflation Rates: 1914-2022” (accessed 12/8/22).

[18] Buyupside.com, “Inflation Calculator” (accessed 12/8/22).

[19] Niloofer Shaikh, Seeking Alpha, “98% of CEOs predict recession in 2023 – Conference Board” (December 7, 2022, accessed 12/8/22).

Devlyn is director of education, the on-staff economic analyst at Augusta Precious Metals, and a member of the Harvard Business School's business analytics program. Over three decades, he has processed more than $2 billion in financial assets and now uses his experience to guide American retirement savers to diversify, hedge against inflation, and protect their retirement savings through gold IRAs.