Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Due Diligence consists of performing a careful, competent and thorough review of an investment, its soundness and its suitability. Due Diligence aims to identify the most appropriate funds for an investor considering various tax and legal characteristics, together with fund strategy, manager proficiency and performance profile.

Qualitative and Quantitative

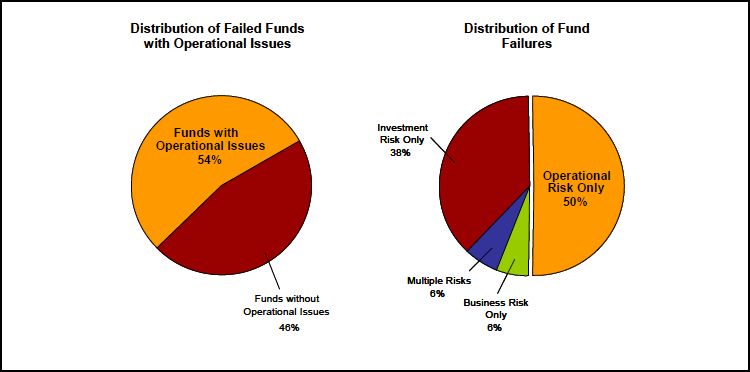

The process of due diligence in fund manager selection is defined by two types of metrics used in making the decision to invest with a certain manager, Quantitative and Qualitative analysis. These analyses are both used to determine which managers may be out-performers based on the quantitative analysis of their past records but even more so on the qualitative analysis of their organization, personnel and risk management. Many investors may be tempted to make allocation decisions based on strong performance results alone, this could prove to be extremely hazardous without a complete review of the fund and its operations. Feffer and Kundro found that amongst 100 hedge fund liquidations, spanning 20 years, half of the failures were attributed to operational risk alone. Their study shows it is the largest single risk for hedge fund failure, by far larger than business risk or investment risk.

Quantitative analysis involves comparisons to a peer group or index, considerations on risk adjusted returns, distribution of returns and performance attribution. The process should also consider the volatility of the fund and correlations to other assets within the investor’s portfolio.

The qualitative analysis should firstly answer 3 questions;

1) What is the investment objective?

2) What is the investment process?

3) How does the fund manager add value and what is the source?

Investment Objective

This question should define the manager’s general investment strategy, Long/Short, Macro Global or Event driven are a few examples, where the investments pursued are well defined and the assets or markets the strategy will operate in are also well defined. The fund manager should also ideally state a benchmark, which should be relevant to the strategy pursued and the assets that the fund trades in.

Investment Process

This is the process the fund uses to formulate, execute and monitor the investment strategy. It should give the investor a clear understanding of how investment decisions are made, if by a committee or individually and how portfolios are monitored. This should also lead to the identification of of who the key people are within the organization. This refers to the Chief Investment Officer, Chief Risk Manager, Portfolio Managers and CEO. It is important that there is no overlapping of roles. It would create a strong conflict of interest if the Chief Risk Manager were also the Chief Investment Officer or a Portfolio Manager. A key personnel clause can help mitigate risks involved with the investment process, this clause obliges the fund manager to give notice to investors of any departures of key personnel.

Source of Added Value

Choosing a fund manager based on past returns is not by itself a metric that can prove to be reliable going forward. It is necessary to understand where the manager gets the added value from, it may be Alpha or it may simply be luck. It is important then to ask, what allows the manager to access Alpha? And are there reasons to think it may continue? The manager may be offering substantial returns due to risks being taken within the strategy such as liquidity or adding value by tax advantages. He may be proficient at using available information to better identify miss-priced assets and thereby offer enhanced returns.

Here we are trying to understand what makes the manager smarter than others, there are two primary explanations for superior performance based on information in competitive markets;

Information Gatherer or Searcher; here the manager may have a better information set than his peers. He may have a wider or deeper understanding that allows him to develop an improved information set. In this case the manager is not relying on superior analysis skill but on a superior information set. The manager may have a competitive edge created through specializing in a segment or sector giving an advantage in proprietary information collected over time.

Information Filterer or Analyzer; These managers have a competitive edge in extracting better trade ideas from an information set. In the case of quantitative or algorithmic trading the managers have an improved algorithm compared to their peers that allows them to generate more profitable trading patterns. With fundamental managers their advantage lies in their capability to take a mosaic view of publicly available information allowing them to develop more profitable insights and implement better performing trades.

Not all managers will necessarily identify with only one of the two styles, but in any case it fundamental to asses the managers capability in producing a competitive edge and the capability of keeping that edge going forward. It is necessary to analyse their strategies and sources of their returns to assess whether the manager is actually in a position to take advantage of an informational lead.

General Review

Once the three questions above have lead to satisfactory answers we then need to take several more steps to complete the process of Due Diligence. Needless to say this is a time consuming process and there are perhaps financial market professionals that pursue this regularly for many clients who are in a better position to carry out these tasks. However it is still useful to know what your investment advisor should be looking out for and what sort of questions you need to ask.

Structural Review; Here we need to look at how the fund has been set up and if it is tax efficient for the investor. Non US investors may face double taxation if the fund is not off-shore, on the other hand a US investor may need or prefer for the fund to be on-shore. Registrations that may be needed should be checked and verified, the investor should also check for any possible investigations or sanctions. Full details of the outside service providers should be supplied, such as the auditing company, prime broker or legal counsel.

Strategic Review; This part involves analysing the managers strategy which should be clearly stated and its appropriateness within the given Macro narrative. Hedge Fund strategy selection is far more important than it is in Mutual Fund selection, as discussed here.

Administrative Review; The investor needs to be authorised by the fund manager to carry out background checks on the manager himself and his/her principles. A long history of criminal or civil lawsuits should ring alarm bells, of course a divorce can also be a lawsuit, but then there may be the concern the person in question may be distracted by an external event. Each case should be considered individually however a principal with a record of lawsuits related to the financial field should cause concern as to the ethics of the person in question.

Performance Review; Here we take a look at a mangers performance in the classical risk adjusted return analysis of past performance. As already stated past performance does not guarantee future performance but it does tell how much risk the manager takes usually, which is also most likely to continue. Risky managers tend to continue being big risk takers as that is something that is fully in their control. A benchmark for the manager according to the assets traded and strategy applied should be used to consider how this manager has performed. It is also common to use a Hedge Fund index for peer comparison.Maximum draw down of a fund should also be reviewed. It is a big factor in revealing how much risk a manager is actually taking even more so than volatility.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst