Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Using a 401(k) as a retirement vehicle is one of the best ways you can start to save for retirement from a young age. Since a 401(k) is typically an employer-sponsored plan, you can start contributing to your 401(k) right when you start your working life as long as your employer offers it as part of your benefits package.

An added benefit to most 401(k) plans is that some employers offer a “match,” which means the employer matches a percentage of your contributions as an incentive for you to stay with the company.

While the 401(k) might sound like a no-brainer, there are some details you should be aware of before you decide to contribute 15% of your paycheck to your company’s 401(k) plan.

Continue reading to discover everything there is to know about the 401(k) for dummies, including the benefits, drawbacks, tax implications, and limitations of this tried-and-true retirement savings plan.

The Basics of a 401(k)

Named after the tax code subsection where the plan is described, a 401(k) is a “salary-deferral” plan offered by private sector employers to their employees.

Salary-deferral plans are often self-directed, meaning you’re responsible for choosing the investments for your own money. For example, you may have the option to select from a list of domestic stock indexes, money market funds, or bond yields.

A self-directed 401(k) allows for better diversification and gives you control over your money and where you choose to allocate it.

However, having a self-directed 401(k) means more responsibility when managing your money. Making poor allocation choices could lead to losing a substantial portion of your retirement savings over the forty or fifty years of your working life.

Using this helpful guide from FINRA.org explains the process for choosing your investments and how to build a diversified portfolio through a self-directed 401(k) plan.

Benefits of a 401(k)

A 401(k) comes with plenty of benefits that make it an excellent option for those that plan on saving for retirement. The main benefits you’ll receive if you start contributing to a 401(k) include:

- Contributing to a tax-advantaged account

- The ability to choose your investments

- They may help to lower your tax bracket

- More flexible options for contributions

- A variety of investment options are available

- Employer matches

- High contribution limits

Drawbacks of a 401(k)

While the benefits of contributing to a 401(k) outweigh the disadvantages, you should still be aware of the implications and limitations of the 401(k):

- Investment options may be limited depending on your employer

- Account fees may be higher than expected

- High fees if you need to take an early withdrawal

- The company match may be minimal

- Penalties for early withdrawal

- The company match is irrelevant if you leave the company without meeting the vesting period

- Tax implications once you start taking distributions

Contributing to a 401(k)

Employees contribute to their 401(k) by electing a percentage of their paycheck to be taken out and automatically placed into the 401(k) each pay period.

While there are no set rules for how much or how little you should contribute to your 401(k), most experts agree that contributing between 10 and 15 percent of your paycheck is a safe bet.

The amount you decide to contribute to your 401(k) depends on several factors, including:

- Your income

- Your age

- How close to retirement you are

- Whether or not you have other debt like a mortgage or student loans

- Annual contribution limits

Contribution Limits of a 401(k)

One of the core traits of a 401(k) and other retirement vehicles like the Roth IRA is that you have “contribution limits” that you must not exceed in a calendar year.

Contribution limits vary depending on the retirement vehicle and often change every few years. For example, the employer contribution limit for a 401(k) in 2023 is $22,500, while it was $20,500 in 2022, and $19,500 in 2021.

Below you’ll find a visual representation of how contribution limits change over time:

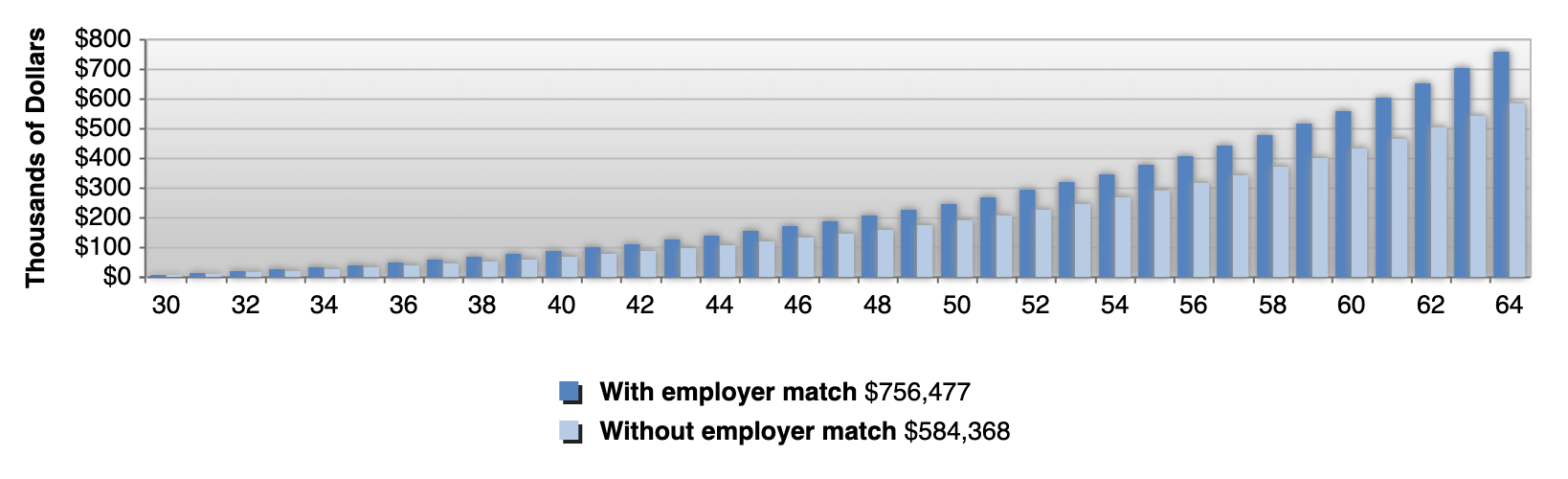

What About the Employer Match?

An employer match is an incentive for employees to stay with their company where the employer matches their contributions up to a certain amount. Most employers determine their employer match percentage based on the percentage of employee contributions.

For example, a company may choose to contribute 50% of the first 5% that an employee decides to contribute to their 401(k). If the employee’s annual income is $60,000 and they contribute 10%, they’ll contribute $6,000 and their employer will match 50%, meaning they’ll contribute an additional $3,000 each year. It’s often considered a good idea to contribute as much as needed per year to maximize your employer’s contribution.

Vesting Periods

Most employers establish a “vesting period” that determines how long it takes for the employers’ contributions to belong to the employee. A standard vesting period for many private sector employers is three years, meaning you’ll have to stay with your company for at least three years before their matched contributions belong 100% to you.

Depending on your employer’s vesting schedule, you may have to return all employer contributions if you leave the company without meeting the vesting period.

Withdrawals

The 401(k) is a retirement plan, which means it’s not designed for you to take withdrawals (or distributions) while you’re just beginning your working life. Most withdrawals taken before age 59 and 1/2 have a 10% penalty.

You can take retirement withdrawals without penalty starting at age 59 and 1/2, and withdrawals taken after this age are taxed as ordinary income at your current tax bracket.

You should know that you aren’t required to take any distributions until you reach 72. Once you turn 72, the IRS requires you to take annual taxable withdrawals as required minimum distributions.

Another option is to take out a 401(k) loan. You may borrow against your 401(k) balance without incurring penalties. If you decide to change jobs, you’ll be required to repay the loan when your next tax return is due.

401(k) Rollovers

Another benefit to 401(k) plans is that you can transfer your contributions (or “rollover”) if you decide to leave your current job.

In a 2020 News Release by the U.S. Bureau of Labor and Statistics, they found the median number of years employees stay with their company is only 4.1 years. This tenure continues to get smaller as young professionals tend to switch jobs more frequently.

The government introduced the rollover option with the 401(k) to account for the possibility of employees switching companies or leaving their working life altogether.

There are two types of rollovers available:

- Direct Rollover: A direct rollover happens when you request your plan administrator to send your balance directly into another retirement account which can be an IRA or a 401(k) plan with your next employer. No taxes are incurred or withheld with a direct rollover.

- 60-day Rollover: You also have the option for your employer to send your 401(k) balance to you directly. You’ll then have 60 days to deposit your balance into an IRA or your new 401(k) plan with your next employer.

IRA vs. 401(k)

There are several differences between a traditional IRA and a 401(k) you should know if you want to plan for your retirement. However, you can contribute to these retirement plans simultaneously (and we highly recommend you do).

One distinct difference between an IRA and a 401(k) is that your employer offers a 401(k), while individuals open IRAs using a broker or bank.

A Roth IRA is an individual retirement account that uses after-tax dollars and allows tax-free withdrawals once you reach age 59 and ½.

The Roth is an excellent option since you pay taxes on your contributions now and withdraw them at a later date tax-free.

Since you’ll likely have a higher income and be in a higher tax bracket later in life, opening a Roth IRA and contributing while you’re in a lower tax bracket will allow you to withdraw more money when you reach age 59 ½.

Opening an employer-sponsored 401(k)

Opening a 401(k) sponsored by your employer is a straightforward process.

First, you’ll need to know which company your employer uses to sponsor your plan. You should receive information in your onboarding paperwork that tells you the basic steps to set up your new account and begin the process of contributing to your 401(k).

Choosing your contributions

Those beginning their working careers should have a different strategy for contributing to their 401(k) than those getting ready to retire.

Young professionals should aim to put 10% of their gross wages into their 401(k) to start. If 10% is too much, 4% to 5% is a viable option as long as you plan to contribute more as your role grows and you get pay raises down the line. For many, “maxing out” their employer’s 401(k) contribution is often seen as a key strategic priority, otherwise you effectively leave money on the table. Usually, this involves contributing as much as you’re legally allowed to your 401(k) within a given year.

Remember that most employers have a waiting period before you can contribute to your 401(k), typically around 60 to 90 days.

Picking your investments

Each individual 401(k) plan has a selection of investment options for employees to choose from. Young professionals can choose investments with a higher risk profile since they are furthest from retirement. Those closer to retirement should opt for a diversified portfolio that fits their risk tolerance.

We recommend doing research into the investment options you have to choose from. If you have a financial advisor or a trusted friend familiar with 401(k) allocations, you may consider asking them for advice on allocating your funds.

401(k)s are generally quite restrictive in the kinds of assets in which you can invest. For example, some alternative investments traditionally available to IRA investors are, in most cases, excluded from 401(k) eligibility, including:

- Precious metals

- Collectible items and antiques

- Fine art

- Some annuities and defined-payment plans

- Cryptocurrencies (depending on employer plan)

However, there are some specialized retirement investing companies that cater to gold and precious metals investors. If you’re interested in diversifying your portfolio with non-traditional assets, consider going with one of America’s top-ranked gold 401(k) companies.

Self-employed 401(k)

While far less common, self-employed individuals without employees have the option to open an individual 401(k), which works much like an employer-sponsored plan.

The self-employed 401(k) is ideal for sole proprietors or independent contractors because they can still make pre-tax contributions from their earnings and invest the funds in various investment options.

An individual 401(k) allows business owners and contractors to put away more money yearly than those with an employer-sponsored plan. For example, they’ll be able to contribute up to $66,000 per year for tax year 2023.

Final Thoughts

Opening a 401(k) with your employer or as a self-employed individual is a great step towards a comfortable retirement. Plenty of benefits make the 401(k) one of the best retirement vehicles you can take advantage of, regardless of where you’re at in your career.

New investors should take advantage of the tax benefits of a 401(k) and the concept of compounding interest. If you contribute 10% of your gross income starting from age 25 with an annual rate of return of 7%, at age 60 you’ll have roughly $1.61 million in your 401(k) retirement plan (see below).

For more helpful information on getting started with your retirement planning, find out how to set up a self-directed IRA, which permits a host of diversified assets not allowed in traditional IRAs. An IRA may be preferable to investors who are ineligible for an employer-sponsored 401(k), or to supplement your retirement savings.

Liam Hunt, M.A., is a financial writer covering global markets, monetary policy, retirement savings, and millennial investing. His commentary and analysis have been featured in the New York Post, Reader's Digest, Fox Business, and Forbes.