Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Hedge Fund Longevity

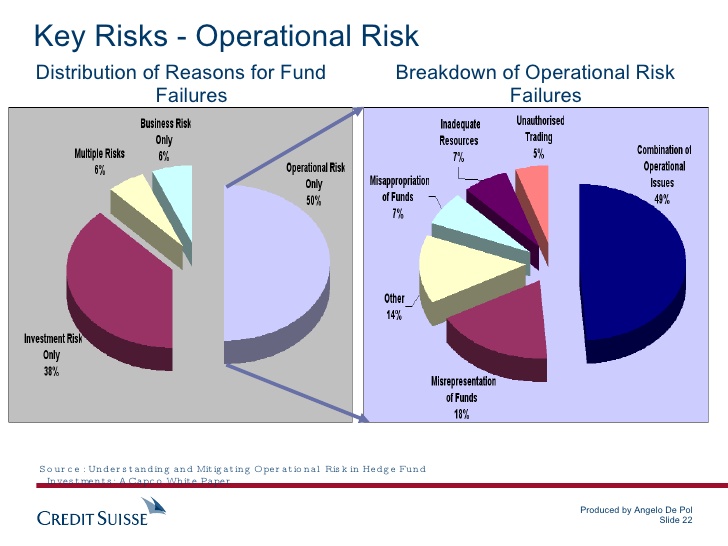

It is vital that Due Diligence is performed before investing in any fund. This helps us take on less risk and hopefully avoid funds that are managed badly, more likely to fail, or simply more likely to be fraudulent. Hedge Funds are well known for being likely to have a short life. The singular most common reason for Hedge Fund failure is actually operational risk, not market risk as most would probably think. This type of risk includes inadequate resources, unauthorized trading, fraud, and other events which may include external events and people. We will leave aside in this article the analysis of risk and return in the due diligence process. There are some other questions that should be asked when analysing a fund Manager that should help us avoid Hedge Funds that are likely to fail.

Red Flags

It would seem a mundane question but who is the Auditing firm? This is actually a more important question than it may initially seem. A Fund manager with the intent to commit fraud would be easily helped if he is using an auditing firm that he set up himself or of dubious reputation.

A well-known example of Hedge Fund fraud is the Bayou Management Fund, founded in 1996 it began making losses immediately, by 1998 to be able to conceal those losses the two General Partners fired the auditing firm and appointed another firm which they had set up themselves. One of the General Partners was the sole owner of the auditing firm and it had no other clients. By 2005 things began to unravel, however until then the GPs continued to claim incentive fees based on their fraudulent performance. Simple questions like asking full details of the auditing company and the actual staff from the auditing company assigned to the fund should be asked.

Another top question is who is in charge of risk management? Along with a series of questions derived from that one. Does this person have the authority to close down or re-size positions that are becoming too risky? Traders may often feel that keeping a losing position will see them eventually return to a profit, this can sometimes exacerbate an already critical situation. Does the Risk Manager have the power to over-ride the Trader’s will? Has he had to apply his/her authority in such a situation before? If this is so in what circumstances did these actions occur and what were the conclusions. Is the Risk Manager also the Portfolio Manager, Trader or CEO? This can create conflicts of interest which mitigate the utility of having a Risk Manager.

Amaranth Hedge Fund collapsed in 2006 with losses of $6.6 billion around 70 percent of the value of the fund. There where various factors that compiled together to bring around the fund’s demise but one of them was certainly the lack of intervention in terms of risk management. The fund’s star trader was allowed to be in total control of his trades. It is true the types of trades he placed in natural gas in 2006 had been working for the past two years, however more than half of the fund’s capital was tied into that market at one point. High concentration in a losing trade should not have been allowed to happen. The trader lost $4.6 billion in one week alone, if a Risk manager with the authority to act had been in place the positions in Natural Gas would have been closed well before losing so much money and ultimately sinking the fund.

Feasibility of the strategy is also an important factor in due diligence and should raise red flags when they do not seem to make sense, are extremely simply or so complex that they are impossible to understand. A good example of feasibility in strategy is the Bernie Madoff fund Ascot Partners. True it was a Ponzi scheme but everybody who invested in it were in reality tricked into believing something that was too good to be true. The strategy was an Option Collar on equities, this consisted of buying a Call option with a higher strike and selling a Put option with a lower strike, when long of the underlying this limits your profits to the upside and downside. Bernie Madoff’s returns were very stable and predictable year after year and through different market cycles. This created a lot skepticism form certain people. His scheme was actually discovered by Harry Markopolos well before the scheme imploded. It’s clear that Hedge Funds may use Collar options strategies within their broader fund strategy, but this was all that Madoff’s returns were about. There are also no other funds using solely this option strategy; these two assumptions should have sounded warning bells.

It may be impossible to mitigate all investment risks, but asking the right questions may help in reducing those risks dramatically. Having access to the managers, key personnel and outside providers is part of the transparency a Hedge Fund manager should offer to attract investors. A lack of availability or cooperation should also ring alarm bells as the information necessary may not be available or accessible in a timely manner.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst