Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

The hedge fund industry is filled with superstar managers. They consistently turn out above-average returns, making enough money for their investors that their notorious management and performance fees don’t take too much off the top. These finance rock stars use different strategies to exploit inefficiencies in the market and deliver “alpha” – that is a return that is more than a given benchmark, usually an index like the S&P 500.

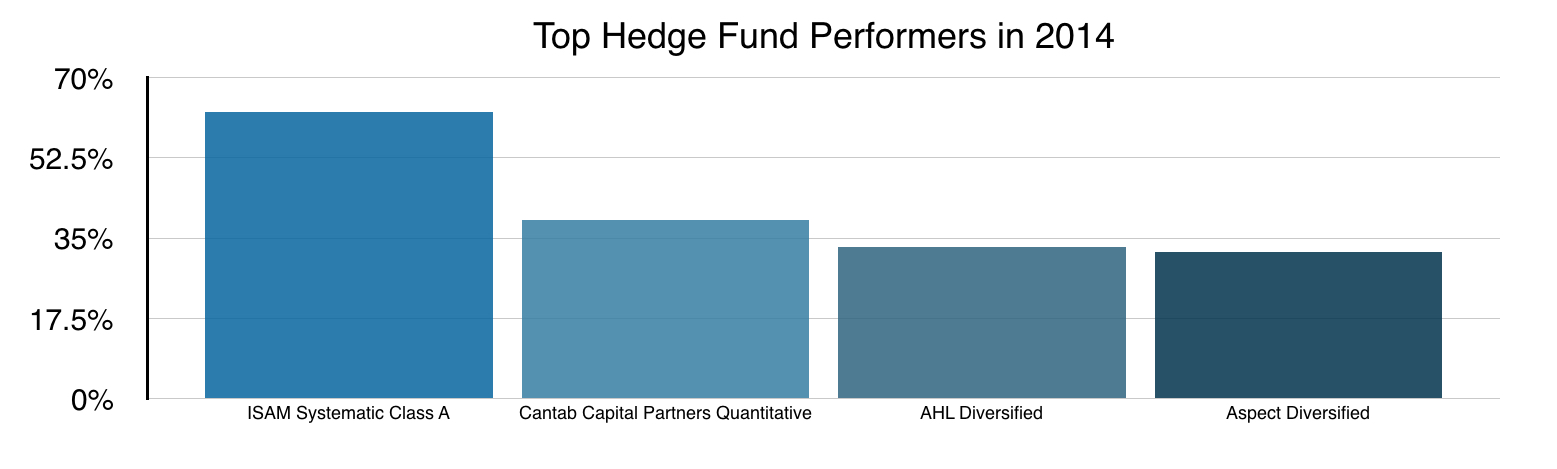

Point in fact, last year several funds brought in returns over 30 percent, including the $13.4 billion Man AHL, the $4.7 billion Aspect Capital, and the $3.8 billion Cantab Capital Partners:

Chart by CNBC, “Hedge fund robots crushed human rivals in 2014”, published 5 January 2015

The problem is that you probably can’t invest with them. “These superstars are unlikely to need your money,” explains BloombergView. “By the time we discover them, they already have a lot of capital, and taking on more would make it hard for them to keep generating market-beating returns.” This leaves you with two choices: “find a hedge-fund who can reliably beat the market for you is to pick one who’s not yet a star” or find a way to replicate hedge fund returns.

HFRX Global Hedge Fund Index

Strategies for recreating hedge fund returns are not just possible; they are even probable when looking at the hedge fund industry as a whole. Take the HFRX Global Hedge Fund Index for example. It replicates hedge fund returns, net of fees. The HFRX can provide a way for you to get a taste of hedge fund returns or be a solid addition to help diversify your portfolio.

The only problem here is that when you rely on an index, you include the high-flying hedge funds as well as those with less than enviable performance. Hedge Fund Research (HFR) created an HFRX Global Hedge Fund Index that is “designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies; including but not limited to convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage, and relative value arbitrage.”

That sounds pretty good but look at its performance.

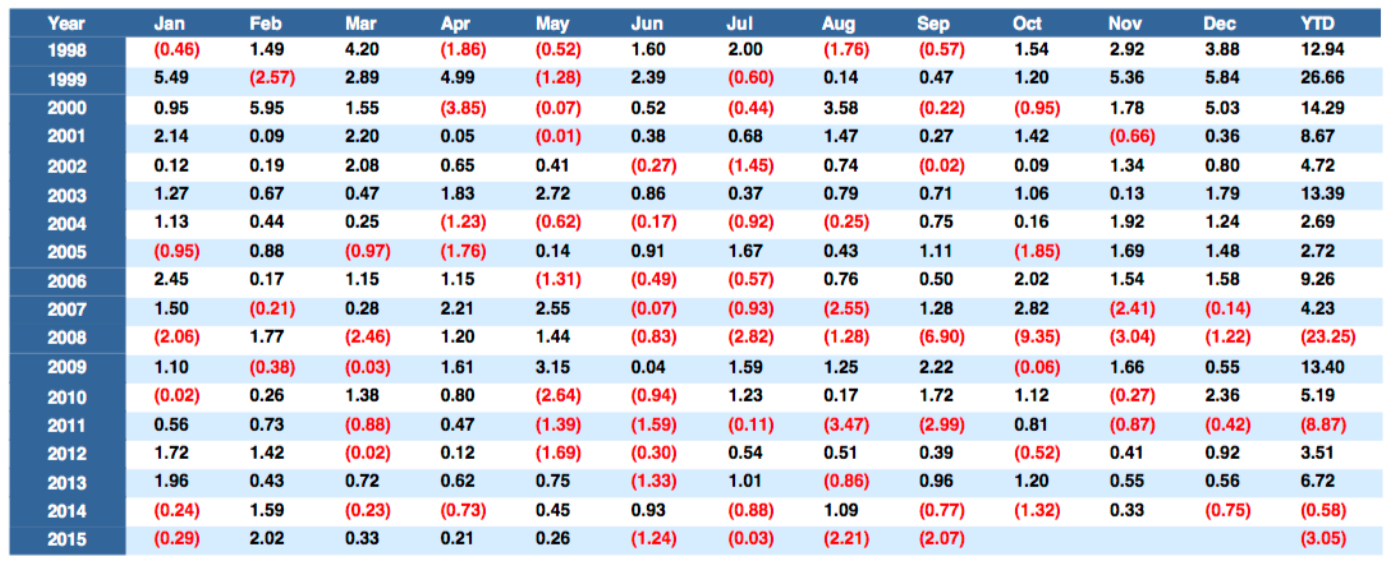

HFRX GLOBAL HEDGE FUND INDEX (HFRXGL) FROM 01/1998 TO 09/2015

All in all, the annualized return of the Index since 1998 is 4.68 percent. For comparison the 3-month LIBOR USD was 2.58 percent for the period.

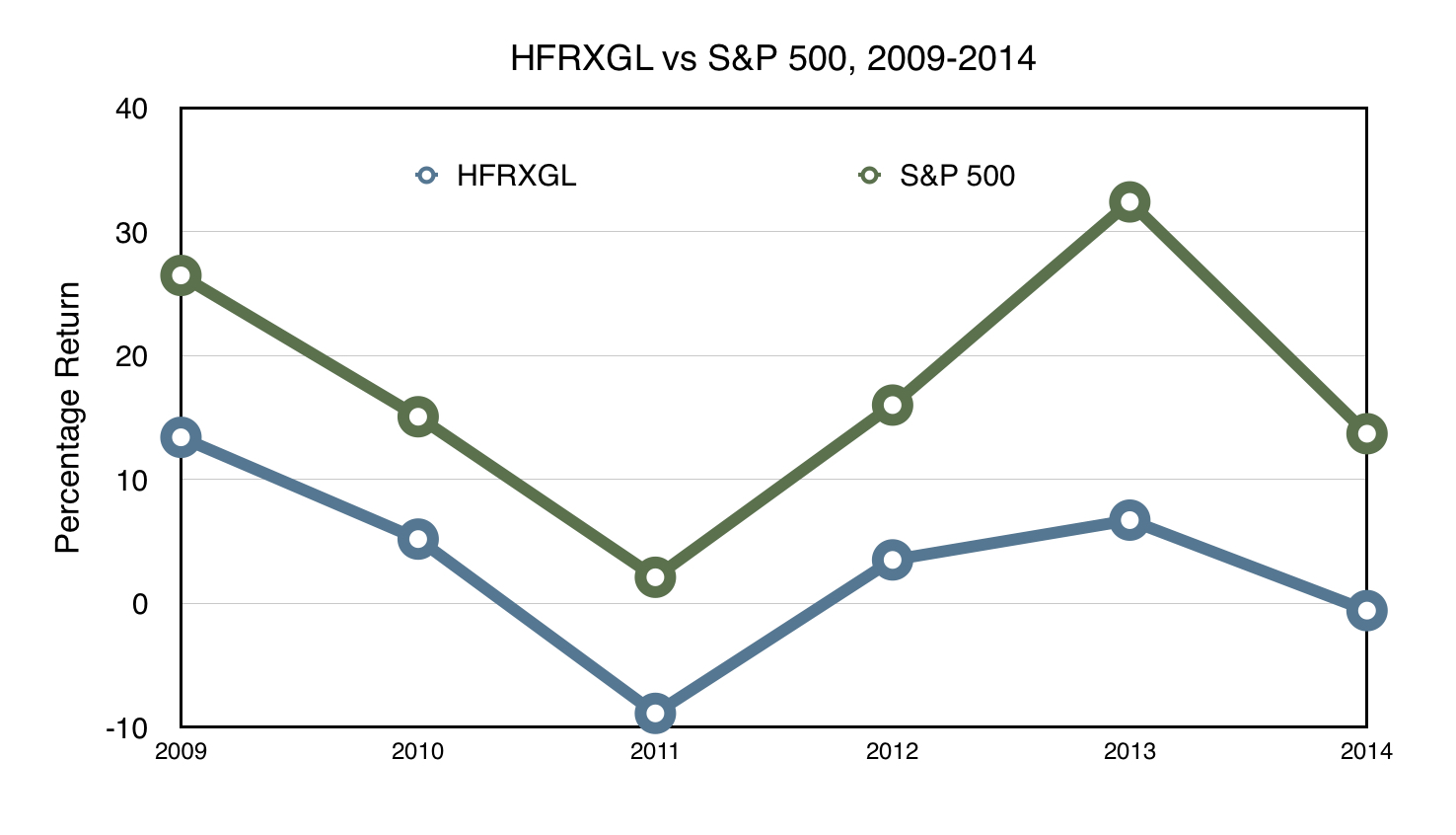

Hedge Funds vs. the S&P 500

That might not sound too bad, but remember that the S&P 500 annual total return for 2014 was 13.69 percent, and looking at the past five years, the S&P 500 completely outpaced the HFRX Global Hedge Fund Index.

DATA FROM HEDGE FUND RESEARCH AND Y-CHARTS

That said, when looking at specific events, hedge funds do tend to deliver on reducing volatility. Think of the volatile dip in the market during the August 17 to August 24 week. “Returns ranged from a positive 0.2 percent (for managed futures funds) to a negative 4.8 percent (for equity hedge funds),” explains the New York Times, “which is much better than the roughly 9.4 percent drop in the S.&P. 500 for the same period,” and some funds, like the MainStay Marketfield fund, actually saw a small (almost 1 percent) increase during that short dip.

So the real question is how can you achieve alpha while getting lower volatility.

Broad Strokes

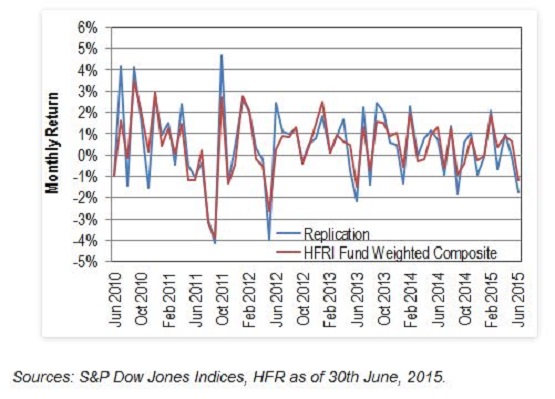

The simplest way to replicate hedge fund returns on a broad scale is to invest half your money in stocks, like the S&P 500, and the other half in bonds, according to the senior director of index investment at S&P Dow Jones Indices, Tim Edwards, in a Wall Street Journal article. Using the S&P U.S. Aggregate Bond index to represent bonds and the S&P Global 1200 index to represent stocks, the results are pretty similar to the Hedge Fund Research Institute’s fund:

Chart from Wall Street Journal

A similar approach gained some traction a few years ago. The New York Times called it the “50-50 Solution” after a report from Vanguard in 2011 advocated for something similar as a way for investors to produce consistent returns.

“The average real returns of such a portfolio since 1926 have been statistically equivalent regardless of whether the U.S. economy was in or out of recession,” according to the Vanguard report. “During expansions, the model portfolio had average real returns, factoring in inflation, of 5.6 percent, compared with 5.3 percent during recessions.”

Getting Higher Returns

Of course, while hedge funds were originally designed to deliver returns with less volatility, there are those investors who are drawn to the investment vehicle and news of its rock star managers because of the dazzling high returns. If this sounds like you, remember that higher rewards equal greater risk.

That said, you could replicate the returns of your favorite hedge fund through a method called “Individual Position Replication”. In this method, you would pay attention the filings that hedge fund makes with the Securities and Exchange Commission (SEC). All hedge funds have to submit 13F filings every quarter and a 13D filing any time they acquire more than 5 percent of a company.

This method has a significant disadvantage in that it is backwards-looking, and the hedge fund may have only held the position in question briefly, exploiting whatever advantage and exiting the position well before you ever learn of it. However, if you try to ape a hedge fund that tends to take longer positions, you might be able to win out on value.

The Bottom Line

Replicating hedge funds is a decent strategy for producing consistent returns, but you are not going to be able to get those larger returns without taking on more risk. A 50-50 portfolio will deliver fairly consistent returns. Individual position replication can take some of the guesswork out of managing your portfolio when you want to try your hand at investing in individual companies, but be aware that you see those positions after the fact.

Renee Ann Breiten is a freelance finance writer and former management consultant with over 15 years of experience in business management and strategy. She earned an MBA in financial management from Exeter in 2007 and has enjoyed a variety of international business experiences, working primarily in England and Australia. Breiten's work is centered on technology, consumer trends, and investing strategies. Her writing has appeared on TheStreet, Marketwatch, Insider Monkey, Seeking Alpha and Motley Fool.