Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Private equity (PE) makes the business world go ‘round. It is how new companies finance early beginnings, how young companies harness growth opportunities, and can facilitate the dealings of even the largest companies. It is risky because the business may or may not become successful, but the rewards can be enormous. With enough diversification, many private equity investors do come out ahead.

PE firms often have the influence to direct the borrowing company towards greater earnings, be it putting money in the right place, installing more experienced leadership, or mentoring management as needed. They keep the focus on boosting earnings and making the companies in which they invest profitable. Private equity firms make money as long as they are investing and coaching, but some factors can affect their ability to do so.

Image via Flickr by 401k Limits

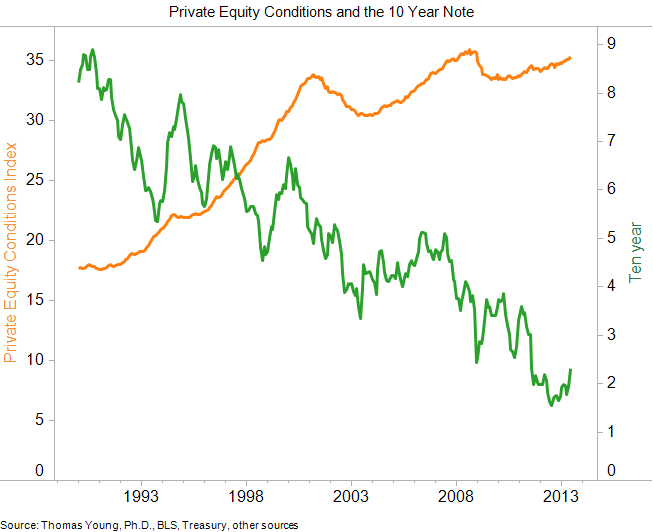

One of the biggest risks is on the horizon now – a Fed rate increase. While a slow, gradual rise in Federal interest rates could serve to increase corporate confidence in the economy to support mergers and acquisitions, that effect won’t be seen as much in private equity companies, or at least not right away. Moreover, private equity conditions are inversely correlated to its movement.

Just look at this chart comparing private equity conditions with 10-year T-bills:

Private Equity Firms

PE firms combine funds from various institutional investors and qualified to help companies raise capital outside of traditional financing options, like bank loans or stock issuance. To provide the most benefit, many private equity firms will leverage the capital they raise by taking on large amounts of debt. The resulting capital structure can sometimes be as high as 97 percent debt with just 3 percent equity. When interest rates are high, fixed costs are high, and that is if the PE firm can get the loan. Many lenders are hesitant to over-leverage an asset or a company as it is, let alone when cash flow is impeded.

Profit Cushions

Obviously, that level of leverage has its risks, but returns to investors are usually pretty solid so long as the company seeking financed is valued correctly, its inflows forecasted correctly, and its operations properly managed. However, changing interest rates can really take their toll. Not only does the cost of borrowing increase for the PE firm, but the necessary payments also go up. As that happens, most private equity firms will have to be more conservative with their investments because the profit cushion is smaller.

Financial Performance

In addition, when interest rates rise, companies within private equity portfolios are exposed to their own risk. If a company has loans with variable interest rates and those rates increase, it is going to cut into its bottom-line. This could affect its profitability, possibly even throwing the company into financial distress if its earnings are already low. In turn, the company may be prevented from making timely payments or could become less attractive for the PE firm’s exit strategy.

Exit Activity

In other words, higher interest rates mean that private equity firms could have difficulty exiting their investments. IPO activity is always highest when interest rates are low or declining because valuations tend to be higher and returns are greater. As interest rates increase, there could be a rush to exit certain deals.

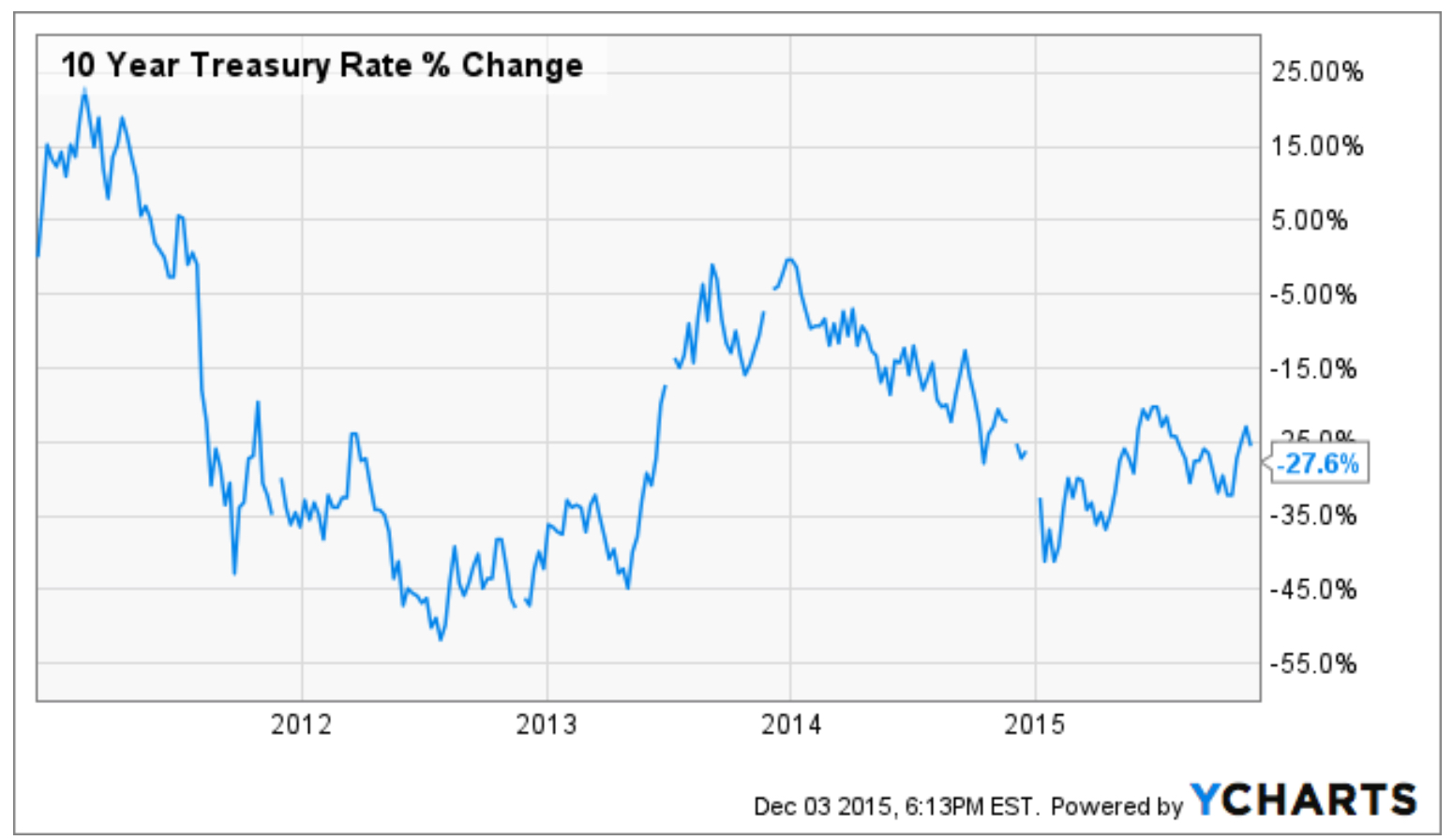

A 2014 report by Bain and Co. Found that the number of private equity-backed exits rose 15 percent to 2014 from 2013 and the value of those exits increased by 67 percent. This coincides with an increase in the 10-year Treasury bill rate:

When interest rates are going up, fundraising can become an issue. Asset valuations are often lower and retail investors have a decreased appetite for IPOs, making an exit through public offering more difficult. PE firms have to strategize in response.

Private Equity Acquisition

The effect can be felt in private equity acquisitions as well. When a PE firm takes on a transformative role with a company, the cost of the asset and the cost of obtaining the capital to finance an acquisition become paramount. As the cost of debt rises, PE companies are going to have to pay less for assets than they may have otherwise. Until confidence is assured or conditions change, PE acquisition activity is bound to slow down. Private equity firms may make smaller investments, invest in fewer companies, or a combination of the two.

Fewer Investors

When interest rates are low, investors turn towards equities and alternative investments to help create fixed income, or at least leave the possibility open. As interest rates go up, most investors are going to rebalance their portfolios. While this trend is more pronounced with retail investors, PE investors may do the same thing, especially if interest rates begin to rise quickly. This effect will not be as pronounced in institutional investors and different funds, but even they need to make sure their portfolios are adequately diversified.

Going Abroad

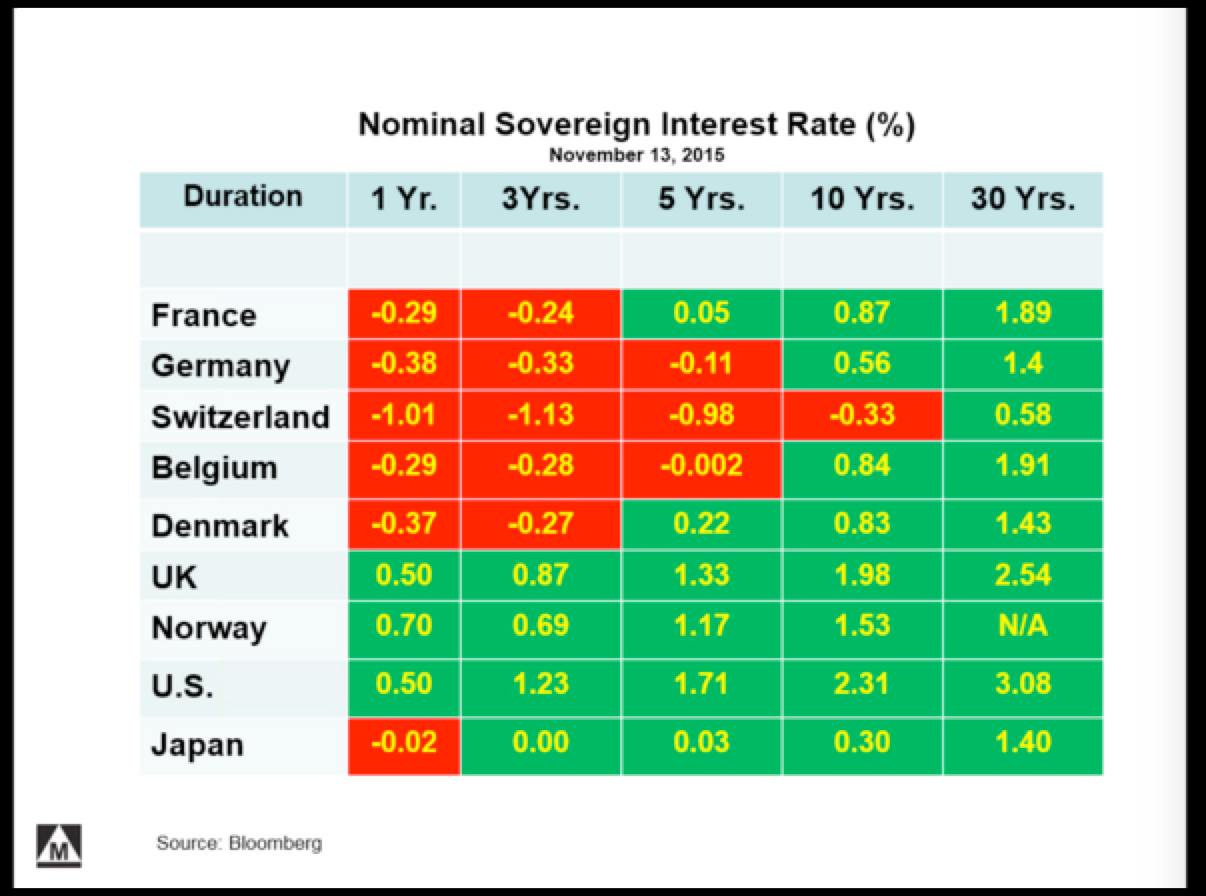

Of course, there is always a location effect. It is surprisingly cheap to borrow money in other parts of the world. While the United States may have stopped its qualitative easing program, the European Central Bank launched its own QE program in March 2015. Moreover, several countries in Europe have negative federal interest rates right now and the borrowing conditions in Japan are advantageous:

This could lead to some PE firms obtaining financing from outside the United States if the currency risk is manageable for the firm and its business.

Takeaway

An increase in the Fed rate will likely have an effect on the private equity market. Look for PE firms to seek exits at a higher rate and to be more conservative about the investments they make going forward. In addition, there may be some investors and institutions who rebalance their portfolios to reduce their private equity holdings because of the interest rate risk. The effect of interest rate increases will be proportionate to the pace at which the Fed raises its rates.

Renee Ann Breiten is a freelance finance writer and former management consultant with over 15 years of experience in business management and strategy. She earned an MBA in financial management from Exeter in 2007 and has enjoyed a variety of international business experiences, working primarily in England and Australia. Breiten's work is centered on technology, consumer trends, and investing strategies. Her writing has appeared on TheStreet, Marketwatch, Insider Monkey, Seeking Alpha and Motley Fool.