Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

If you are a high-income earner, you may be limited in what amount you can contribute to a Roth IRA, or not allowed to contribute whatsoever. Thanks to a tax loophole it is still possible to get your extra savings into a Roth IRA, with what is known as a Backdoor Roth IRA.

The process, to simplify it greatly, starts with contributing to a Traditional IRA up to your yearly limit. You then request a rollover, or conversion, to a Roth IRA. You have now circumvented the restriction on your income for making contributions to Roth IRAs

Roth IRA Income Limits for 2021-2022

The table below shows the income limits which affect the contribution amount you may make to a Roth IRA. These figures refer to your modified AGI.

Source IRS

Background on Backdoor Roth IRA

Until 2010, high-income earners couldn’t make conversions from one IRA to another. Before that year the yearly income limit was $100,000, after which you could not make IRA conversions.

Eliminating the income limit for conversions allowed people to contribute to an IRA where income limits do not apply. They could then convert the Traditional IRA to a Roth IRA; hence the Backdoor Roth IRA was created.

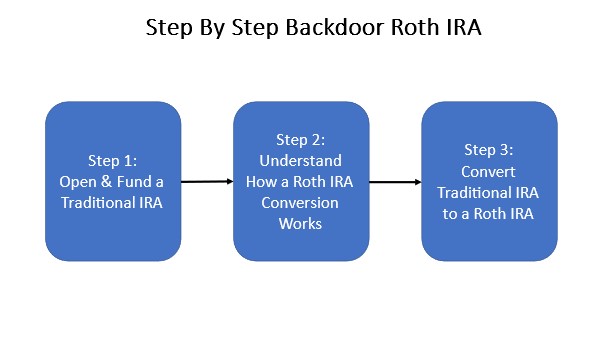

How to Set Up a Backdoor Roth IRA

To avoid possible penalties when converting a Traditional IRA to a Roth IRA you need to follow certain guidelines. Let’s take a look at how to proceed in 3 easy steps.

Step 1: Open & Fund a Traditional IRA

Open a Traditional IRA and fund the account with non-deductible contributions. You can also use a preexisting account to convert to a Roth IRA. However, in this account, you probably contributed untaxed dollars. You may also have earned some income from your investments.

These two factors may impact the taxes you will have to pay when you make the conversion to a Roth IRA. If you haven’t had the Traditional IRA for very long and growth hasn’t been that high, you may find that the tax on the conversion may still be worth it. Consult a tax planner for expert advice.

Many investors have been opening a Traditional IRA every year since 2010. Funding the new IRA with non-deductible contributions, and immediately converting to a Roth IRA. Note that you must file an IRS Form 8606 listing the non-deductible contributions.

Step 2: Understand How a Conversion to a Roth IRA Works

If your Roth IRA and Traditional IRA are with the same account provider, a simple same-trustee transfer shouldn’t be too complicated. Check with your IRA company about the paperwork needed to make a conversion.

If you have IRAs with different account providers making a trustee-to-trustee transfer of funds shouldn’t be excessively complicated either. Some IRA companies won’t handle fund transfers, in this case, they will pay you a check.

You must deposit this check into a Roth IRA account within 60 days of receipt. The IRS may consider you are making an early withdrawal if you hold onto the cash for longer. Early withdrawals may incur taxes and penalties.

Step 3: Convert Your Traditional IRA to a Roth IRA

Make the conversion from a Traditional IRA to a Roth IRA as soon as possible. Early conversion will help you avoid possible income gains from your investments in the IRA. Income earned from the IRA with non-deductible contributions could be taxed when you make the conversion to a Roth IRA.

However, there is no time limit as to when you can make the conversion from a Traditional IRA to a Roth IRA. Although, if you already had funds in your Traditional IRA, you may want to wait for later in the year to see how the account settles to minimize potential taxable gains.

Backdoor Roth IRA: Special Considerations

Backdoor Roth IRA conversions merit special attention to a few features and special taxable situations that may arise inadvertently.

5-Year Rules for Backdoor Roth IRAs

With a Roth IRA, you can take distributions on any amount without inferring income tax charges when they are qualified. One of the criteria for qualified distributions is respecting the 5-year rule, which states that 5 tax years must have passed before you take a distribution.

The IRS treats conversions as contributions for this purpose. So, if you are converting a Traditional IRA into a new Roth IRA, you must respect the 5-year rule before taking any distributions. The 5-year rule also applies if you are over the age of 59 ½.

You may have more than one Roth IRA, which may be the case when converting a Traditional IRA to a Roth IRA each year. However, you only need to satisfy the 5-year rule for one Roth IRA for all of your Roth IRAs to satisfy the rule.

Because you contribute non-deductible dollars to your Roth IRA, you may take distributions of principle even if you are under the age of 59 ½. However, you must still respect the 5-year rule for each conversion. If you convert a Traditional IRA to a Roth IRA yearly, then for each IRA 5 tax years must pass before withdrawing principal amounts.

Traditional IRAs with deducted Contributions

Things get a little bit more complicated if you have preexisting Traditional IRAs with both taxed and untaxed contributions. When you create a Backdoor Roth IRA, the IRS treats the conversion as a distribution.

The IRS does not allow you to separate your taxed contributions from your untaxed contributions. When you convert your Traditional IRA to a Roth IRA the total funds will be contributed to the new IRA, both taxed and untaxed.

The IRS does allow rolling over the untaxed dollars to a new Traditional IRA and converting the taxed contributions only to the Roth IRA. The IRS does not allow you to take distributions or make a conversion with only one of the 2 types of contributions.

This rule is often referred to by the “cream in your coffee” saying. Just like cream, once you add it to your cup of coffee you cannot separate the cream from the coffee anymore.

State Taxes on Backdoor IRA Conversions

The majority of states that charge income tax consider Backdoor Roth conversions in the same way the IRS does. However, some states might exempt parts of a pension or IRA distribution from taxation if the person is over a specific age.

Other states may entirely exclude the whole conversion amount from taxation. States without an income tax law will not tax any amounts for conversion. Getting the help of a tax professional will help you navigate the ins and outs of state and federal tax rules for Backdoor Roth IRAs.

Is a Backdoor Roth IRA Worth It?

Whether a Backdoor Roth IRA is the right arrangement for you depends on your particular situation. Some things to consider before going ahead.

Those Who Can Benefit from a Backdoor Roth IRA:

- High-income earners who don’t qualify under current IRS rules to contribute to a Roth IRA.

- Investors who can afford the taxes on the Roth conversion and want to take advantage of the tax-free growth and distributions.

- At retirement, those who wish to avoid compulsory required-minimum-distributions at age 72.

Those Who Won’t Benefit from a Backdoor Roth IRA:

- Investors who are already eligible to contribute to a Roth IRA or have access to an employer-sponsored Roth 401(k) that they haven’t maxed out yet.

- Those who anticipate they may need to access the funds in the Roth IRA before 5 tax years. Penalties may apply if you need to withdraw those funds early.

- If you have preexisting Traditional IRAs that complicate matters under the pro-rata rule. The tax consequences may burden the conversion to the point where the extra taxes outweigh any benefits.

Build Back Better Legislation

Build Back Better legislation had proposed to terminate the possibility of converting Traditional IRAs into Roth IRAs. This is considered a loophole that wealthy Americans can legally use to contribute to Roth IRAs.

The bill was voted down in 2021, but the bill is still under discussion in the Senate. If passed the new legislation would effectively put an end to Backdoor Roth IRA conversions for anyone. It would also restrict the amount of money held in retirement plans for the super-wealthy.

The questions that are concerning most people are: does this bill have a chance of passing? And would this bill be retroactive? According to Aron Szapiro, head of retirement studies and public policy at Morningstar, it’s very unlikely.

Szapiro sees at least a couple of Senators who would like to end this provision, as the tax revenues associated with the loophole are modest. He also believes that the likelihood of the bill being retroactive is close to zero.

Wrapping Up

The Backdoor Roth IRA loophole offers opportunities for those with higher incomes that cannot contribute to a Roth IRA otherwise. Be sure to consult with a financial planner to get all the expert advice needed to meander through the IRS maze concerning rules for conversions.

You may be thinking of setting up a Traditional IRA for the purpose of converting to a Roth IRA and adding alternative investments. To invest in this type of asset class, you need a Self-Directed IRA.

Choosing an appropriate IRA company for your self-directed IRA needs is fundamental to achieving the best results. You can get all the information you need in our review of the top Self-Directed IRA companies

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst