Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Concerns over global economic growth, market volatility, not to mention whisperings of a pending recession, have all made the prospect of guaranteed returns very appealing. A fixed annuity is a type of annuity contract with a life insurance company. The investor puts in a lump sum in exchange for a fixed rate of return for a set number of years. It is a tax-deferred savings vehicle, which grows based on a fixed interest similar to a CD (certificate of deposit). When earnings are withdrawn, they are taxed as regular income determined by the owner’s tax bracket.

A fixed annuity is also referred to as a Multi-Year Guaranteed Annuity (MYGA), or a fixed deferred annuity. They offer higher rates for longer terms (typically between 3 to 10 years). During the present term of the vehicle, fixed annuities offer one withdrawal a year up to 10% of the total value. Any withdrawals made before the owner is age 59 ½, are subject to an IRS penalty. At the end of the term, the owner is free to withdraw out all money, renew the for another term, or convert the fixed annuity into an immediate annuity to generate lifetime guaranteed income.

Akin to any investment, there are likewise disadvantages to fixed annuities. Money locked into a set period of time with an insurance company, during which, the investors have limited access at best. Additionally, annuities can come wit exorbitantly high fees that can whittle away at the returns.

Fixed Annuities do not come with FDIC (Federal Deposit Insurance Corporation) insurance, and instead, the capital invested is guaranteed by the financial strength of the life insurance company. Therefore, it is crucial for investors to choose life insurance companies with an A- or higher rating, based upon respective financial strength. If an insurance company files for bankruptcy or faces litigation in some capacity, investors run the risk of being unable to recover the principal invested.

Before investing, it is essential to do your due diligence, research the drawbacks of fixed annuities and the MYGA (the multi-year guaranteed annuity), and consult a financial professional before locking yourself into a contract.

Below are some of the best fixed annuities rates for 3-year and 5-year terms, based on a company rating of A- or higher as of September 2019. A description of the respective product is also provided.

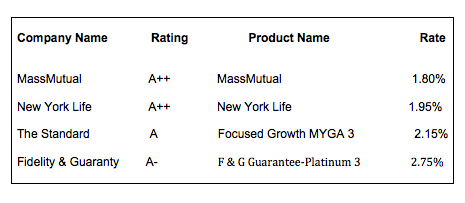

Fixed Annuities 3-Year Term

MassMutual – MassMutual Stable Voyage

Investors who decide on the MassMutual Stable Voyage can choose an initial guarantee period of three, four, five, seven or nine years. Generally, the longer the guarantee period, the higher the interest rate will be.

There are 2 different rate bands: $10,000 – $99,999 and $100,000 – $1,500,000. Investment amounts in higher bands receive higher rates.

The minimum purchase payment limit is $250. After partial withdrawals, the minimum contract value of $7,500 is required.

Most contracts offer a free withdrawal amount each year during the accumulation phase. Although this amount is not subject to surrender charges, liquidated earnings are subject to income tax. Amounts withdrawn in excess of the free withdrawal amount are typically subject to surrender charges. Withdrawals, if made prior to age 59½, may be subject to an additional 10% federal income tax.

The free withdrawal amount is calculated as follows: Contract years two and later – up to 10% of the contract value calculated as of the last business day of the previous contract year. RMD: Qualifying RMD amounts for an IRA or a qualified plan that exceed the free withdrawal amount are not subject to surrender charges. Unused free withdrawal amounts: Cannot be accumulated from year to year

There are age limits on this product from 18 – 85 years old.

New York Life – 3 Years Secure Term MVA Fixed Annuities II

With the 3 Years Secure term MVA Fixed Annuities II, there is a minimum initial premium is $5,000. Premiums of $1 million or more require NYLIAC approval.

The initial interest rate will be determined by the amount of your premium payment, when it is received, and the initial interest rate guarantee period selected. Investors have a choice of a three-, four-, five-, six-, or seven-year initial interest rate guarantee period, which corresponds to a matching surrender charge schedule. At the end of the initial interest rate guarantee period, the policy will receive a new renewal rate each anniversary that is based on the accumulation value. That rate will not be less than the guaranteed minimum interest rate (GMIR) stated in your policy. The GMIR is generally set on January 1 and July 1 for the next six months. All policies issued during that period will receive the GMIR in effect at the time of issue. The minimum GMIR is 0.05%, and the maximum is 5%.

The Living Needs Benefit/Unemployment Rider is automatically added to the policy with no additional fee. If the investor needs immediate access to the money in the policy, this rider may give some flexibility in accessing it, assuming you meet one of the following qualifying events.

Minimum withdrawal amount is $100. Surrender charges and a Market Value Adjustment (MVA) may apply. The policy accumulation value may not fall below $2,000 due to a partial withdrawal. Each policy year, the investor may withdraw the greatest of: 10% of the accumulation value as of the last policy anniversary, or, 10% of the current accumulation value, or 100% of the gain earned in the policy (for policies with a premium amount of $100,000 or more. Not available in New York.).

Withdrawals over the free withdrawal amount are subject to surrender charges, based on the surrender charge period the investor selects.

The Standard – Focused Growth MYGA 3

With a Focused Growth MYGA 3, the investor may choose a 3-year initial interest rate guarantee period and receive the rate in effect at the time they buy the annuity for the entire length of the guarantee period. Interest is calculated and credited daily. At the end of the term, they may withdraw their money or automatically start a new guaranteed-rate period. Surrender-charge periods match the rate guarantee periods. For example, if the investor selected a Focused Growth Annuity 3, all subsequent guarantee periods will be 3 years.

3-Year Rate Guarantee Periods, 3-Year Market Value Adjustment Periods

3-Year Surrender-Charge Periods (9.4%, 8.5%, 7.5%)

Additional premium accepted in first 90 days

FGA 3 issues to age 93 (The purchase of the annuity for those age 91-93 must be for transfer-of-wealth or estate-planning purposes.)

$15,000 to $1,000,000 initial premium (greater amounts may be possible if pre-approved before submitting an application).

Surrender-Charge-Free (and MVA-Free) Withdrawal Options: First 30 days of each subsequent surrender charge period, regularly scheduled payments of interest earnings, death benefits, Annuitization.

F & G Guarantee-Platinum 3

The principal grows steadily at the fixed rate of interest F&G guarantees at the outset of each 3-year period. Interest is credited daily. The interest earned may always be withdrawn without incurring withdrawal charges. At the end of the 3-year guarantee period, the investor may withdraw up to the full account value during a 30-day window.

If nursing home care is required, or in the event of terminal illness, the investor may access the account with no withdrawal charges. The diagnosis of terminal illness, or the beginning of nursing home care, must occur at least one year after the contract is issued. These are defined conditions, and this benefit may vary from state to state.

Withdrawals of principal are subject to a withdrawal charge, in the form of a surrender charge and Market Value Adjustment (MVA). The surrender charge in contract year one is 9% of the withdrawal. This percentage decreases annually through the end of each guarantee period.

Any time a withdrawal incurs a surrender charge, an MVA will be made. The MVA is based on a formula that takes into account changes in the U.S. Treasury yields since the contract was issued. Generally, if treasury yields have risen, the MVA will decrease the surrender value; if they have fallen, the MVA will increase the surrender value. The MVA may be subject to a ceiling in PA.

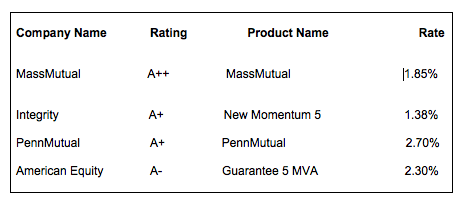

Fixed Annuities 5-Year Term

MassMutual – MassMutual Stable Voyage

Investors can choose an initial guarantee period of five years. Generally, the longer the guarantee period, the higher the interest rate will be. This product has age limits from 18 – 85 years old

There are 2 different rate bands: $10,000 – $99,999 and $100,000 – $1,500,000. Investment amounts in higher bands receive higher rates.

The minimum purchase payment limit is $250. After partial withdrawals, minimum contract value of $7,500 is required.

The free withdrawal amount is calculated as follows: Contract years two and later – up to 10% of the contract value calculated as of the last business day of the previous contract year. RMD: Qualifying RMD amounts for an IRA or a qualified plan that exceed the free withdrawal amount are not subject to surrender charges. Unused free withdrawal amounts: Cannot be accumulated from year to year

Integrity – New Momentum 5

New Momentum is a flexible premium deferred annuity (FPDA) that combines the power of tax deferral with a choice of guaranteed rate options (GROs), as well as a quarterly interest option (QIO) providing a rising rate opportunity. The principal may be allocated to one or more of the multiple initial GROs, all with an initial first-year rate enhancement, or to the QIO until moved.

At the end of the guarantee period, investors may transfer to existing GROs or remain in the QIO at a then-current interest rate. And at the end of a GRO period, transfer to a different guaranteed rate option without a withdrawal charge or transfer fee. New Momentum also offers flexible annual withdrawal privileges.

Choose scheduled payments guaranteed to continue for a lifetime, with a 10-year period certain (single or joint). Other options may be available. Income payment guarantees are backed by the claims-paying ability of Integrity or National Integrity.

PennMutual – Guaranteed Foundation Fixed Annuity

Guaranteed Foundation Fixed Annuity is a single-payment retirement vehicle available for qualified plans (funded with pre-tax dollars) and non-qualified money (funded with after-tax funds), for single or joint owners, from ages 0 – 85. Guaranteed Foundation Fixed Annuities are available for a variety of guarantee periods. The guarantee period chosen will determine: the guaranteed, fixed interest rate; The number of years which are guaranteed growth at that interest rate; When the investor will have full access to the contract value without incurring a surrender charge.

There are 2 different rate groups: $10,000 to $99,999, and $100,000 to $2,000,000. Investments n higher rate groups receive higher rates.

A Guaranteed Foundation Fixed Annuity offers tax-deferred growth. Interest is credited daily so there is no uncertainty about what you will earn. The fixed interest rate for your initial guarantee period will be declared at the time your annuity is issued. This interest rate will vary based on the guarantee period you select and the amount of your purchase payment. Interest rates for renewal guarantee periods will be determined based on the length of the selected (or default) guarantee period and the contract value as of the renewal contract anniversary. A Minimum Guaranteed Interest Rate (MGIR), ranging from 1% to 3%, is set at issue and guaranteed for the life of the contract. All declared interest rates, both initial and renewal, will be greater than or equal to the MGIR rate.

American Equity – Guarantee 5 MVA

American Equity allows the accumulation of interest based on a fixed interest rate determined at the beginning of the contract. A traditional fixed annuity includes:

Guaranteed Rate – A competitive rate is declared at the beginning, and guaranteed for a set period of time.

Liquidity Flexibility – Increased access options for healthcare-related expenses available with optional Rider.

Lifetime Income Options – Convert retirement funds into a stream of guaranteed, lifelong payments.

Within 30 calendar days after the end of the 5-year guarantee period chosen, investors may choose to apply a Contract Value to a settlement option, take a partial withdrawal and apply to another guarantee period, surrender the contract without surrender charges, or renew the contract for another guarantee period.

This long-term retirement product is purchased with an insurance provider that, in turn, guarantees principal protection, tax-deferred growth on assets and a reliable income stream. Throughout the course of the contract, the fixed annuity earns interest based on an established rate.

American Equity offers Traditional Fixed Annuity products that provide different benefits and terms.

Conclusion

This is a sampling of the fixed annuities products that are available to investors. To reiterate, it is highly advisable to research annuities and consult a financial professional before making investment decisions. Always do your due diligence, and keep your money and investments safe.

Sarah Bauder is a financial writer with over a decade of experience at numerous online publications, writing about alternative investments, retirement, US politics, world economy and more.