Disclosure: Our content isn't financial advice. Do your due diligence and speak to your financial advisor before making any investment decision. We may earn money from products reviewed. (Learn more)

- What exactly defines a 40s Act Fund?

- The main strategies and how they fit into my portfolio

- General performance in terms of risk and return

The limitations that set Liquid Alternatives apart from Hedge Funds

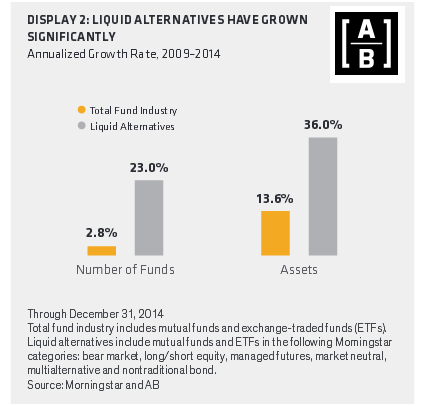

40s Act funds also known as Alternative Strategy Mutual Funds or Liquid Alternatives are compliant with the Investment Company Act of1940. Hence the name and have been around for some time but only really took off after the 2008 crisis. With a level of growth that has beaten that of long only funds. Investors started to see the need to redefine their risk levels and portfolio allocations. These funds unlike their bigger brothers, Hedge Funds, are available to be marketed publically. They may also have limits for minimum amounts to invest but in general they are open to retail investors as well as UHNW individuals or institutions.

These funds have to be set up as a mutual fund and offered through a fund sponsor. They are therefore obligated to provide daily liquidity just like mutual funds. There are no incentive fees for these funds but they tend to be slightly higher than typical mutual fund fees; management fees of 2% will be fairly standard in a 40s Act fund.

Even though these funds’ strategies go beyond the simple buy and hold of typical mutual funds they have many limitations. These limitations guarantee liquidity and risk reduction. First of all 40s Act funds must maintain no more than 15% of funds in illiquid assets. Illiquid assets are defined as those that take more than one day to liquidate. This guarantees redemptions are possible daily, which is also a requirement.

To reduce risk there are limitations on shorts and leverage. All shorts have to be fully backed by an equal amount of funds with a separate broker or custodian. Leverage is not allowed to be greater than 33% of assets. In times of highly volatile markets those are limitations your portfolio will probably appreciate.

Strategies in 40s Act funds

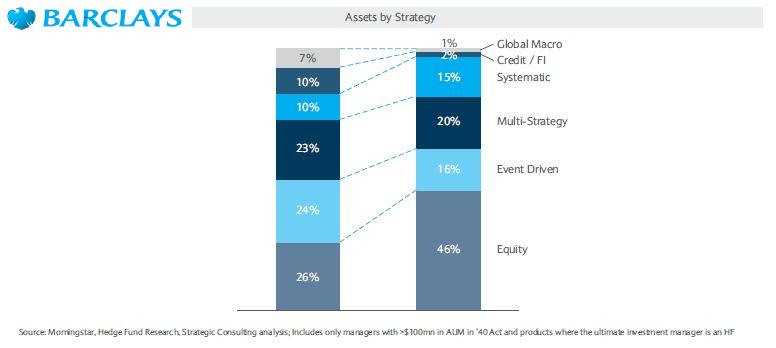

These funds can implement any of the Hedge Fund strategies as long as they remain within their limitations. 40s Act funds also have to deal with limitations in concentration; they are not allowed to hold more than 5% of securities from any one issuer. This may be a reason why the Macro Global strategy sees a lower percentage of AUM when compared to the Hedge Fund industry.

The chart above shows the largest share of strategies for 40s Act funds goes to the equity category. The category includes strategies like Long/Short, Market Neutral or Event Driven. This may be due to the easier strategy implementation for this category and the tendency for mutual fund managers to prefer strategies of this type.

These funds may be managed by a traditional Mutual Fund manager or by a Hedge Fund manager. In my opinion a Mutual Fund manager may lack some of the necessary skills and know how that are well acquired by a hedge fund manager. However some argue that a hedge fund manager will have less interest in their 40s act product as there are no incentive fees.

Why I should include 40s Act funds in my portfolio

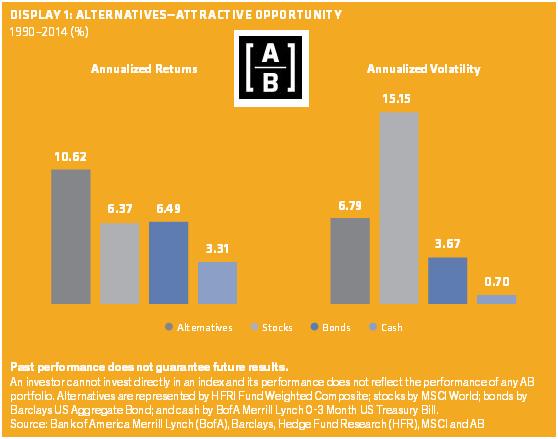

40s Act funds have proven to be able to beat the market and offer some protection to the downside. As seen with Hedge Funds over the past crisis there can be some reduction in overall maximum drawdown in times of stress. As with Hedge Funds 40s Act funds are also likely to reduce overall portfolio volatility. These funds over the past 20 years have proven to have a much lower risk profile than long only funds. The chart below shows annualized returns and volatility for 40s Act funds, Stocks, Bonds & cash. Data goes from 1990 to 2014, we see that liquid alternatives’ returns outperformed all the other assets yet had a volatility level that less than half that of stocks.

The average annualized return for 40s act funds during the 25 year period, which included the 2008 crisis, shows that these types of funds outperformed stocks by 4.25%. Volatility for these funds was lower than stocks by 8.36%

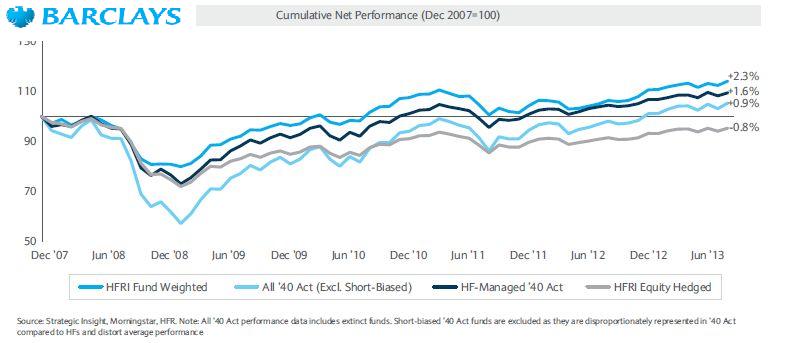

Holding these types of funds would certainly seem to have been able to enhance returns and reduce risk. The chart below shows the cumulative net performance of two Hedge Fund indices and two 40s Act indices from 2007 to 2013. We can appreciate the superior performance of the two 40s Act indices when compared to the hedge fund Equity index. Whereas the hedge fund weighted index outperformed all three.

We can also see how the hedge fund managed 40s Act index outperformed the broader All 40s Act index throughout the whole period. Looking at the period of the last crisis from 2008 to 2009; in the chart we can see that the hedge fund managed 40s Act index even performed slightly better than the hedge fund equity index.

Gino D'Alessio is a Broker/Dealer with over twenty years experience in various OTC markets such as Bonds, FX and Derivatives. Currently a Financial Markets and Investments Writer & Analyst