Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

#1 How will my portfolio fare in a crisis

This is a question every investor should have on his mind. What happens to my portfolio if there is a Stock market crash? Or what would happen if interest rates go up sharply? A good balance and a well-diversified portfolio can help off-set some of the damage done in times of crises or periods of high inflation. When these periods hit we tend to panic when the market gets close to the bottom. That’s when money that was not smart enough to get out earlier liquidates positions and those that where hedged or had exited their positions sooner get back in.

Some of the systematic risks involved with the markets are impossible to avoid. We saw that in the last great crisis of 2008, when previous correlations fell apart and most asset classes where hard hit.

But there are some asset classes that do better than others in these particular times of crisis and that may be due to their lack of correlation through liquidity needs. Other reasons are their reliance on strategy implementation to create returns and an inelastic demand curve.

Which assets may protect against downside and inflation

Infrastructure has a very inelastic demand curve, as they offer high necessity goods or services. These assets tend to operate in a monopolistic market, or at least have very little competition. These factors mean that income streams are very stable and reliable. They are usually positively correlated to inflation as prices are often linked to an inflation index. Investors typically have low liquidity needs and these assets do not tend to change hands often, this creates little volatility in their price.

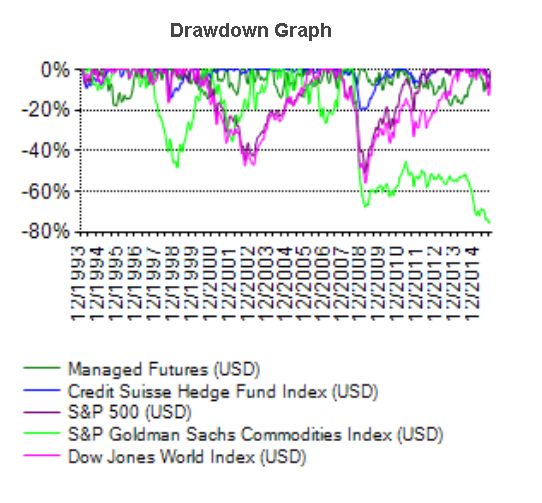

Managed Futures is a Hedge fund style that is highly uncorrelated to Stocks and Bonds. Hedgeindex shows the correlation of their Managed Futures index to S&P 500 is – 0.07. They also manage to maintain that low correlation through crises. This is due to the fact that Managed Futures do not generate any of their return from simply holding an asset class. Their returns have high a component of Alpha as it can only be attributed to the implementation of a strategy and therefore they are not likely to suffer break downs of low correlation when a crisis hits.

The chart below shows how Managed Futures suffered much smaller losses during both the 2001 Tech bubble and the 2008 crisis than the S&P 500. The maximum drawdown for the Managed Futures index from 1994 does not reach -20% compared to a nearly -60% drawdown for the S&P 500.

#2 Am I short of liquidity

Liquidity may be a bigger cause for concern than many investors think. Before constructing your portfolio and allocating funds to various assets you need to be aware of what your liquidity needs may be going forward.

Considering your liquidity needs is especially important when you are considering alternative investments. These investments are often very illiquid, that is they are hard to get out of or sell in a secondary market.

This also gives rise to the possibility that they offer a liquidity premium, in that their performance will reward holders of these assets for the fact that they have little liquidity. You can see then that low liquidity may be a good thing if it allows you to harness superior returns. The problem however may arise if or when you need extra liquidity. Holding extra cash also allows you to seize the opportunity of a great investment when it comes along.

Liquidity has to be thought of as simply the amount of cash you have in your bank account. Stock, Bonds and Long only funds are considered as having a high level of liquidity, as they can be converted to cash usually within days. But you may be in the middle of a market correction when all of a sudden you need cash and your bank account does not have enough money. Now you may be looking at picking up a 5% or 10% loss on the amount of assets you sell to gain the liquidity you require.

Hedge Funds and Private Equity funds usually have lock-up periods which pose big restrictions on withdrawing your cash early. They also have withdrawal windows usually every quarter with a one month notice. Private Equity funds have even stricter restrictions as the capital you commit to the fund may not be accessible at all for the first years. When you can access these funds they will usually be sold below Net Asset Value of the fund. There are various reasons, but mainly it is due to a lack of buyers in the secondary market and the lack of transparency of these funds’ accounts.

Careful thought, planning of your needs and the size of your portfolio need to be considered to determine how much capital should be kept in cash. Generally speaking the larger the size of a portfolio the smaller your cash allocation may need to be.

#3 What are the Return Sources of my portfolio

It is necessary to understand the sources of return of the investments we make. It will allow us to analyze more efficiently the performance of an asset compared to its peers. In the case we have invested in an actively managed fund it will allow us to analyze if the manager has the skills he claims to have. In other words is he/she worth the fees charged.

To do this it is necessary to split return into two components or sources. Beta, is the source of return for holding an asset, it is the reward you gain for holding the systematic risk of the broader market. A long only fund of S&P 500 would only be expected to return a similar rate to the broad index. That is to say it would be expected to have a Beta of 1 and its returns should closely match those of the index. If a manager is capable of outperforming his peer group or broader market then he is considered to have Alpha. This is the capacity of the manager to produce return that is above the return for simply holding an asset.

When measuring return compared to a peer group, or benchmark, we are looking at Beta return. This is the return from simply holding the asset when compared to the general market. For example a Long/Short Hedge Fund may be compared to a general stock index like the S&P 500. In theory this type of strategy has less exposure to the systematic risk of the general stock market. As the strategy’s name suggests it is also short of stock, which reduces its overall exposure to systematic risk.

But these managers still invest in assets that underlay the S&P 500 index, and have a high correlation to that index. Hedgeindex shows the correlation between the sub index of Long/Short Hedge Funds and S&P 500 is 0.67 Which is quite high. You would then take the fund manager’s return and associate 67% of the S&P return to Beta as a source of return in the fund manager’s performance.

Let’s say the S&P 500 had a return of 10% and your fund manager a return of 11%. The manager’s performance was clearly better than the general market, but by how much? To calculate this manager’s Alpha you need to multiply the S&P 500 return by the manager’s Beta and subtract it from the manager’s return.

This would give you 11%-6.7%, so the managers Alpha, or his skill, was the source of 4.3% of his returns.

Now you are going to have a better idea as to how much your manager’s services are really worth. When differentiating between Beta and Apha as sources of return you can gain a better understanding as to what the manager’s performance really is like.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst