Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Why define investment styles?

The concept of investment style is imported from traditional assets like Stocks and Bonds. An example of investment style for Stocks may be Mid-Cap domestic growth. It is basically a way of distinguishing and defining which sector within an asset class the investment is aiming for. This helps an investor define a suitable peer group to assess and evaluate how well the investment is performing going forward and also pre-allocation, to evaluate risk and return profiles compared to the investment’s peers. Style definition allows evaluating on a like for like basis at the single property level, an office building in the center of town cannot, or should not, be compared to a residential development land in the suburbs. Style definition also allows determining which type of Real Estate fund, portfolio or property best suits your investment time horizon, cash flow needs and risk appetite. Once an allocation to a Real Estate fund has been made Style definitions also help track if a manager is exposed to Style drift. That is he/she may be investing in properties outside of the core expertise of the fund, and not in line with the investment decision you took when you allocated capital to that fund.

Having a clear definition of investment styles allows for a better diversification within the Real Estate portfolio. As you are able to identify which characteristics are most suitable to your portfolio and add weight to the styles that meet your allocation criteria.

What are the Real Estate investment Styles?

There is no single broad Real Estate market definition of Styles. But I’m going to use the three types of Real Estate Styles, Core, Value-Added and Opportunistic, as they were defined by NCREIF.

Core Real Estate

Core investments involve commercial properties that have a steady income flow, usually from rents and leases with full or high occupancy. These properties are usually held for longer periods to fully take advantage of their income stream and have very low volatility. For this reason they are often considered as having a Bond like structure. The appreciation of the property is not the main factor of return as the income stream is considered fairly reliable. The types of property in this category tend to be offices, shopping malls and residential apartment buildings. Funds that invest mainly in Core properties use very little leverage. A small percentage of allocation to other Styles is considered acceptable.

Value-Added Real Estate

These properties tend to achieve a substantial proportion of their return through price appreciation, are usually more subject to price volatility and are not deemed as having the level of reliability in income streams as Core properties. They tend to be low cost housing complexes, Elderly care homes, Hospitals, hotels, resorts and so on. This Style may also include new properties that still have a low level of occupancy creating uncertainty in cash flows which places them in this category instead of being considered as Core properties.

Opportunistic Real Estate

These properties are often in need of redevelopment or are even at the initial development stage and are held for capital appreciation solely. They are usually held for short periods of time compared to Core properties, in the range of 3 to 5 years. Relying on capital appreciation alone and the short holding period means this type of Real Estate is also the riskiest. The investments are usually accessed through Private Equity Real Estate funds (PERE) which focus on investments with a high risk return profile. Within the Opportunistic Style you will also find foreign Real Estate in particular those in emerging markets. Funds with this style are more likely to use high levels of leverage in an attempt to enhance returns.

Attributes to define Styles

How do you know which fund is investing in what type? Well the investment memorandum will tell you, but part of due diligence means that you have to check that the manager is actually invested in what he says he is. You may also be considering individual properties, these definitions will allow you to define each property accordingly and help the process of having a diversified portfolio. NCREIF defined 8 attributes to help categorize the 3 different Styles.

1) Property type; that is what it’s used for, office, residence, retail etc.

2) Life cycle phase; i.e. new development with high risk or established property, high occupancy and low risk.

3) Occupancy; i.e. high occupancy or vacant.

4) Rollover concentration; how often has this property changed ownership.

5) Near term Rollover; likelihood of the sale of property as imminent.

6) Leverage

7) Market recognition; an office building in the center of a major city, or a retail outlet in a rural area.

8) Investment structure and control; the extent of control and type of governance.

These attributes to define investment style can be applied to a single property or a portfolio of properties. Managers that define the fund’s strategy should have properties that for the most part respond accordingly to all 8 of the above conditions.

Real Estate Style Box

It is very common for an Equity investor to choose to invest according to Value or Growth and then within those two categories choose amongst Small, Mid or Large Cap Stocks. Creating a Style box shows the possible combinations and helps an investor to see how the Equity portfolio allocation is distributed based on investment Style.

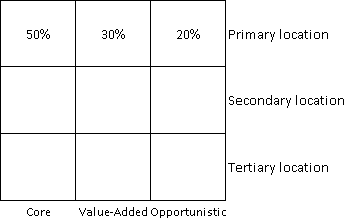

The same can be done for a Real Estate portfolio, an investor may choose between Core Value-Added and Opportunistic and then between Primary, Secondary or Tertiary location. Defining how the Real Estate portfolio will be split up is essential in the allocation process. Depending on your risk aversion and liquidity needs you will then proceed to choose how much of your Real Estate portfolio goes to each style and location.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst