Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Timberland and its origin as an asset class

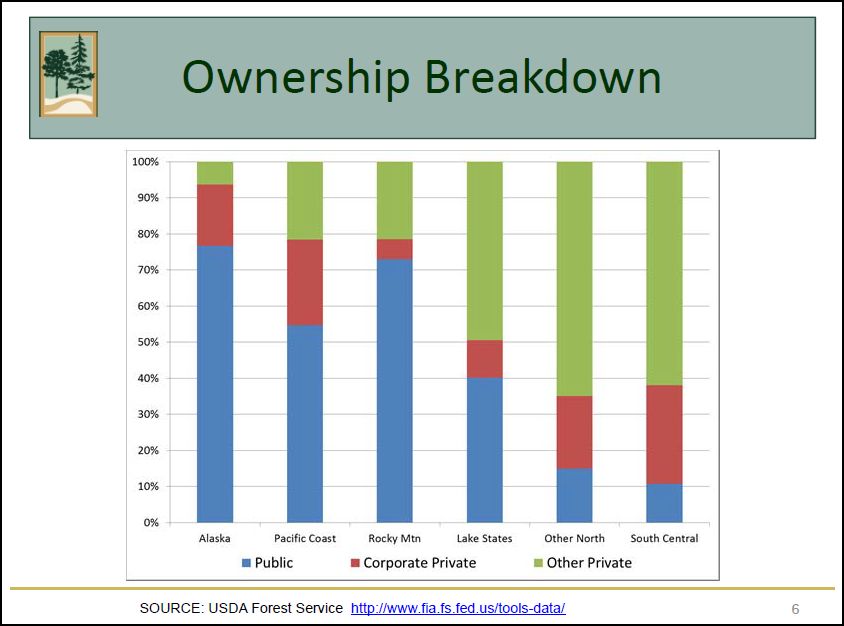

Timberland is the ownership of forests for the long-term harvesting of wood as an investment. Forests are owned by either public or private entities, public refers to government ownership and private refers to ownership by individuals, funds, endowments or other institutions.

Around 87% of the world’s 9.9 billion acres of forest land is owned by governments, the percentage of public ownership is even higher in Europe, Asia and Africa where 90%, 94% and 100% of forest land is publicly owned. The situation changes considerably in the USA where 65% of forest land is in private hands of one type or another, the percentage is even higher in the southern states where private ownership increases to 88%.

Until around 30.years ago Timberland investments were part of an integrated forest industry. Corporations owned the forest land, transportation companies and the saw and pulp mills. The surge in leveraged buyouts in the 70s and 80s saw these corporations being acquired to break them up and sell each part of the industry separately for a substantial profit. Much like the character played by Richard Gere in the well known 90s film. One notorious real life example was the purchase of Crown Zellerbach in 1985 which was then broken up and the units sold separately.

Another reason for the change of Timberland to an asset class was the rise of Timberland Investment Management Organizations (TIMOs) These organizations provide all the necessary management and services needed that helped in the transition of ownership of Timberland from industry corporations to endowments, pension plans or insurance companies which lack the necessary know how and expertise to manage these investments.

Access to Timberland

Recently there has also been a rise in REITs holding Timberland, in 1999 an IRS ruling allowed for these Trusts to hold Timberland. The major ones are Plum Creek, Weyerhaeuser and Rayonier with ownership of 16.4 million acres amongst the three and a market capitalization of $31.2 billion. These Trusts are publicly quoted allowing for enhanced liquidity whilst still being able to gain exposure to a very illiquid asset such as Timberland.

Correlation of Timberland with Traditional assets

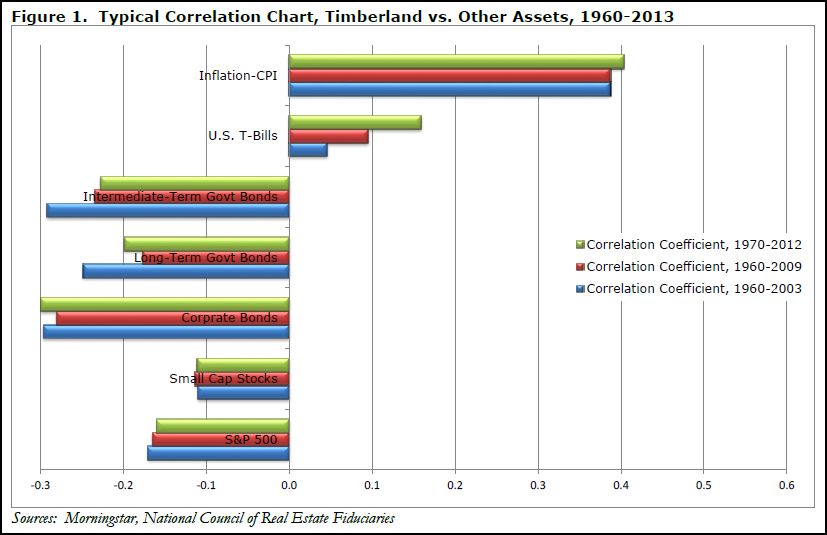

Timberland has proven to have a great potential as an inflation hedge with a high correlation to the Consumer Price Index. The chart below shows the correlation coefficient for Timberland from 1970 to 2012 as being 0.4 which is relatively high. The length of the period the correlation was tested for gives more importance to this statistical measure. It is presumable that Timber investments will perform well through periods of high inflation, which we know from experience is not the case for long term Bonds or Stocks.

We can also see from the above chart that It may also have a strong potential as a risk diversifier within a portfolio of traditional assets, with negative correlations amongst most asset classes. However there may also be evidence that Timberland is simply not correlated at all to other assets. In either case, with negative or no correlation Timberland would make for a potentially strong diversifier of risk.

Farmland

Farmland is a real asset like Real Estate but its cash flow is more linked to commodity prices rather than rent prices as the land produces crops like Corn or Grains, therefore the market price for Farmland is linked more to commodities. Usually the investor in Farmland does not actively manage the land, in most cases the land will be leased to a farmer, a cooperative or agricultural corporation. Farmland pays rent throughout the calendar year despite incomes being generated within a small window at harvest.

When contrasted with Timberland, Farmland allows for a harvest every year generating a steady income, however Timberland may take several years to harvest. A Timberland investor however has the benefit of being able to choose when to harvest. If wood prices are too low the timber may be kept on the stump until more favourable market conditions, of course with Farmland you are obligated to reap the harvest when it is due at prevailing market prices.Farmland having a short growth cycle allows for the possibility of multi-purpose usage, if a crop is deemed to have better value in the next years then land may be designated to growing that crop rather than another type of crop.

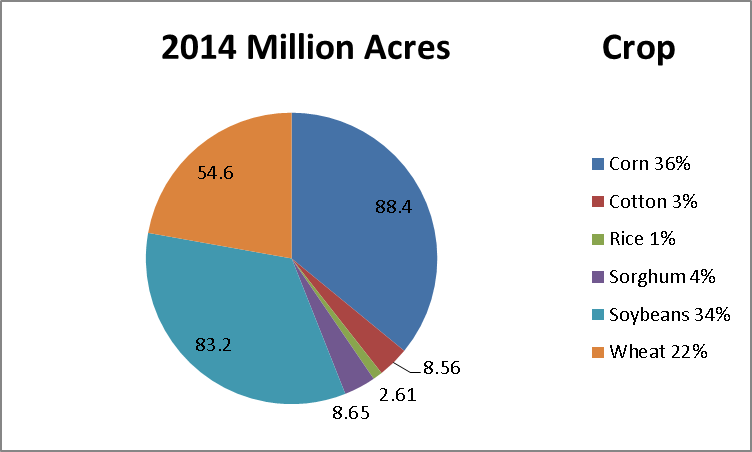

Data from National Agricultural Statistics Service

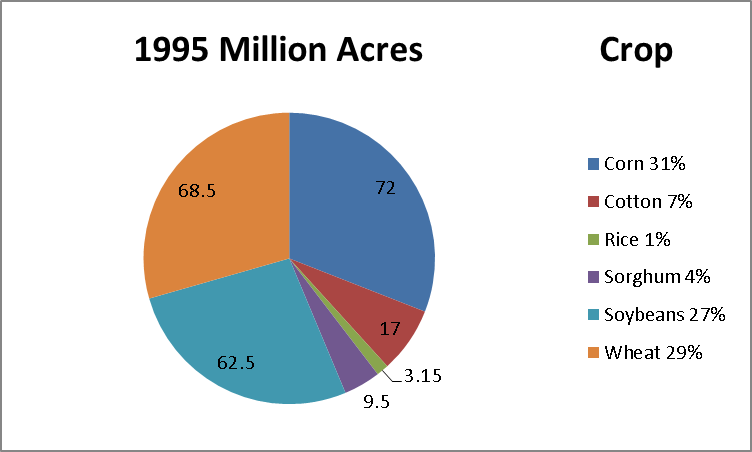

The pie chart above shows the distribution of Farmland per crop type, in Acres and as a percentage of total land mass, in the USA for the year 2014. The Chart below shows the same distribution but for the year 1995, we can see how the multi-purpose use of Farmland has actually taken place. More Farmland has been designated in 2014 compared to 1995 to Corn and Soybeans, with the decline coming from Cotton and Wheat. There may be many factors that determine the explanation, but the most conclusive is that Farmers found Corn and Soybean more advantageous in price.

Data from National Agricultural Statistics Service

Data from National Agricultural Statistics Service

Farmland investing also implies agency risk, that is to say the dispersion of income due to a third party not making the best decisions to maximize returns. This can happen as the Farmer or entity managing the Farmland may take decisions contrary to those of the investor. Another risk associated with Farmland investing is political risk, that is risk arising from a reduction in government subsidies to agriculture or in a worse case scenario land confiscation and expropriation as happened in Zimbabwe.

How to access Farmland investments

The Main way to gain exposure to Farmland investments is through REITs that invest solely in Farmland. Many of these REITs are agriculture businesses that have repackaged the farmland into these tax efficient and publicly traded vehicles. TIAA-CREF last August raised a $3 billion REIT for Farmland, demand for this investment is rising as investors look to diversify risk and gain access to new sources of return. Another route is to invest in an ETF that tracks an Agribusiness index like the DAX Global Agribusiness Index (DXAG Index) A well known example in this case is the Market Vectors Agribusiness ETF, probably well known also thanks to its ticker, MOO.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst