Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

An employer-matched 401(k) is an excellent retirement savings vehicle. As a tax-advantaged account, 401(k) plans let your money grow tax-free while also lowering your upfront income tax burden. Unlike a regular savings account, you won’t have to pay taxes on the savings in your 401(k) until you make your first withdrawal in retirement.

Employers often match employee 401(k) contributions up to a certain dollar amount, or up to a predetermined percentage of one’s gross income. The most common employer match is 50 cents on the dollar of up to 6% of the employee’s pay. In 2019, 80% of American employers offered this 401(k) match to their employees within one year of service with the company.

But what happens if you lose your job? Without an employer to administer the account, it’s up to you, the account holder, to decide what happens to your retirement savings. In this article, I’ll go over what your options are in the event of a 401(k) plan termination.

What Happens to Your 401(k) When You Lose Your Job

I’m often asked, “What happens to your 401(k) when you leave a job?” The short answer is that neither you nor your employer will be able to make contributions to the plan. However, the account remains yours. You can still check your balance, adjust your portfolio, make an early withdrawal (with applicable penalties), or rollover your account.

Unfortunately, any company match that required vesting will not be kept if the money has not matured by the date you leave the company. Additionally, about 36.5% of employers cover all or some of their employee’s administrative fees for their 401(k). If your employer was covering these annual fees (usually valued between 0.04 and 0.5% of all assets in the account), you’re going to be on the hook for them once you’re let go.

The upside is that whatever funds are available in your 401(k) the day you’re let go will remain available to you indefinitely.

Option 1: Rollover Your Money Into An IRA

In most cases, rolling over your account balance to a self-directed individual retirement account (IRA) is your best bet. This way, you can skip out on the fees associated with actively-managed IRAs and can exercise complete discretion over the asset classes in which you invest.

You can open an IRA with any brokerage and can invest in a variety of traditional and alternative assets such as stocks and bonds, exchange-traded funds, mutual funds, index funds, precious metals, cryptocurrencies, and more. Opening a precious metals IRA is one of the best ways to diversify your retirement savings and insulate your portfolio against volatility during an economic downturn.

Moving your retirement savings into a self-directed IRA usually comes at no upfront cost and lets you continue to enjoy the tax-deferment benefits of your old 401(k). Readers should note that IRS rules permit only one 401(k)-to-IRA rollover per 12 month period, and every rollover must be completed within 60 days of the date that you receive your 401(k) distribution.

Note: If a financial institution is writing a check to facilitate your distribution, ensure that the check contains your new IRA account number. This requirement varies by IRA provider, so you might want to check with your financial institution to avoid unnecessary complications or delays.

Option 2: Rollover Your Money Into A New 401(k)

In the event of a 401(k) termination from your previous employer, you can simply roll over your existing account balance to one administered and matched by a new employer. Obviously, this option is only on the table for those who’ve already found employment with a new company that offers 401(k) matching.

It’s worth noting that a plan-to-plan rollover isn’t subject to the same limitations as a 401(k)-to-IRA rollover. Currently, there are no restrictions on the number of plan-to-plan rollovers that can be completed within a 12-month period.

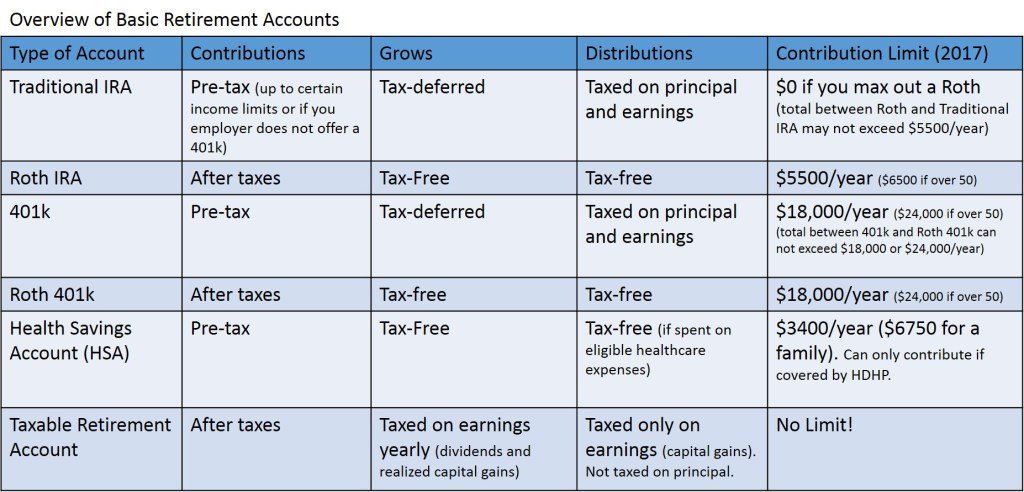

The chart below demonstrates the key differences between 401(k) plans and IRAs (Roth and Traditional) as well as other retirement savings accounts. The primary differences lie in the annual contribution limits (IRAs, in most cases, cannot exceed $5,500 yearly) and whether contributions are tax-free or merely tax-deferred. Whether you decide to roll over your balance to a 401(k) or IRA will depend on your employment status, number of years from retirement, income level, and risk tolerance.

Source: KevinMD

Option 3: Withdraw Your 401(k) Funds Early

This is the “nuclear option” that should only be considered if you’re over the age of 59.5, the age at which you become exempt from the IRS early withdrawal penalty. One of the foundational rules of investing is that the time value of money should always work in your favor. Once you pull money out of the market, the function of time stops working to your benefit—in fact, inflation will diminish the value of your dollar every year (on average, by about 3.22% annually).

Any withdrawal from your 401(k) plan initiated while you’re under the age of 59.5 will stipulate a 10% penalty on the withdrawn amount. For this reason, early withdrawals should only be seriously considered as a last resort to cover emergency expenses.

Note: Under the Coronavirus Aid, Relief, and Economic Security (CARES) Act, 401(k) account holders may qualify for a penalty-free withdrawal depending on one’s plan requirements and provided that they acquire appropriate documentation.

The Bottom Line

When you’ve lost your job, you have three options for your retirement savings: Renew, rollover, or withdraw. The wrong choice can end up costing you.

Whatever you do, don’t panic and pull money out of your 401(k) when you lose your job. Cashing out early—that is, before the age of 59.5—will trigger a 10% early withdrawal penalty payable to the IRS when you file your tax return.

Plus, the IRS automatically withholds 20% of early 401(k) withdrawals for taxes, which means you may only receive $40,000 of a $50,000 early withdrawal before applicable penalties. However, you may get the withheld portion back in the form of a tax refund if the withheld amount is greater than your tax liability.

It’s also worth noting that early 401(k) withdrawals effectively cement any losses you may have incurred in your investments. If you pull from your 401(k) while markets are down, you lose out on future gains to your portfolio when the market eventually rallies.

Resist the temptation to withdraw early. Instead, respond to a 401(k) plan termination by rolling over your balance to a self-directed IRA or into a new employer-matched retirement account. This way, you’ll avoid penalties and allow your money to grow tax-free for a longer period of time.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.