Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

There are fundamentally 2 reasons for including Commodities within a Portfolio, diversification and return enhancement. We will have a look at why Commodities may be good for diversification, therefore reducing overall risk and in what way they may enhance returns of a portfolio.

4 Reasons for diversification potential of Commodities

Firstly, Commodity prices are not determined by the present value of discounted future cash flows as would be the case with Bonds and Stocks. Therefore Commodity prices are not related to changes in forecast cash flows or discount rates, but are related to perceived supply and demand factors for the present and near future. This should mean that Commodity prices are not highly correlated to traditional assets.

Second, Commodities are positively correlated to Inflation, they are often components that make up the index for inflation. If it is not the raw Commodity sometimes their derivatives make up components of an inflation index, for example Gasoline or Bread. Stocks and Bonds on the other hand are negatively correlated to inflation. Higher inflation will mean higher interest rates and discount factors, this means future cash flows from these securities will be worth less.

Third, Stock and Bond prices reflect what the market believes is the current value of future income streams, whereas Commodity prices reflect immediate supply and demand pressure. As Stock and Bond prices are anticipatory they tend to be at their highest when the economic cycle is coming to the bottom of a contraction period. Whilst Commodity prices will be at their lowest when the economy is at a bottom. Reversely when the economic cycle is at the top so will Commodity prices be high whereas Stocks and Bonds will have begun to fall in price.

Fourth, when Commodity prices increase so do production costs for corporations, this will reflect negatively on Stock and Bond prices, for example high crude oil prices will negatively effect Air Line transportation corporations. There are exceptions such as Commodity production companies that gain in value when the Commodities they produce increase in price.

Return Enhancement

Return enhancement to the overall Portfolio comes from downside protection offered by the low correlation to Stocks and Bonds, plus Beta exposure to the systematic risks of commodity markets. In the case of a headline event Stocks and Bonds will usually react negatively to these shocks, whereas Commodities will usually act positively. Natural disasters or geopolitical events will have an adverse effect on Stock and Bond prices of corporations or governments involved in the area, but Commodities will more likely be pushed up in price due to the same event. Holding Commodities may therefore help absorb downside risk.

From the table below we can see the correlation of the GSCI Index with three other major traditional asset classes. All three show very low correlation to GSCI index, this index is based on commodity futures. But as they offer ease of use, transparency in pricing and liquidity, they are the vehicle of choice for broad investments in a basket of commodities.

Source CAIA body of knowledge

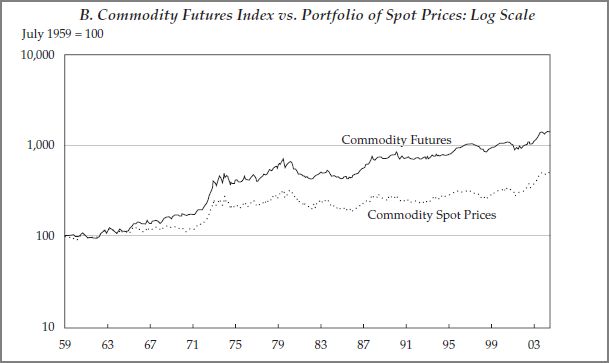

In a various studies Commodity futures have been shown to offer the same Sharpe Ratio and Returns as Equities. The paper by Gorton and Rouwenhorst 2006 shows that from 1959 to 2004 average monthly returns for Commodity Futures, Stocks and Bonds were 5.23%, 5.65% and 2.22% respectively. Standard deviation for Commodity Futures was 12.10% lower than Stocks at 14.85%, while Bonds showed lower volatility at 8.47%. The use of futures further enhances return given that investing in futures also produces roll return. This return is produced when the nearby futures contract is rolled into the next futures contract. The chart below, from the same paper, shows how returns for a Commodity Futures Index performed, on a log adjusted basis,compared to Spot prices for Commodities from July 1959 to December 2004.

Which Commodities ?

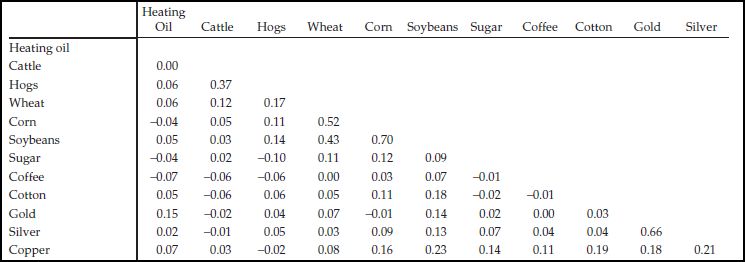

The role of a single Commodity may not be as clearly valuable as that of a basket of Commodities. Commodities have been shown to have very little correlation amongst themselves. Gold and Silver may have a comparatively higher correlation but then they will have very low and sometimes negative correlation to most other Commodities. A broad basket of Commodities then allows for creating more consistent returns. When some commodities may be under-performing other others may be out-performing. The chart below shows the correlations amongst 11 major Commodities.

Source Erb & Harvey 2006

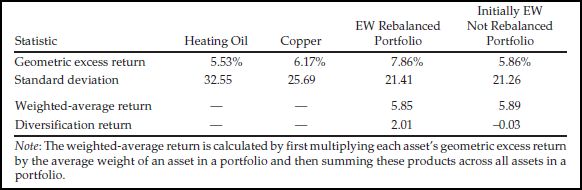

The highest correlations, as would be predictable are amongst Commodities within the same sector. Looking at Commodities from different sectors we can see that correlations are low and sometimes negative. This produces Diversification Return through rebalancing the portfolio of Commodities after a specified percentage move. This also allows for keeping the weights of each Commodity within the basket consistent with the initial weights. Consider a two Commodity portfolio of Oil and Gold, the initial weighting being 50% to each one. If Oil rises in price by 20% you would now have 54.55% of the Commodity portfolio in Oil and 45.45% in Gold. At these new prices the portfolio is clearly unbalance with respect to the initial desired exposures. Rebalancing can enhance performance of a broad basket of Commodities, below is a table of returns for a two Commodity portfolio with and without rebalancing.

Source Erb & Harvey 2006

We can see how the equally weighted return was higher at 7.86% compared to the unbalanced portfolio which had a return of 5.86%. Standard deviation remained more or less the same for both portfolios, just above 21% We can also see that the volatility for both individual Commodities was much higher than the volatility of the two Commodities combined in a portfolio. Confirming the theory that low correlation amongst assets helps reduce risk when they are combined in a portfolio.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst