Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

Most Managed Futures Funds will not offer separately managed accounts (SMAs) and often those that do have extremely high minimums ranging into the millions. However there are some CTAs that do offer separately managed accounts (SMAs) with a more accessible minimum amount, which may be as low as $50,000 or less. This type of investment has its advantages and disadvantages, we’ll take a look at both as well as a third possibility; CTA platforms.

Investing in managed futures has become more popular since the futures market turned predominantly to electronic trading. This new environment created much easier access to the futures market to a wider investor base, but most of all it created liquidity and transparency.

Advantages of a Separately Managed Account

SMAs allow you to have much more control over the investment in this type of asset class. These accounts offer the most transparency as the investor has access to all trade logs and activity and can even decide to exit a position if it was thought necessary. Liquidity is also high as positions can be liquidated and funds accessed any time the markets are open. In fact the money remains in the investor’s account; it is only through a power of attorney that the manager is authorized to trade on that capital which can be revoked at any time.

The investor can also choose how much leverage he/she wants the manager to use, and therefore personalize the amount of risk taken with the investment. CTA funds can be chosen based on their leverage, but if you want to decrease or increase it you would probably have to change fund.

Disadvantages of SMAs

These investments take a lot of work in setting up the account and in ongoing maintenance. You would need to process brokerage reconciliation and cash balance management and control. Probably the most important disadvantage is unlimited liability. If you invest in a fund your liability is limited to the amount of money you have placed in the fund, that is to say if you invest $200 thousand in a CTA fund you cannot lose more than that amount even if the manager incurs higher losses. However with a separately managed account you may be liable for more than the original investment due to the high levels of leverage which may be applied.

How to gain limited liability with SMAs

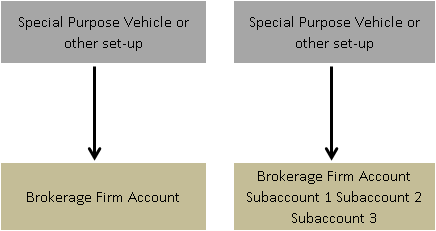

If the capital investment in SMAs is large enough it could justify setting up a structure that allows you to invest in SMAs but still maintain limited liability. Special Purpose Vehicles (SPV) can be set up which limit the liability to the amount placed in the SPV, the SPV then places the capital with the manager or managers running the SMAs. This is not the only structure to gain limited liability; depending on jurisdiction it may be possible to use a limited liability partnership or company. In either case the structure would function in a similar fashion and guarantee possible liabilities caused by the manager cannot affect other assets you own.

With an account with various subaccounts the managers are segregated and trade information is kept separate. You only need one set of account and formation documents and all subaccounts are cross collateralized. This structure is accepted in most jurisdictions including the USA.

Third possibility; CTA Platform

Recently a few financial services firms have started to offer the possibility of investing amongst a variety of CTAs, through a platform. These firms argue the key advantage is that the directors and vendors are objective and independent as they are selected by the firm that manages the platform not by the CTAs.

This structure allows you to choose which CTA you want to invest with given different levels of leverage, specialization of markets, strategy type and so on. Effectively allowing you to choose your personalized level of leverage and investment. Platforms also pass on some of the transparency and liquidity available to SMAs and are considered a hybrid of CTA funds and SMAs.

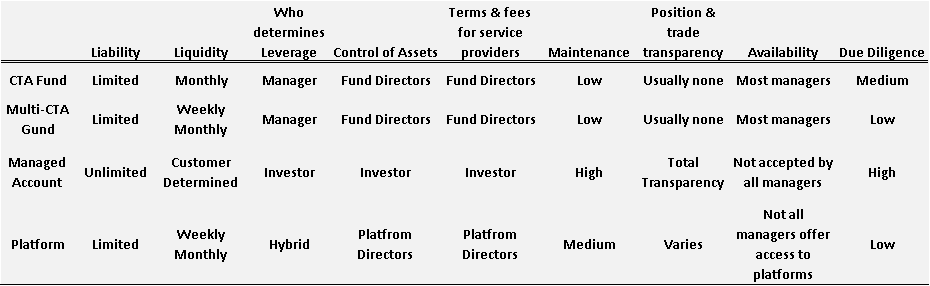

The chart above shows the main difference amongst CTA single and multi-manager, SMAs and platforms. We have seen how to go around the problem of unlimited liability that comes with a SMA, this means one less disadvantage and one more advantage.

However the advantages gained in personalization of leverage, strategy, maximum liquidity, complete transparency and total control, come at a price. Creating a portfolio of separately managed accounts will entail much more work and take away much more time. SMAs will consume more effort to perform the necessary due diligence and to maintain these investments.

Diversification amongst SMAs

As in all portfolio or sub-portfolio construction capital needs to be allocated to more than one risk source. As we are talking about investments within one type of asset, then the portfolio needs to be split up into various SMAs. You probably don’t want to have too many, as each one will take much more time and effort to oversee than a CTA fund, but you don’t want too few. You also don’t want to dilute the top performers by having too many managers. Ten managers are probably going to give a good mix and allow you to spread around 10% of your allocation to SMAs with each manager. This helps avoid one single manager that may be having a disastrous performance ruining the overall return of the portfolio. It also allows for the top managers to significantly add to total return as their performance is not too diluted.

Multi brokerage set-up

Often these managers will be in more than one brokerage firm; this can complicate things further as now you are going to need several different SPVs or entities to guarantee limited liability. If you use just one entity for all 10 CTAs then all the capital will be liable to the failure of any single fund. Setting up several SPVs or limited partnerships is going to get time consuming and expensive.

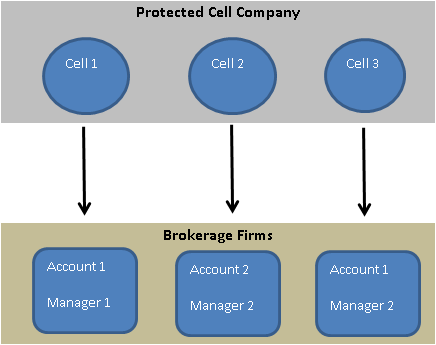

The way to get around setting up multiple companies is by structuring the investment within a Protected Cell Company. The figure below shows how this works. A single company is set up with various cells within the company. Each sell allocates a limited amount of capital to a manager, meaning each cell is protected by limited liability just as if it were a single entity. The managers’ performances are segregated allowing for precise risk and return analysis and ultimately portfolio management.

The Protected Cell Company forms one set of documents and provides addendums for each cell with one set of formation documents. If the company is formed correctly there is no cross liability amongst cells.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst